Neither universal nor creditable: The report of the Citizen’s Basic Income Trust’s Universal Credit working group to the trustees

The Citizen’s Basic Income Trust’s Universal Credit working group

At their meeting in October 2019 the trustees of the Citizen’s Basic Income Trust asked a group of three trustees to prepare a report on Universal Credit. The trustees appointed were Anne Gray, a social policy academic; Barb Jacobson, a Welfare Rights Advisor; and Gareth Morgan, Chief Executive Officer of Ferret Information Systems (the largest company in Europe in the field of law dealing with welfare benefits). Also members of the group were Colin Hampton, Coordinator of the Derbyshire Unemployed Workers’ Centre; and Malcolm Torry, Director of the Citizen’s Basic Income Trust. This is the group’s report to the trustees.

At their meeting on the 5th February 2020 the trustees approved the report for publication.

Introduction

The UK’s Universal Credit is a household-based, means-tested and work-tested benefit. A Citizen’s Basic Income would be an unconditional income for every individual, paid regularly without means test or work test. This report will compare these two very different ways in which a state might provide its population with an income.

Universal Credit is in crisis. Far from being an aid to people on low income, it has pushed many further into debt, use of foodbanks, rent arrears, and sometimes homelessness (Universal Credit: Not fit for purpose, Unite the union, 2019). Even worse than the five-week wait before it starts, Universal Credit payments fluctuate monthly, yet with a rigid assessment schedule which does not take into account actual paydays. Universal Credit therefore makes it impossible for claimants to plan payment of their bills more than one month in advance, and the draconian repayment demands for people who need Universal Credit advances leave some with nothing to live on despite their claim starting. Cuts, in the form of the two-child limit, the bedroom tax, the Local Housing Allowance, the Benefit Cap, the ‘Income Floor’ for the self-employed, promised new in-work conditionality, reductions in severe disability payment, and reductions in passport benefits such as free school meals and exemptions from National Health Service charges, have squeezed the incomes of people on Universal Credit. The cuts have also led to lower take-up, leaving many to rely on family, friends, and debt, to get by.

The Labour Party in their 2019 General Election manifesto promised to ‘scrap Universal Credit’, but did not say what they would replace it with; and the grassroots campaigns by Unite Community, Disabled People Against the Cuts, and others, seem mainly to advocate a return to the previous system. With the Conservatives now in power, even some of their politicians are starting to express doubts in private about Universal Credit, such are the problems reaching their surgeries and inboxes all over the country.

Far from the expensive, complicated process of returning to the old system, we need to reform social security by introducing a Citizens Basic Income as a foundational payment to each person, with housing, disability and other needs-based benefits on top. This would mean everyone would have a regular amount of money every month that they could count on, no matter how their employment, health or family situation might change. A Citizen’s Basic Income would enable and truly encourage budgeting, because everyone would have at least some money coming in every week. A Citizen’s Basic Income would also enable and truly encourage employment, by ensuring that everyone had enough money to eat, travel, and communicate in order to find a job: and they would not lose out if they found one. With separate payments to each individual, a Citizen’s Basic Income would help to ensure that family arrangements would be voluntary, and it would ameliorate the biggest cause of family breakdown: money and debt problems. A Citizen’s Basic Income would help to encourage more training, self-employment, and new enterprises, rather than burdening small businesses with further paperwork. A Citizen’s Basic Income would encourage more community and voluntary work, and would support those with caring responsibilities.

Elements of Universal Credit might still be needed for some people, but many households would no longer suffer from Universal Credit and the counter-productive, punitive and debt-inducing policies that surround it, and everyone would suffer less from them. It is time to introduce a regular national inheritance payment which would truly enable people ‘to reach their potential’.

