Introduction

This research note summarises parts of a recent working paper published by the Institute for Social and Economic Research, Static microsimulation research on Citizen’s Basic Income for the UK: a personal summary and further reflections, EUROMOD working paper EM13/19 (Colchester: Institute for Social and Economic Research, 2019) [1]

An up to date Citizen’s Basic Income scheme

The new version of EUROMOD, I1.0+, along with updated Family Resources Survey (FRS) data, has enabled what has become a fairly consistent Citizen’s Basic Income scheme in recent EUROMOD working papers to be brought thoroughly up to date and retested. Only minor changes have been required to ensure that the scheme continues to fit a normal list of criteria. The only caveats in relation to results being ‘up to date’ are that:

- the FRS data is collected via a rolling programme of interviews, so it is always to some extent out of date;

- neither the UK country system nor the FRS data enable us to take account of the roll-out of the UK Government’s new means-tested benefit, Universal Credit; and

- because Council Tax Support is now localised, and each local authority can set its own regulations and taper rates, calculations relating to Council Tax Benefit might provide less of a useful picture than calculations relating to other means-tested benefits.

The scheme tested here is funded from within the current tax and benefits system by reducing to zero the Income Tax Personal Allowance and the National Insurance Contributions Primary Earnings Threshold, charging National Insurance Contributions (NICs) at 12% on all earned income, and increasing Income Tax rates slightly. Current means-tested benefits would be left in place, and each household’s means-tested benefits would be recalculated to take into account household members’ Citizen’s Basic Incomes in the same way as their earned income is taken into account. The list of requirements for financial feasibility is as follows:

- as few changes as possible are to be made to the current tax and benefits system, consistent with the other aims in view;

- revenue neutrality (Hirsch, 2015), which I shall take to be a net cost or saving of no more than £2bn;

- the avoidance of significant household net disposable income losses, particularly for low income households (with an aim of ensuring that no more than 2% of low income households should experience household net disposable income losses of more than 5%);

- Income Tax rates to rise by no more than 3 percentage points (Hirsch, 2015);

- reductions in inequality (measured by the Gini coefficient) and in all poverty indices.

The illustrative Citizen’s Basic Income scheme that emerges is found to be as follows:

- Child Benefit is increased by £20 per week for each child.

- Citizen’s Basic Income levels are set as follows: An Education Age Citizen’s Basic Income (ECBI), for 16 to 19 year olds no longer in full-time education, is set at £40 per week; a Young Adult’s Citizen’s Basic Income (YCBI), for people aged 20 to 24, is set at £50 per week; a Working Age Adult Citizen’s Basic Income (WACBI, or simply CBI), for people aged 25 to 64, is set at £65 per week; and a Citizen’s Pension, for everyone aged over 65, is set at £40 per week. The existing National Insurance Basic State Pension is left in place. (In this particular scheme, the ECBI is not paid to someone still in full-time education, in recognition of the fact that their main carer is receiving Child Benefit on their behalf.). Table 1 gives the detail of the scheme and the household net disposable income losses generated for all households and for the lowest original income quintile.

Table 1 shows the parameters of the scheme and the losses generated, and table 2 shows the changes in the numbers of households receiving a variety of means-tested benefits, and also the numbers of households brought within striking distance of coming off them.

Table 1: The standard Citizen’s Basic Income scheme and losses generated

| CBI levels, tax rates, numbers of losses over various limits for all households and lower quintile, and total net cost of scheme for fiscal year 2018-19. | |

| Citizen’s Pension per week (existing state pensions remain in payment) | £40 |

| Working age adult Citizen’s Basic Income per week [2] | £65 |

| Young adult Citizen’s Basic Income per week | £50 |

| Education age Citizen’s Basic Income per week | £40 |

| (Child Benefit is increased by £20 per week) | [£20] |

| Income Tax rate increase required for strict revenue neutrality | 3% |

| Income Tax, basic rate (on £0 – 46,350) | 23% |

| Income Tax, higher rate (on £46,350 – 150,000) | 43% |

| Income Tax, top rate (on £150,000 – ) | 48% |

| Proportion of households in the lowest original income quintile experiencing losses of over 15% at the point of implementation | 1.23% |

| Proportion of households in the lowest original income quintile experiencing losses of over 10% at the point of implementation | 1.77% |

| Proportion of households in the lowest original income quintile experiencing losses of over 5% at the point of implementation | 3.71% |

| Proportion of all households experiencing losses of over 15% at the point of implementation | 0.41% |

| Proportion of all households experiencing losses of over 10% at the point of implementation | 1.74% |

| Proportion of all households experiencing losses of over 5% at the point of implementation (losses over 6%: 7.11%) | 12.54% |

| Net cost of scheme | £1.41bn p.a. |

Source: own calculations with EUROMOD version I1.0+.

Table 2: Reductions in numbers claiming means-tested benefits or within striking distance of coming off them, and the reductions in the totals costs of the benefits and the average value of claims

| Reductions in numbers claiming means-tested benefits or within striking distance of coming off them | The existing scheme in 2018 | The Citizens Basic Income scheme | % reduction |

| Percentage of households claiming out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 13.28% | 11.12% | 16.23% |

| Percentage of households claiming more than £100 per month in out-of-work benefits (defined as above) | 13.06% | 5.50% | 57.86% |

| Percentage of households claiming in-work benefits (Working Tax Credits and Child Tax Credits) | 13.28% | 10.77% | 18.86% |

| Percentage of households claiming more than £100 per month in in-work benefits (defined as above) | 12.08% | 9.86% | 18.45% |

| Percentage of households claiming Pension Credit | 5.81% | 5.39% | 7.25% |

| Percentage of households claiming more than £50 per month in Pension Credit | 4.95% | 4.39% | 11.36% |

| Percentage of households claiming Housing Benefit | 15.76% | 15.71% | 0.33% |

| Percentage of households claiming more than £100 per month in Housing Benefit | 14.68% | 14.63% | 0.32% |

| Percentage of households claiming Council Tax Benefit | 21.19% | 20.61% | 2.76% |

| Percentage of households claiming more than £50 per month in Council Tax Benefit | 16.38% | 15.35% | 6.31% |

| Percentage of households claiming any means-tested benefits | 32.86% | 30.45% | 7.35% |

| Percentage of households claiming more than £100 per month in means-tested benefits | 28.98% | 24.31% | 16.11% |

| Percentage of households claiming more than £200 per month in means-tested benefits | 26.23% | 20.67% | 21.20% |

| Reductions in total costs and average values of claims for means-tested benefits | Reduction in total cost | Reduction in average value of claim

|

|

| Out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 70.95% | 59.62% | |

| In-work benefits (Working Tax Credits and Child Tax Credits) | 23.24% | 3.75% | |

| Pension Credit | 28.64% | 22.87% | |

| Housing Benefit | 2.40% | 1.15% | |

| Council Tax Benefit | 8.72% | 2.41% | |

| All means-tested benefits | 30.60% | 22.00% | |

Source: own calculations with EUROMOD version I.10+.