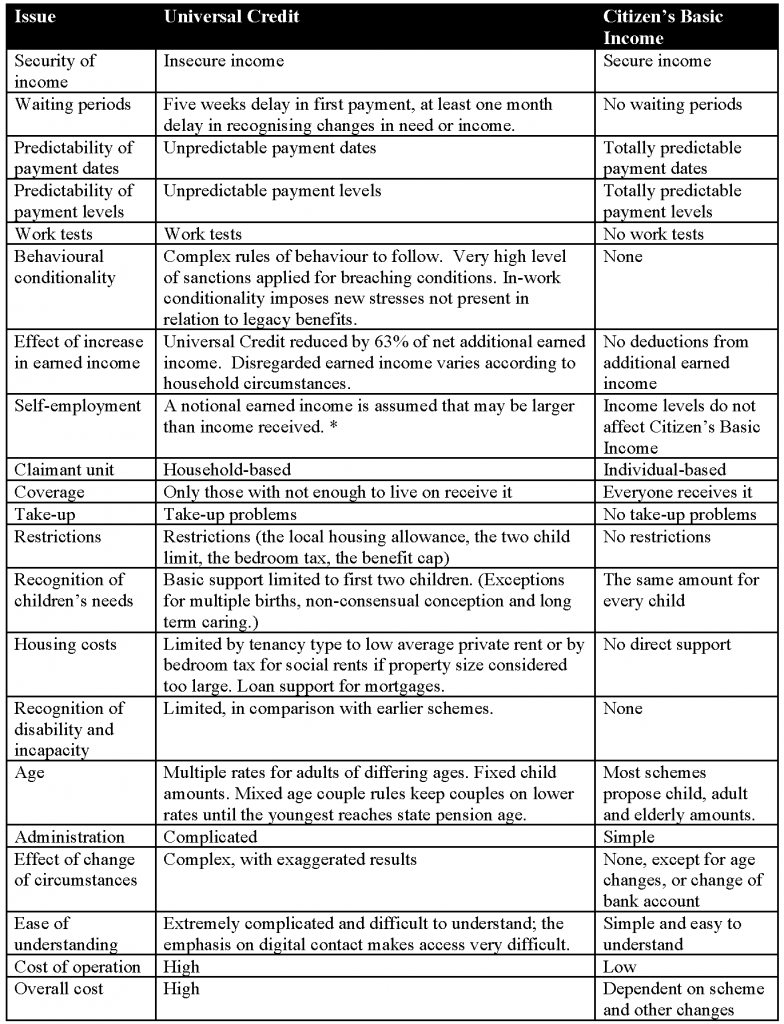

A table showing many of the differences between Universal Credit and Citizen’s Basic Income can be found in Appendix 1.

Universal Credit: payment periods and amounts

Two important aspects of income security are that income should arrive in a timely fashion and should be of predictable amounts. To an astonishing degree, Universal Credit appears to have been designed to remove security from many people. This is somewhat surprising, given the emphasis on the importance of security when the benefit was conceived.

For many looking to enter the world of work, a potentially unstable pattern of earnings poses many risks, and deters the first steps into work. A better benefits system will take account of the realities faced by those entering low wage jobs. Security of income is important, especially when a potential worker has a partner and children to consider. Benefits should be provided quickly: they are to supplement the income of those who cannot afford a decent living otherwise. They should be managed in a way to reflect or compensate for the natural cash-flow issues of those transitioning into and out of work. (Dynamic Benefits – Towards welfare that work, Centre for Social Justice, September 2009)

The importance of security of income was reinforced when the government enthusiastically adopted the concept.

The system will be simpler and will respond more quickly to changes in earnings so that people will not face the same complexities as they do now, particularly at the end of a tax year. As a result people will be much clearer about their entitlements and the beneficial effects of increasing their earnings by taking on more hours or doing some overtime. (Universal Credit – welfare that works, Secretary of State for Work and Pensions, November 2010)

If we were generous then we would attribute at least some of the system’s failings to an overoptimistic view of the technical challenges that the system would face: challenges clearly not understood by the Secretary of State:

This would involve an IT development of moderate scale, which the Department for Work and Pensions and its suppliers are confident of handling within budget and timescale. (Universal Credit – welfare that works)

We would, though, have to be extremely generous to find any excuse for the choices that were made about time periods and assessments. Every claimant household has an assessment period of a calendar month. Within this, earnings and income received, and some outgoings, are taken into account to determine the following month’s entitlement. A simple glance at the calendar will show that in four of the months during the year, people who are paid weekly will have five paydays, and in the other eight months they will have four. On constant earnings, that will mean that for one third of the year their benefits are assessed on earnings which are 25 per cent higher than for the remainder. If people receive their pay on a four weekly basis, then, similarly, there will be at least one month with two paydays in it; giving a 100 per cent increase in earnings taken into account. With some combinations of dates, people paid four-weekly will see more months with two paydays and some months with zero. People who are paid monthly and whose paydays fall close to the universal credit month start dates can face even worse situations. (For a more detailed look at this issue, and some consequences, see https://benefitsinthefuture.com/universal-credit-and-patterns-of-earning/ )

A single person with steady earnings can thus see their income vary dramatically month by month. If they pay rent weekly to a social landlord, they will find that they sometimes have five rent weeks in the universal credit month, and sometimes four, further complicating their disposable income after housing costs. A couple, who are both working, perhaps one paid weekly and one paid monthly, will see even more variation in benefits.