Note: EUROMOD microsimulation of both the 2018 tax and benefits system and the Citizen’s Basic Income scheme generates information on the number of claims for each social security benefit for the two options, and also information on the total cost of those benefits and on the average values of benefits claims. To obtain the numbers claiming benefits the weights attached to the households in the survey that are claiming the relevant benefits are added together.

Table 3 shows reductions in inequality and in poverty rates.

Table 3: Inequality and poverty indices

| Inequality and poverty indices | The current tax and benefits scheme in 2018 | The Citizen’s Basic Income scheme | Percentage change in the indices |

| Inequality | |||

| Disposable income Gini coefficient | 0.3087 | 0.2756 | 10.73% |

| Poverty headcount rates | |||

| Total population in poverty | 0.16 | 0.11 | 29.57% |

| Children in poverty | 0.18 | 0.11 | 42.08% |

| Working age adults in poverty | 0.15 | 0.11 | 28.17% |

| Economically active working age adults in poverty | 0.06 | 0.04 | 37.48% |

| Elderly people in poverty | 0.14 | 0.12 | 14.80% |

Source: own calculations with EUROMOD version I.10+.

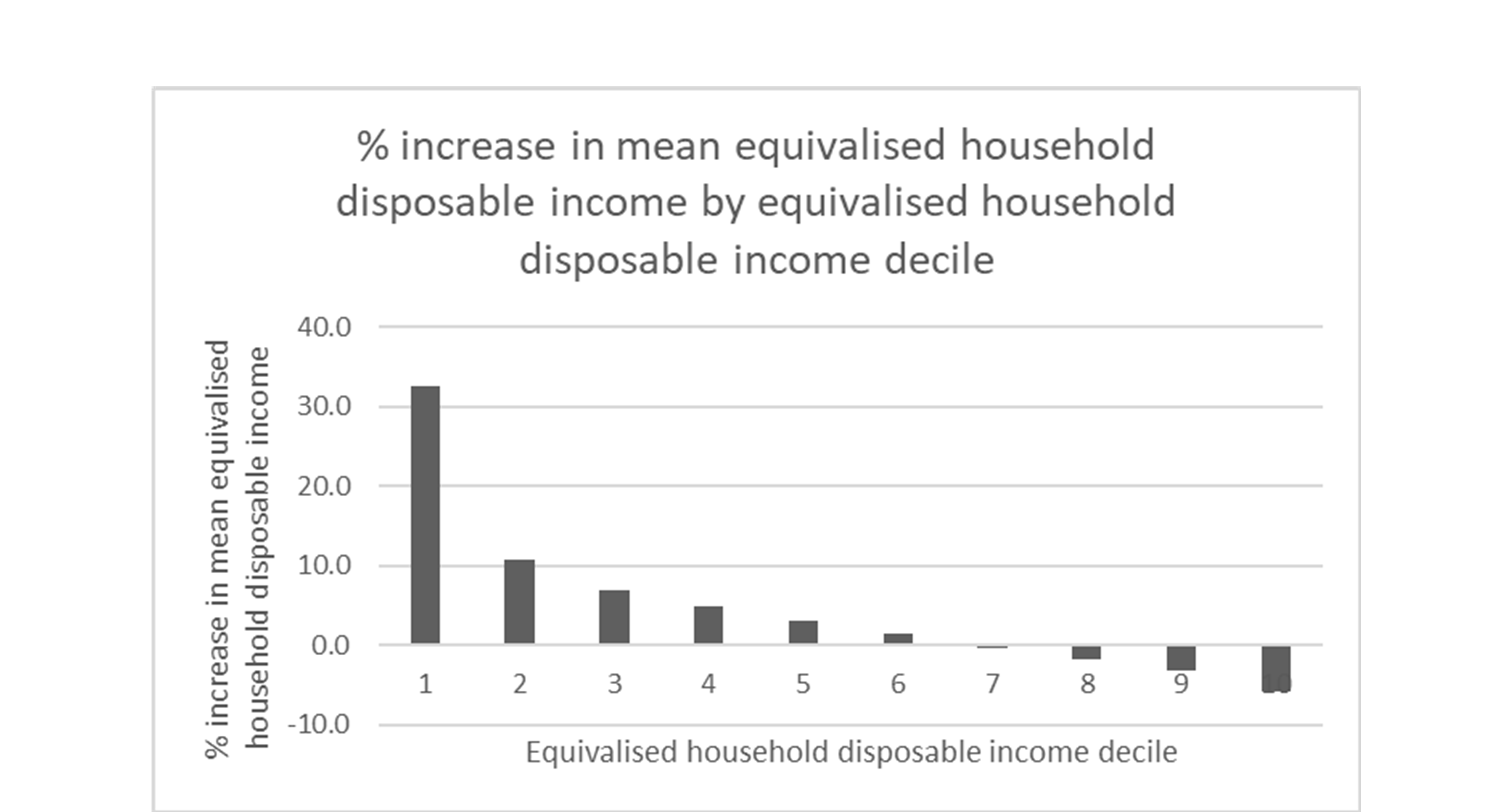

Table 4 shows the changes in mean household disposable income by decile groups, and also mean equivalised household disposable income by decile group, the latter taking account of the composition of the household.

Table 4: Mean (equivalised) income by decile groups

| Decile group | % change in mean household disposable income | % change in mean equivalised household disposable income |

| 1 | 31.21 | 32.54 |

| 2 | 9.7 | 10.66 |

| 3 | 5.98 | 6.81 |

| 4 | 4.21 | 4.96 |

| 5 | 2.38 | 3 |

| 6 | 0.95 | 1.4 |

| 7 | -0.7 | -0.47 |

| 8 | -1.89 | -1.76 |

| 9 | -3.17 | -3.18 |

| 10 | -5.71 | -5.82 |

Source: own calculations with EUROMOD version I.10+.

(It might be of interest that the figures look very similar whether or not equivalised household incomes are employed. This suggests that all of the deciles contain similar spreads of household sizes.)

Figure 1 is a graphical representation of the redistribution pattern.

Figure 1

Source: own calculations with EUROMOD version I.10+.

We can conclude that this updated version of what has become a standard feasible Citizen’s Basic Income scheme in EUROMOD working papers would be revenue neutral (that is, it could be funded from within the current income tax and benefits system); and that the increase in Income Tax rates required would be feasible. The scheme would substantially reduce poverty and inequality; it would remove large numbers of households from a variety of means-tested benefits; it would reduce means-tested benefit claim values, and the total costs of means-tested benefits; it would provide additional employment market incentives for the large number of households no longer on means-tested benefits to the extent that marginal deduction rates affect employment market behaviour; and it would avoid imposing significant numbers of losses at the point of implementation.

Because the only changes required in order to implement this illustrative Citizen’s Basic Income scheme would be

- payment of the Citizen’s Basic Incomes for every individual above the age of 16 (apart from those between 16 and 19 still in full-time education), calculated purely in relation to the age of each individual,

- increases in the rates of Child Benefit,

- changes to Income Tax and National Insurance Contribution rates and thresholds, [3] and

- easy to achieve recalculations in existing means-tested benefits claims,

the entire scheme could be implemented very quickly.

This simple illustrative scheme could be both feasible and useful.

Responses to recent questions

During the past year I have collected up the following questions, which I shall tackle in turn:

- What would be the effect of raising the working age Citizen’s Basic Income from £63 per week (the 2018 level for working age adults) to £70 per week?

- How much would it cost to run a pilot project for a whole community for a genuine Citizen’s Basic Income of £70 per week for working age adults?

- Would it be possible to construct a financially feasible Citizen’s Basic Income scheme that retained a small Income Tax Personal Allowance rather than reducing it to zero?

- Would it be possible to reduce the Income Tax rates required to fund a Citizen’s Basic Income scheme if the top rate of tax was raised to 70%?

- What’s causing the losses for low income households, and is it possible to reduce them?

- What would be the effect of raising the working age Citizen’s Basic Income to £70 per week?

For this exercise, the usual set of requirements for financial feasibility was employed. A financially feasible Citizen’s Basic Income scheme was discovered as follows:

Table 5: The £70 per week Citizen’s Basic Income scheme and losses generated

| Citizen’s Pension per week (existing state pensions remain in payment) | £40 |

| Working age adult Citizen’s Basic Income per week | £70 |

| Young adult Citizen’s Basic Income per week | £60 |

| Education age Citizen’s Basic Income per week | £25 |

| (Child Benefit is increased by £5 per week) | [£5] |

| Income Tax rate increase required for strict revenue neutrality | 3% |

| Income Tax, basic rate (on £0 – 46,350) | 23% |

| Income Tax, higher rate (on £46,350 – 150,000) | 43% |

| Income Tax, top rate (on £150,000 – ) | 48% |

| Proportion of households in the lowest original income quintile experiencing losses of over 15% at the point of implementation | 1.59% |

| Proportion of households in the lowest original income quintile experiencing losses of over 10% at the point of implementation | 2.29% |

| Proportion of households in the lowest original income quintile experiencing losses of over 5% at the point of implementation | 4.19% |

| Proportion of all households experiencing losses of over 15% at the point of implementation | 0.48% |

| Proportion of all households experiencing losses of over 10% at the point of implementation | 1.52% |

| Proportion of all households experiencing losses of over 5% at the point of implementation (losses over 6%: 6.22%) | 11.59% |

| Net cost of scheme | £1.14bn p.a. |

Source: own calculations with EUROMOD version I.10+.

Table 6 shows the changes in the numbers of households receiving a variety of means-tested benefits, and also the numbers of households brought within striking distance of coming off them.

Table 6: Reductions in numbers claiming means-tested benefits or within striking distance of coming off them, and the reductions in the totals costs of the benefits and the average value of claims

| Reductions in numbers claiming means-tested benefits or within striking distance of coming off them | The existing scheme in 2018 | The Citizens Basic Income scheme | % reduction |

| Percentage of households claiming out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 13.28% | 9.56% | 28.05% |

| Percentage of households claiming more than £100 per month in out-of-work benefits (defined as above) | 13.06% | 5.46% | 58.18% |

| Percentage of households claiming in-work benefits (Working Tax Credits and Child Tax Credits) | 13.28% | 10.59% | 20.25% |

| Percentage of households claiming more than £100 per month in in-work benefits (defined as above) | 13.06% | 9.71% | 19.66% |

| Percentage of households claiming Pension Credit | 5.81% | 5.38% | 7.48% |

| Percentage of households claiming more than £50 per month in Pension Credit | 4.95% | 4.38% | 11.55% |

| Percentage of households claiming Housing Benefit | 15.76% | 15.56% | 1.27% |

| Percentage of households claiming more than £100 per month in Housing Benefit | 14.68% | 14.47% | 1.42% |

| Percentage of households claiming Council Tax Benefit | 21.19% | 20.25% | 4.42% |

| Percentage of households claiming more than £50 per month in Council Tax Benefit | 16.38% | 15.05% | 8.12% |

| Percentage of households claiming any means-tested benefits | 32.86% | 29.24% | 11.02% |

| Percentage of households claiming more than £100 per month in means-tested benefits | 28.98% | 24.38% | 15.86% |

| Percentage of households claiming more than £200 per month in means-tested benefits | 26.23% | 20.39% | 22.26% |

| Reductions in total costs and average values of claims for means-tested benefits | Reduction in total cost | Reduction in average value of claim

|

|

| Out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 75.07% | 65.35% | |

| In-work benefits (Working Tax Credits and Child Tax Credits) | 24.83% | 5.75% | |

| Pension Credit | 29.10% | 23.37% | |

| Housing Benefit | 3.61% | 2.37% | |

| Council Tax Benefit | 8.47% | 4.24% | |

| All means-tested benefits | 32.10% | 23.69% | |

Source: own calculations with EUROMOD version I.10+.

Table 7 shows reductions in inequality and in poverty rates.

Table 7: Inequality and poverty indices

| Inequality and poverty indices | The current tax and benefits scheme in 2018 | The Citizen’s Basic Income scheme | Percentage change in the indices |

| Inequality | |||

| Disposable income Gini coefficient | 0.3087 | 0.2811 | 8.95% |

| Poverty headcount rates | |||

| Total population in poverty | 0.16 | 0.12 | 23.46% |

| Children in poverty | 0.18 | 0.14 | 25.26% |

| Working age adults in poverty | 0.15 | 0.12 | 24.78% |

| Economically active working age adults in poverty | 0.06 | 0.04 | 32.01% |

| Elderly people in poverty | 0.14 | 0.12 | 15.75% |

Source: own calculations with EUROMOD version I.10+.