In future, it is likely that those months when universal credit is not paid because of the additional earnings that these rules assign to a particular month will also affect the amount of benefit in subsequent months, because of the surplus earnings rules expected to be introduced in full in April 2020.

These are the simple cases: people with steady earnings who could be expected to operate regular budgets. They are not those with a ‘potentially unstable pattern of earnings’ that the Centre for Social Justice were worried about. They will find themselves in an even worse situation.

Ignoring the many other failings of Universal Credit and the inadequate amounts often assessed under the rules, we should ask how this structural design feature might be mitigated. A fundamental change to the assessment calculation, such as moving to an annualised basis, could help, but would reintroduce many of the failings of the legacy tax credit system.

Citizen’s Basic Income: Payment periods and amounts

What, though, if there was to be a sum payable of a fixed amount, at fixed intervals, regardless of changes in earnings or other income? If it was large enough to extinguish any assessment of Universal Credit then the problems outlined above would go away. Even if it was less than the Universal Credit amounts payable, it would remove the problem for some people in some months, and reduce it for a lot more people in most months.

Universal Credit: Employment incentives

For most households, paid employment is at the heart of any strategy to provide a secure income; and paid employment is essential to providing the goods and services that individuals, households, and whole societies require.

Universal Credit is enthusiastically promoted by its advocates as a way to incentivise paid employment. Universal Credit was designed to do this better than the previous ‘legacy’ benefits by providing a ‘work allowance’: a level of earned income that would not be taken into account in Universal Credit calculations. This was designed to be particularly useful to people starting to work a small number of hours each week, because it meant that they would keep all or most of their Universal Credit. The five week wait and the monthly payments were designed to mirror a world of work in which wages are paid in arrears and on a fixed day of the month despite the differing lengths of those months. However, the world presented in this way to claimants is one that is unrecognisable to the majority of people reliant on Universal Credit. For many, far from incentivising paid employment, Universal Credit has the opposite effect. There was a massive under-claiming of the legacy benefits and many more will be put off claiming their entitlements by the nature of the new regime. For those able to navigate the system, surveys show that many are descending into debt, relying on foodbanks, getting into rent arrears, and facing eviction, purely as a result of the characteristics of Universal Credit. The damage done by forcing people into indebtedness, far from encouraging people to get closer to the labour market, is driving people away from the prospect of employment, as spiralling debt and insecurity impacts on mental and physical wellbeing. The threat and imposition of sanctions adds to that insecurity and stress. Impoverishing people is not an ‘activation’ policy, but rather it acts as a warning to those in work to do all they can to avoid having to interface with Universal Credit or become unemployed. This means accepting poor terms and conditions of work, and squeezes on wage levels.

It is claimed that 200,000 more people will be in work when the rollout of Universal Credit is complete, but the National Audit Office says ‘the Department will never be able to measure whether Universal Credit actually leads to 200,000 more people in work’. The statistics on foodbank usage, debt and rent arrears, though, make stark reading. Universal Credit, far from being a route to employment, appears, for many, to be a pathway to destitution. The evidence should be making government take notice of the problems it is creating for the health of its citizens as well as their precarious financial position. The situation concerning rent arrears and evictions is alarming. It makes no sense, under the auspices of saving money for the exchequer, to plunge people into serious financial problems, with life-changing consequences that impose a greater burden on the taxpayer in the long run. It appears that despite knowing how Universal Credit is forcing people into poverty, the Government is still intent on ploughing ahead regardless, pushing families to the brink of survival.