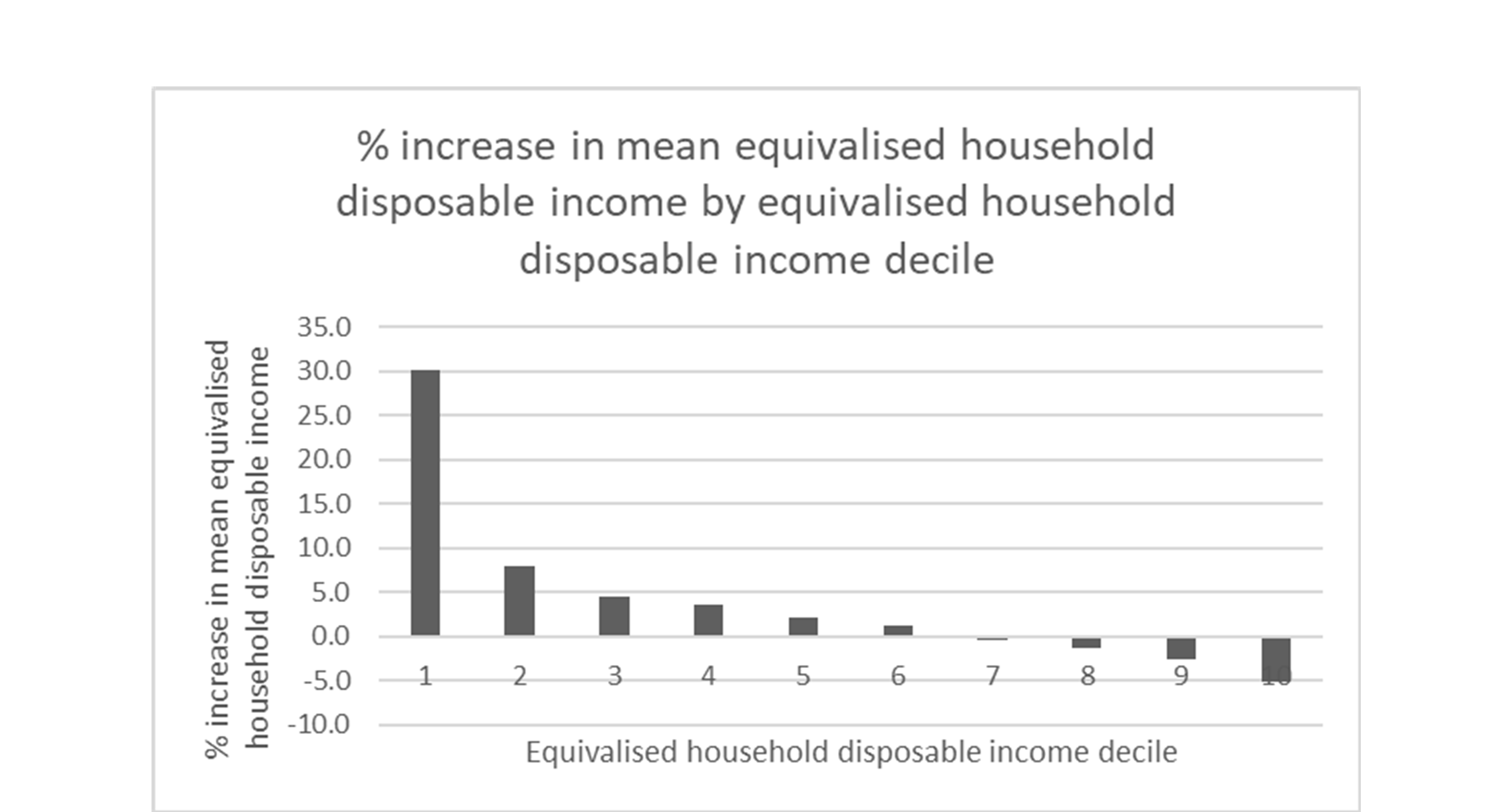

Table 8 shows the changes in mean household disposable income by decile groups, and also mean equivalised household disposable income by decile group, the latter taking account of the composition of the household.

Table 8: Mean (equivalised) income by decile groups

| Decile group | % change in mean household disposable income | % change in mean equivalised household disposable income |

| 1 | 29.95 | 30.11 |

| 2 | 7.69 | 7.97 |

| 3 | 4.2 | 4.45 |

| 4 | 3.25 | 3.58 |

| 5 | 1.87 | 2.14 |

| 6 | 0.91 | 1.13 |

| 7 | -0.48 | -0.42 |

| 8 | -1.43 | -1.4 |

| 9 | -2.51 | -2.55 |

| 10 | -5.14 | -5.25 |

Source: own calculations with EUROMOD version I.10+.

Figure 2 is a graphical representation of the redistribution pattern for equivalised household disposable incomes.

Figure 2

Source: own calculations with EUROMOD version I.10+.

We can see from table 5 that financial feasibility can be achieved, although at the cost of a far smaller increase in Child Benefit than for previous schemes: £5 rather than £20. Predictably, this means that the reduction in child poverty achieved by the £70 per week scheme is lower than for the £65 per week scheme. Other indicators look fairly similar, except that there are generally higher numbers of household net disposable income losses in most of the loss categories.

We can conclude that if for whatever reason a £70 per week Citizen’s Basic Income for working age adults was to be required, then a financially feasible scheme could be implemented.

2. How much would it cost to run a pilot project for a whole community for a genuine Citizen’s Basic Income of £70 per week for working age adults?

In a less developed country there is likely to be only a rudimentary existing benefits system, if any, and a rudimentary income tax system, if any. Establishing a Citizen’s Basic Income pilot project in such a context requires that the unconditional payments should be made to everyone in the chosen community or communities for the prescribed time period, and that the effects should then be evaluated, preferably in relation to control communities that have not received the Citizen’s Basic Incomes. In a more developed country, existing benefits and tax systems would need to be adjusted for the pilot community, because that is what would have to happen if a nationwide scheme were to be implemented. If that is not done, then the experiment will not be a genuine pilot project. The problem is that it is exceedingly difficult to alter complex tax and benefits systems just for pilot communities.

One possible solution (Torry, 2016) entails a roll-out to young adults entering the employment market at age 16 or thereabouts: in practice, providing Citizen’s Basic Incomes to a one-year or a three-year age cohort (or possibly to a six-year cohort). A further suggestion might be a pilot project for such a pilot project, because it would not be too difficult to establish a Citizen’s Basic Income for a one- or three-year age cohort of young adults in a single community, mainly because major changes to the existing tax and benefits systems could be avoided.

But having been asked whether it would be possible to run a pilot project for a genuine nationwide Citizen’s Basic Income scheme like the illustrative schemes researched in this paper, the question has to be answered. In an important sense, the answer has to be ‘no’, because to establish either the £65 per week or £70 per week illustrative schemes reported above would require major changes to the existing tax and benefits systems. This would not be feasible in a single community. However, something similar to a pilot project would be possible if it was conducted along similar lines to the pilot project for the single year age cohort project by operationalising those changes that it would be possible to operationalise and not those that would not be.

The plan would therefore be to provide Citizen’s Basic Incomes for all adults over the age of 16 at the same levels as in the £70 per week project reported above. Everyone in employment would then be allocated a BR (Basic Rate) tax code. [4] Child Benefit would not be altered, Income Tax rates would not be altered, and the thresholds and rates for National Insurance Contributions would not be amended, as all of those changes would be too difficult to achieve for a single community. Every household on means-tested benefits would have their Citizen’s Basic Incomes added to the means employed in calculating benefit claims, so everyone’s means-tested benefit claims would be reduced in value.

Microsimulation of the scheme generates the results found in table 9:

Table 9: The £70 per week Citizen’s Basic Income pilot project

| CBI levels, tax rates, numbers of losses over various limits for all households and lower quintile, and total net cost of scheme | |

| Citizen’s Pension per week (existing state pensions remain in payment) | £40 |

| Working age adult Citizen’s Basic Income per week | £70 |

| Young adult Citizen’s Basic Income per week | £60 |

| Education age Citizen’s Basic Income per week | £25 |

| (Child Benefit is not increased) | [£0] |

| Income Tax rate increase required for strict revenue neutrality | 0% |

| Income Tax, basic rate (on £0 – 46,350) | 20% |

| Income Tax, higher rate (on £46,350 – 150,000) | 40% |

| Income Tax, top rate (on £150,000 – ) | 45% |

| Proportion of households in the lowest original income quintile experiencing losses of over 15% at the point of implementation | 0.90% |

| Proportion of households in the lowest original income quintile experiencing losses of over 10% at the point of implementation | 1.16% |

| Proportion of households in the lowest original income quintile experiencing losses of over 5% at the point of implementation | 1.56% |

| Proportion of all households experiencing losses of over 15% at the point of implementation | 0.43% |

| Proportion of all households experiencing losses of over 10% at the point of implementation | 0.54% |

| Proportion of all households experiencing losses of over 5% at the point of implementation (losses over 6%: 0.70%) | 0.74% |

| Net cost of scheme | £56.56bn p.a. |

Source: own calculations with EUROMOD version I.10+.

Table 10 shows the changes in the numbers of households receiving a variety of means-tested benefits, and also the numbers of households brought within striking distance of coming off them.

Table 10: Reductions in numbers claiming means-tested benefits or within striking distance of coming off them, and the reductions in the totals costs of the benefits and the average value of claims

| Reductions in numbers claiming means-tested benefits or within striking distance of coming off them | The existing scheme in 2018 | The Citizens Basic Income scheme | % reduction |

| Percentage of households claiming out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 13.06% | 5.30% | 59.45% |

| Percentage of households claiming more than £100 per month in out-of-work benefits (defined as above) | 13.28% | 10.59% | 20.25% |

| Percentage of households claiming in-work benefits (Working Tax Credits and Child Tax Credits) | 13.06% | 9.71% | 19.66% |

| Percentage of households claiming more than £100 per month in in-work benefits (defined as above) | 5.81% | 5.09% | 12.41% |

| Percentage of households claiming Pension Credit | 4.95% | 3.95% | 20.11% |

| Percentage of households claiming more than £50 per month in Pension Credit | 15.76% | 15.00% | 5.05% |

| Percentage of households claiming Housing Benefit | 14.68% | 13.82% | 5.85% |

| Percentage of households claiming more than £100 per month in Housing Benefit | 21.19% | 18.97% | 10.48% |

| Percentage of households claiming Council Tax Benefit | 16.38% | 14.41% | 11.84% |

| Percentage of households claiming more than £50 per month in Council Tax Benefit | 32.86% | 28.52% | 13.22% |

| Percentage of households claiming any means-tested benefits | 28.98% | 23.77% | 17.96% |

| Percentage of households claiming more than £100 per month in means-tested benefits | 26.23% | 19.97% | 23.87% |

| Percentage of households claiming more than £200 per month in means-tested benefits | 13.06% | 5.30% | 59.45% |

| Reductions in total costs and average values of claims for means-tested benefits | Reduction in total cost | Reduction in average value of claim

|

|

| Out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 75.32% | 65.35% | |

| In-work benefits (Working Tax Credits and Child Tax Credits) | 24.80% | 5.71% | |

| Pension Credit | 34.12% | 28.80% | |

| Housing Benefit | 7.46% | 6.27% | |

| Council Tax Benefit | 13.31% | 9.30% | |

| All means-tested benefits | 33.74% | 25.53% | |

Source: own calculations with EUROMOD version I.10+.

Table 11 shows reductions in inequality and in poverty rates.

Table 11: Inequality and poverty indices

| Inequality and poverty indices | The current tax and benefits scheme in 2018 | The Citizen’s Basic Income scheme | Percentage change in the indices |

| Inequality | |||

| Disposable income Gini coefficient | 0.3087 | 0.2942 | 4.70% |

| Poverty headcount rates | |||

| Total population in poverty | 0.16 | 0.11 | 27.77% |

| Children in poverty | 0.18 | 0.13 | 25.85% |

| Working age adults in poverty | 0.15 | 0.11 | 29.66% |

| Economically active working age adults in poverty | 0.06 | 0.03 | 46.16% |

| Elderly people in poverty | 0.14 | 0.11 | 23.86% |

Source: own calculations with EUROMOD version I.10+.