Citizen’s Basic Income: Employment incentives

In order for people to contribute in society, whether through paid employment or other activities, they need to be sustained. Mental and physical wellbeing are crucial. The security that a regular income would help to ensure would make paid employment more likely to occur. A Citizen’s Basic Income would completely avoid the access problems that have been heavily reported with Universal Credit, and its predictability would make budgeting and money management a possibility. The corresponding impact on physical and mental wellbeing, with the ability to be able to sustain oneself and one’s family, and the increased sense of security that this would bring, should not be underestimated. Above all, if the earned income of someone on Universal Credit increases, then Universal Credit is withdrawn, and after Income Tax and National Insurance Contributions are deducted as well they can receive an increase in disposable income of only about a quarter of the increase in earnings. Someone whose Citizen’s Basic Income took them off Universal Credit would have only Income Tax and National Insurance Contributions withdrawn, and so their disposable income would increase by a higher proportion of any increase in earned income, and there would be more incentive to seek an additional employment hours, a better job, or additional skills training. Someone receiving a smaller Citizen’s Basic Income, and therefore still on Universal Credit, might be able to take themselves off Universal Credit by adding a relatively small amount of additional earned income, and when they did then they too would experience enhanced employment incentives.

Universal Credit: Labour supply and employers’ behaviour

Whilst government claims that Universal Credit motivates (re)entry into work, in so far as it does so it is to a considerable extent at the expense of the taxpayer, since the effect is to make some low paid jobs acceptable which would otherwise be rejected or taken only under duress, that is, under threat of benefit sanctions. The cost of this hidden subsidy to low-paying employers may well have motivated the increases in the National Minimum Wage under Conservative governments, and there was some evidence of this in George Osborne’s budget speech in July 2015. It is likely that some employers would have had to raise their wage rates to fill vacancies in the absence of Universal Credit, so Universal Credit might be said to have had a wage-depressing effect.

Citizen’s Basic Income: Labour supply and employers’ behaviour

Citizen’s Basic Income might also be considered a wage subsidy, but not in quite the same way. Its introduction could be expected to have the following effects on labour supply:

- The receipt of Citizen’s Basic Income would not be dependent on fulfilling externally imposed job-seeking conditions, so workers would feel free to reject some low paid or insecure jobs and prolong their search for better work. Employers would find it more difficult to recruit for low paid or insecure jobs, and might have to raise wages or offer greater security;

- Some unwaged people who had thought it not worth looking for work because of the prospect of losing unwaged benefits would enter the labour market, augmenting labour supply, and potentially depressing wages;

- Some unwaged people would feel a secure income stream from Citizen’s Basic Income would make it possible for them to take the risk of becoming self-employed. This might lead to an increase in their own economic activity, and also greater acceptability of working in the ‘gig economy’;

- Some people who would, under Universal Credit, have been in work – probably a smaller number than the total of the first three categories – would opt for more leisure, or more caring time or education/training time, reducing labour supply and exerting upward wage pressure.

Of the four effects above, (1) and (4) would operate to raise wages and improve working condition. Effect (1) is not heavily dependent on the level of Citizen’s Basic Income, whereas effect (4) would only occur if the Citizen’s Basic Income were large enough for people to contemplate staying out of paid employment. Effects (2) and (3), on the other hand, would depress wages. If overall labour supply were to rise, then the wage-depressing effect would win out. If overall labour supply were to fall, then wages would increase. A research exercise undertaken in 2017 suggested that the overall effect in the UK economy might be a slight fall in wage levels. (http://citizensincome.org/research-analysis/behavioural-effects-of-a-citizens-income-on-wages-job-security-and-labour-supply/ ).

The evidence from pilot projects is that Citizen’s Basic Income would result in an increase in labour market engagement and an increase in self-employment start-ups. A possible consequence is that Citizen’s Basic Income could make insecure and short hours jobs more acceptable (Standing).

These considerations suggest that implementation of a Citizen’s Basic Income scheme would need to go hand in hand with appropriate labour market regulation, and that the higher the Citizen’s Basic Income, the more such regulation might be thought appropriate. On the other hand, a smaller Citizen’s Basic Income would leave more people on means-tested and work-tested benefits, which could lead to a greater Universal Credit wage subsidy effect, which in turn would mean the combination of Citizen’s Basic Income and Universal Credit subsidising employers rather than benefiting the intended beneficiaries. All of this suggests that care would need to be taken to match labour market regulation to the Citizen’s Basic Income scheme chosen for implementation. (See appendix 2 for a discussion of the effects of an increase in the National Living Wage.)

Conclusion

‘Social Security’ embodies in its two words some important concepts. ‘Social’ implies that social security benefits should be of service to society, specifically by promoting social cohesion, preventing poverty, and reducing inequality; and ‘security’ implies that social security benefits should ensure that individuals and families should experience security, and in particular secure incomes. The content of this report suggests that Universal Credit neither delivers security nor serves society, and that Citizen’s Basic Income would do both.

Universal Credit and Citizen’s Basic Income have some similar aims: To reduce the prevalence of poverty and unemployment traps; to incentivise employment; and to provide an income for those who need it. However, they are very different in their characteristics, as the table above shows, and they are radically different in their effects, as the rest of this report amply demonstrates. It is differences in both their characteristics and effects that suggest that Citizen’s Basic Income would be more likely than Universal Credit to secure desirable social and economic outcomes, and provide the genuine social security that the country needs. More secure incomes would improve mental health, relationships, social cohesion, the ability to budget, and economic risk-taking, and would reduce indebtedness; the absence of work tests and sanctions would improve motivation and mental health, would encourage diverse kinds of work, and would reduce workplace anxiety; the absence of means tests would improve employment motivation and diverse income generation; payment to individuals would improve relationships and gender equality; universality and the absence of take-up problems would reduce poverty, inequality, and stigma, and would improve social cohesion; and the absence of restrictions would reduce anxiety and, with the right Citizen’s Basic Income scheme, would reduce poverty.

It would therefore be ideal if the UK were to establish a Citizen’s Basic Income that would be enough to live on. In practical terms, this would mean a Citizen’s Basic Income at least high enough to ensure that means-tested benefits could be abolished without imposing disposable income losses on low income households. Such a sizeable Citizen’s Basic Income would ensure that all of its social and economic benefits would be maximised.

However, in the immediate future only a smaller Citizen’s Basic Income, funded by changes to the current tax and benefits system, a carbon tax, or both, would be likely to be financially feasible. In this case, the Citizen’s Basic Income scheme (the Citizen’s Basic Income with the levels for different age groups specified, with the funding method specified, and with any changes to the existing tax and benefits system specified) would need to ensure that low income households would not suffer disposable income losses, and that poverty and inequality indices would be reduced.

A smaller Citizen’s Basic Income could work well alongside a continuing Universal Credit. The Citizen’s Basic Income would immediately take a lot of households off Universal Credit; it would reduce the amounts of Universal Credit received by all households, thus enabling many of them to escape from Universal Credit by adding small amounts of earned income; and the Citizen’s Basic Income would have entirely predictable effects on Universal Credit calculations and so would not complicate it any more than it is already.

An additional advantage of Citizen’s Basic Income is that Child Basic Incomes would be paid to the children’s main carer, unlike Universal Credit where the child elements are normally paid to the individual who makes the claim for the household.

If a smaller Citizen’s Basic Income were to make it necessary to retain Universal Credit, then the Unite demands for the reform of Universal Credit should be implemented (see appendix 3). This would bring Universal Credit closer in character to Citizen’s Basic Income, and therefore closer in its effects.

Appendix 1

A comparison of Universal Credit and Citizen’s Basic Income

* Monthly reports have to be hade, which does not reflect the way in which self-employed individuals receive income. Universal Credit was meant to make life easier for people with varying earnings, but has in fact made it more difficult.

Appendix 2

The effects of an increase in the National Minimum Wage

As we have seen, the implementation of a Citizen’s Basic Income scheme would require labour market regulation to be reconsidered. An important element in any such reconsideration will be the level of the National Living Wage, the effects of which are not always obvious. At the end of 2019 an increase was announced. This was said to be a £930 a year increase for someone on 35 hours a week paid at the National Living Wage. The reality is different.

For the employee, the £930 per annum headline figure for 35 hours a week becomes £631 after Income Tax and National Insurance Contributions at current rates, and it becomes £233 if they are getting Universal Credit, as the means-tested benefit is withdrawn as earned income rises. There will probably also be a reduction of around £120 per annum in Council Tax Relief, depending on the area of residence. The net gain will therefore be about £115 per annum.

For the employer employing someone for 35 hours per week on the National Living Wage, the wage bill will rise by £930 a year. The employee on Universal Credit will get £233 or £115. The other £697 or more goes straight to the government in Income Tax, National Insurance Contributions, and benefits withdrawal. Employer costs will also rise by a £128 increase in National Insurance Contributions if no Employment Allowance applies.