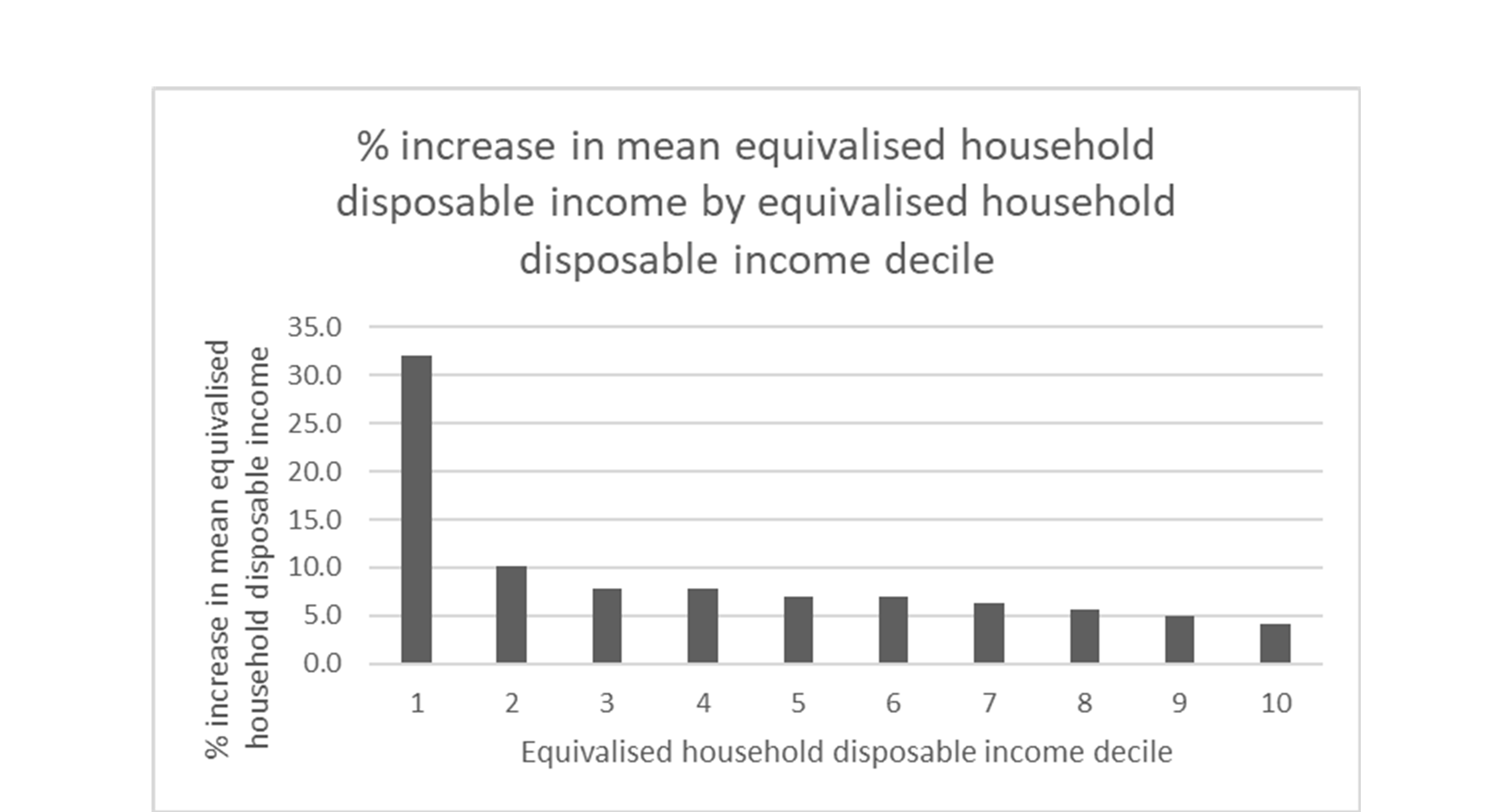

Table 12 shows the changes in mean household disposable income by decile groups, and also mean equivalised household disposable income by decile group, the latter taking account of the composition of the household.

Table 12: Mean (equivalised) income by decile groups

| Decile group | % change in mean household disposable income | % change in mean equivalised household disposable income |

| 1 | 32.17 | 32.02 |

| 2 | 10.01 | 10.1 |

| 3 | 7.71 | 7.79 |

| 4 | 7.48 | 7.84 |

| 5 | 6.68 | 6.96 |

| 6 | 6.7 | 7.01 |

| 7 | 6.02 | 6.23 |

| 8 | 5.46 | 5.62 |

| 9 | 4.83 | 4.94 |

| 10 | 4.04 | 4.13 |

Source: own calculations with EUROMOD version I.10+.

Figure 3 is a graphical representation of the redistribution pattern for equivalised household disposable incomes.

Figure 3

Source: own calculations with EUROMOD version I.10+.

From table 9 we can see that if this scheme were to be rolled out across the whole of the UK then the net cost would £56.56bn per annum. If the pilot project community population were to be 100,000, then the net cost would be £88m; and if the pilot community population were to be 10,000, then the net cost would be £8.8m. (The significant assumption made in this calculation is that the financial profile of the pilot community matches in all respects the financial profile of the country as a whole.)

The reason for the entire graph in figure 3 being above the horizontal, and there being a negligible number of household net disposable income losses reported in table 9, is because no household would be worse off with this scheme, because no National Insurance Contribution rates or Income Tax rates will have been increased. Hence the huge net cost if the scheme were to be rolled out nationwide. In that sense, the scheme is not financially feasible, so any pilot project of this nature would need to be evaluated in the knowledge that if the scheme were to be rolled out nationwide then Income Tax and National Insurance Contribution rates would have to change, imposing losses on some households.

All one can say about this project is that it is probably as close as it possible to get to a genuine Citizen’s Basic Income pilot project in the UK, and that although rolling out the scheme nationwide would not be financially feasible, the pilot project would be.

3. Would it be possible to construct a financially feasible Citizen’s Basic Income scheme that retained a small Income Tax Personal Allowance rather than reducing it to zero?

Rather than beginning with an arbitrary continuing Income Tax Personal Allowance, it seemed sensible to begin this exercise with a level of Citizen’s Basic Income in mind for working age adults. A reasonable assumption might be that a Citizen’s Basic Income of below £50 per week for working age adults might not be worth paying, might be difficult to argue for, and might not generate sufficiently robust effects if it were to be paid.

This leaves the question as to whether the National Insurance Contribution Primary Earnings Threshold should be positive, or reduced to zero as in the £65 and £70 nationwide schemes reported in this paper. There would be an argument for aligning it with the new positive Income Tax Personal Allowance, so that neither Income Tax nor National Insurance Contributions would be collected on earnings below a specified level. There would also be an argument for reducing the threshold to zero so that everyone earning an income was paying National Insurance Contributions, even if they were not paying Income Tax. The argument is that it would be useful to give to everyone earning an income a sense of ownership of the National Insurance system, and that it would enable them to build a genuine contribution record rather than have contributions credited. It is therefore the latter option – to reduce the Primary Earnings Threshold to zero – that this project chooses.

With the National Insurance Contributions Primary Earnings Threshold reduced to zero, a Citizen’s Basic Income of £50 per week for working age adults suggests a continuing Income Tax Personal Allowance of £4,000 per annum. [5]

For this exercise, the usual set of requirements for financial feasibility was employed. A financially feasible Citizen’s Basic Income scheme was discovered as described in table 18:

Table 13: A £50 per week Citizen’s Basic Income scheme with a continuing Income Tax Personal Allowance of £4,000 per annum.

| CBI levels, tax rates, numbers of losses over various limits for all households and lower quintile, and total net cost of scheme | |

| Citizen’s Pension per week (existing state pensions remain in payment) | £35 |

| Working age adult Citizen’s Basic Income per week | £50 |

| Young adult Citizen’s Basic Income per week | £40 |

| Education age Citizen’s Basic Income per week | £30 |

| (Child Benefit is increased by £10 per week) | [£10] |

| Income Tax rate increase required for strict revenue neutrality | 3% |

| Income Tax, basic rate (on £4,000 – 46,350) | 23% |

| Income Tax, higher rate (on £46,350 – 150,000) | 43% |

| Income Tax, top rate (on £150,000 – ) | 48% |

| Proportion of households in the lowest original income quintile experiencing losses of over 15% at the point of implementation | 0.38% |

| Proportion of households in the lowest original income quintile experiencing losses of over 10% at the point of implementation | 0.60% |

| Proportion of households in the lowest original income quintile experiencing losses of over 5% at the point of implementation | 0.73% |

| Proportion of all households experiencing losses of over 15% at the point of implementation | 0.35% |

| Proportion of all households experiencing losses of over 10% at the point of implementation | 2.27% |

| Proportion of all households experiencing losses of over 5% at the point of implementation (losses over 6%: 6.58%) | 8.38% |

| Net cost of scheme | £0.21bn p.a. |

Source: own calculations with EUROMOD version I.10+.