So, in a typical case, the rise in National Minimum Wage supposedly aimed at helping the lowest paid gives them just £115 extra per annum, the local authority £120, and the government £825. The employer pays approximately £1,060.

If a Citizen’s Basic Income were to be sufficient to take the worker off means-tested benefits, then there would be no benefit withdrawal, and the worker would receive approximately an additional £631 per annum from an increase in the National Living Wage of £930 per annum. If the level of Citizen’s Basic Income were not sufficient to take the worker off means-tested benefits then they would be receiving less in means-tested benefits, less might be withdrawn, and they would receive something between £631 and £115 per annum of the £930 per annum increase in the National Living Wage.

Appendix 3

The Unite demands for the reform of Universal Credit (Universal Credit: Not fit for purpose, Unite the union, 2019, p. 27)

Unite is campaigning to stop and scrap Universal Credit. Should government refuse to scrap Universal Credit, Unite strongly demands that government commits to:

- End benefit sanctions for all claimants and abolish plans to introduce in-work conditionality.

- Ending the long waits for claimants to receive money, and the unsustainable debts caused by advanced payments.

- Allow people to apply for Universal Credit in jobcentres with face to face support, not just online.

- Introduce flexibilities within the monthly assessment system to recognises that people are not all paid monthly or regularly.

- Provide people with better help when the system fails them, including through adequate levels of staffing for the system and proper funding to advice and legal aid services for claimants.

- Reverse the in-built benefit cuts within Universal Credit including lifting the cap on benefit uprating, removal of the taper rates for payments, reversing the cuts to the work allowance in full, scrapping the unfair ‘two-child’ policy and removal of the first child premium.

- Simplifying the childcare support offered to Universal Credit claimants to prevent claimants having to cover massive upfront costs.

- Allow payments to multiple recipients within the same household to prevent financial dependence on one individual and provide some protection for victims of domestic abuse

- Remove the Minimum Income Floor for the self-employed.

- Pay landlords directly to stop people getting into rent arrears and losing their homes.

- Introduce incentives and penalties on employers to protect claimants from error or malicious act that cause benefits not to be paid. This should include an enforcement body with real power to win compensation and sanction employers who cause Universal Credit claimants to lose their benefits, as well as an extension of the right of workers to bring tribunal claims against employers for unpaid wages to include unpaid, underpaid or late Universal Credit.

- Give claimants the right to trade union help and representation for Universal Credit claims. Trade unions should also be given formal enforcement powers, including the ability to bring a class action.

Click here to download the report as a pdf

Further reading: Citizen’s Basic Income: A brief introduction

.

This is interesting, it would be useful to see in real terms what happens to the income subsidy received from government, and what is the state of industry which requests a government “top up”, via universal credit on the income given to a household.

Example

1) A benefits only income consisting of 317.82 (Adult over 25) + Rent (Housing Association of 359.50). Ends up as 53% to a Landlord. In the case of private renters this can be a much higher percentage. This looks like payment to government but in fact is payment to Landlords.

2) Similarly a council tax payment ends up subsidising a variety of industries. because it provides raw materials from fertiliser to scrap metals and more, however it seems that although the full supply chain is profitable, even highly profitable, the cost is apportioned in such a way to gain more from the councils.

3) The contributions that you speak of above to council tax and income tax made by people earing below the median wage will subsidise earnings above the median wage if a contract is provided to the tax budget and the profit of the company in question apportions a staff cost above the average.

4) If UC is subsidising wage of low earners, and the industry is profitable in the supply chain, then the subsidy is collected by government but handed to the industry. E.g. if potatoes are sold at 17p per kilo from the field, and sold in a fast food chain at 2.00 for a fifth of a kilo, Then it is likely that the supply chain somewhere is profitable. The fast food chain may be making a high profit, or its supplier of ready cut chips. The wage of the worker however is subsidised by the tax payer.

5) Once again things go full circle, because even in the subsidised minimum wage . If it was £8.21 an hour, would be apportioned to a % rent, % food % clothing. Because rent is too high a portion, and possibly other items at retail like food, then a too high % of the wage (subsidised by government or not) goes to the landlords, industry chain etc