Table 14 shows the changes in the numbers of households receiving a variety of means-tested benefits, and also the numbers of households brought within striking distance of coming off them.

Table 14: Reductions in numbers claiming means-tested benefits or within striking distance of coming off them, and the reductions in the totals costs of the benefits and the average value of claims

| Reductions in numbers claiming means-tested benefits or within striking distance of coming off them | The existing scheme in 2018 | The Citizens Basic Income scheme | % reduction |

| Percentage of households claiming out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 13.06% | 10.19% | 21.95% |

| Percentage of households claiming more than £100 per month in out-of-work benefits (defined as above) | 13.28% | 11.34% | 14.56% |

| Percentage of households claiming in-work benefits (Working Tax Credits and Child Tax Credits) | 12.08% | 10.51% | 13.09% |

| Percentage of households claiming more than £100 per month in in-work benefits (defined as above) | 5.81% | 4.72% | 18.82% |

| Percentage of households claiming Pension Credit | 4.95% | 3.55% | 28.25% |

| Percentage of households claiming more than £50 per month in Pension Credit | 15.76% | 15.57% | 1.26% |

| Percentage of households claiming Housing Benefit | 14.68% | 14.36% | 2.18% |

| Percentage of households claiming more than £100 per month in Housing Benefit | 21.19% | 19.90% | 6.11% |

| Percentage of households claiming Council Tax Benefit | 16.38% | 14.76% | 9.87% |

| Percentage of households claiming more than £50 per month in Council Tax Benefit | 32.86% | 30.32% | 7.73% |

| Percentage of households claiming any means-tested benefits | 28.98% | 25.56% | 11.79% |

| Percentage of households claiming more than £100 per month in means-tested benefits | 26.23% | 21.21% | 19.15% |

| Percentage of households claiming more than £200 per month in means-tested benefits | 13.06% | 10.19% | 21.95% |

| Reductions in total costs and average values of claims for means-tested benefits | Reduction in total cost | Reduction in average value of claim

|

|

| Out-of-work benefits (Income Support, Income-related Jobseeker’s Allowance, Income-related Employment Support Allowance) | 56.84% | 40.01% | |

| In-work benefits (Working Tax Credits and Child Tax Credits) | 17.60% | 3.32% | |

| Pension Credit | 41.20% | 36.45% | |

| Housing Benefit | 3.97% | 2.73% | |

| Council Tax Benefit | 10.00% | 5.83% | |

| All means-tested benefits | 26.00% | 16.84% | |

Source: own calculations with EUROMOD version I.10+.

Table 15 shows reductions in inequality and in poverty rates.

Table 15: Inequality and poverty indices

| Inequality and poverty indices | The current tax and benefits scheme in 2018 | The Citizen’s Basic Income scheme | Percentage change in the indices |

| Inequality | |||

| Disposable income Gini coefficient | 0.3087 | 0.2776 | 10.09% |

| Poverty headcount rates | |||

| Total population in poverty | 0.16 | 0.12 | 26.17% |

| Children in poverty | 0.18 | 0.13 | 28.36% |

| Working age adults in poverty | 0.15 | 0.12 | 22.72% |

| Economically active working age adults in poverty | 0.06 | 0.04 | 31.75% |

| Elderly people in poverty | 0.14 | 0.09 | 35.30% |

Source: own calculations with EUROMOD version I.10+.

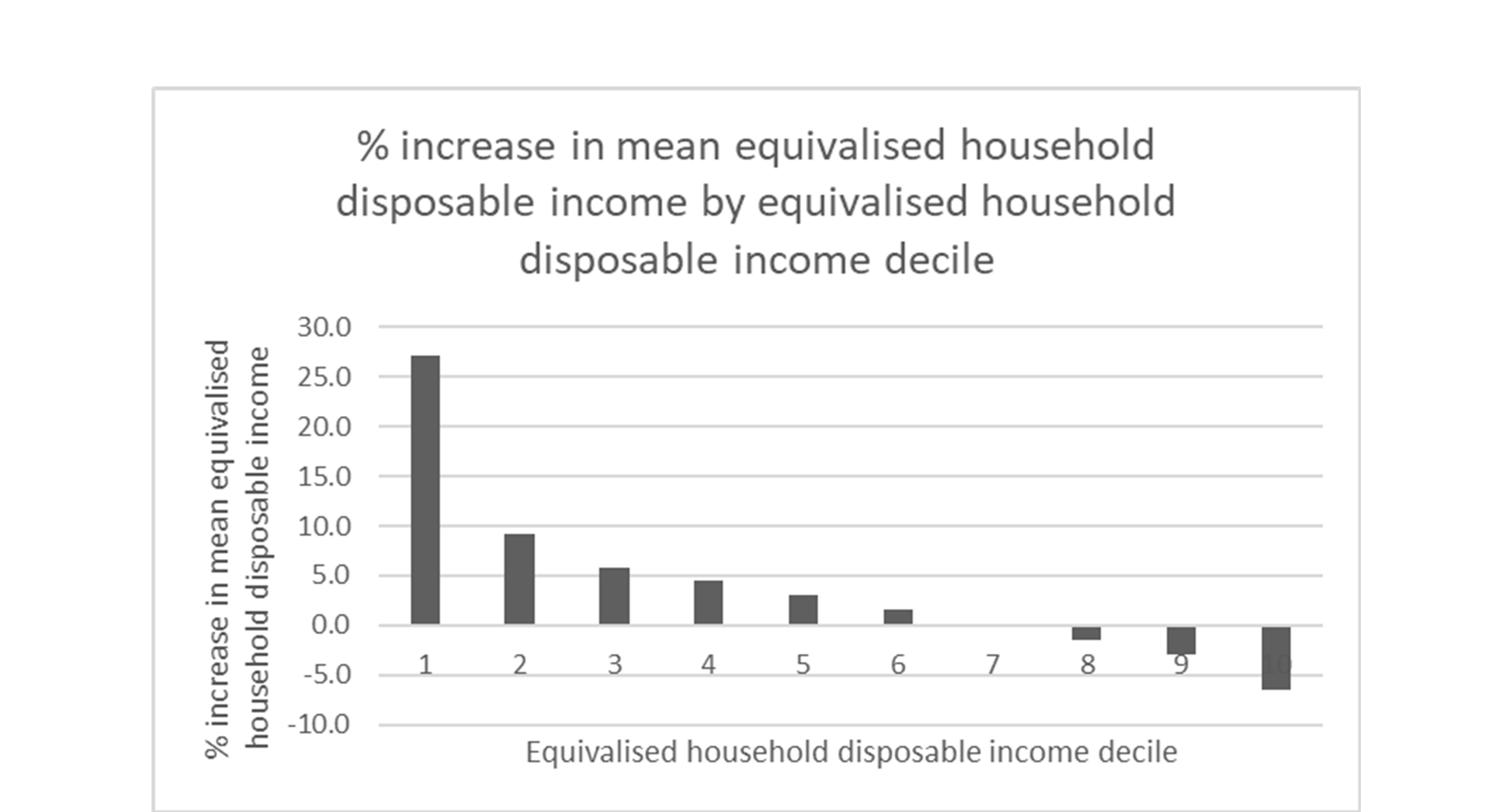

Table 16 shows the changes in mean household disposable income by decile groups, and also mean equivalised household disposable income by decile group, the latter taking account of the composition of the household.

Table 16: Mean (equivalised) income by decile groups

| Decile group | % change in mean household disposable income | % change in mean equivalised household disposable income |

| 1 | 26.84 | 27.1 |

| 2 | 8.87 | 9.13 |

| 3 | 5.52 | 5.73 |

| 4 | 4.17 | 4.42 |

| 5 | 2.74 | 2.96 |

| 6 | 1.42 | 1.56 |

| 7 | -0.27 | -0.26 |

| 8 | -1.46 | -1.5 |

| 9 | -2.90 | -3.02 |

| 10 | -6.33 | -6.46 |

Source: own calculations with EUROMOD version I.10+.

Figure 4 is a graphical representation of the redistribution pattern for equivalised household disposable incomes.

Figure 4

Source: own calculations with EUROMOD version I.10+.

We can see from the tables and graphs that an entirely feasible scheme has emerged that brings household net income losses below the levels found for other schemes researched here. If a £50 per week Citizen’s Basic Income for working age adults was felt to be a worthwhile starting point, then this feasible scheme could be rolled out fairly easily and would have useful effects.

4. Would it be possible to reduce the Income Tax rates required to fund a Citizen’s Basic Income scheme if the top rate of tax was raised to 70%?

The highest rate of Income Tax in the UK is currently 45% above a £150,000 per annum income threshold. At that point in the earnings range, National Insurance Contributions on additional earned income are paid at a rate of 2%, making a total tax rate of 47%. The Citizen’s Basic Income schemes researched for this paper assume that National Insurance Contribution rates will be at 12% across the entire earned income range: so in order for the total tax rate to reach 70%, Income Tax would have to be charged at 58% rather than 45%. If the other Income Tax rates were to be increased by 3 percentage points, as in the schemes researched for this paper, then instead of the net cost being £1.14bn per annum, there would be a net gain to the Treasury of £0.78bn per annum. This still coheres with our definition of strict revenue neutrality. If the other Income Tax rates were to be increased by 2 percentage points rather than by 3 percentage points, then there would be a net cost £8.3bn, which would be well outside our definition of strict revenue neutrality, and the scheme would no longer be financially feasible. We therefore have to conclude that raising the total tax rate for the highest earners to 70% would not enable the other Income Tax rates to be reduced, and so would not change the general patterns of results for the schemes researched for this paper. Raising the top total tax rate to 70% would unfortunately make almost no difference to the kind of Citizen’s Basic Income scheme that could be implemented.

5. What is causing the losses for low income households, and is it possible to reduce them?

We can hypothesise that one cause might be the fact that a household’s Citizen’s Basic Incomes have added to the means used to assess means-tested benefits claims, and if the household is on a number of different means-tested benefits, then several benefits might be being withdrawn at the same time, which means that the value of the Citizen’s Basic Income might be being withdrawn more than once at the same time. To test whether this might be at least part of the problem, a project that added only half of a household’s Citizen’s Basic Incomes to the means used to calculate Housing Benefit is reported on here.

Again, the usual set of requirements for financial feasibility was employed. A financially feasible Citizen’s Basic Income scheme was discovered as follows:

Table 17: The £70 per week Citizen’s Basic Income scheme and losses generated

| CBI levels, tax rates, numbers of losses over various limits for all households and lower quintile, and total net cost of scheme | 0.5 of Housing Benefit added to means | Housing Benefit added to means |

| Citizen’s Pension per week (existing state pensions remain in payment) | £40 | £40 |

| Working age adult Citizen’s Basic Income per week | £65 | £65 |

| Young adult Citizen’s Basic Income per week | £50 | £50 |

| Education age Citizen’s Basic Income per week | £40 | £40 |

| (Child Benefit is increased by £20 per week) | [£20] | [£20] |

| Income Tax rate increase required for strict revenue neutrality | 3% | 3% |

| Income Tax, basic rate (on £0 – 46,350) | 23% | 23% |

| Income Tax, higher rate (on £46,350 – 150,000) | 43% | 43% |

| Income Tax, top rate (on £150,000 – ) | 48% | 48% |

| Proportion of households in the lowest original income quintile experiencing losses of over 15% at the point of implementation | 1.02% | 1.23% |

| Proportion of households in the lowest original income quintile experiencing losses of over 10% at the point of implementation | 1.57% | 1.77% |

| Proportion of households in the lowest original income quintile experiencing losses of over 5% at the point of implementation | 3.49% | 3.71% |

| Proportion of all households experiencing losses of over 15% at the point of implementation | 0.36% | 0.41% |

| Proportion of all households experiencing losses of over 10% at the point of implementation | 1.66% | 1.74% |

| Proportion of all households experiencing losses of over 5% at the point of implementation (losses over 6%: 7.01% rather than 7.11%) | 12.20% | 12.54% |

| Net cost of scheme | £4.32bn p.a. | £1.41bn p.a. |

Source: own calculations with EUROMOD version I.10+.

As we can see, the household net disposable income losses are lower. However, as we would also expect, the total net cost of the scheme is higher, and the scheme is no longer strictly revenue neutral.

Whatever the problems that the UK Government’s new Universal Credit has encountered, one of its aims was laudable: to bring means-tested benefits together into a single benefit so that individuals would suffer a single taper rate rather than risk facing more than one at the same time. It is unfortunate that the localisation of Council Tax Support has meant that households can suffer the withdrawal of Council Tax Support at the same time as Universal Credit is withdrawn, but it is still likely that for many households a single taper rate might apply, which would make it easier to avoid household net income losses on the implementation of a Citizen’s Basic Income.

Other results for this scheme – such as the numbers leaving means-tested benefits – are not very different from those for the scheme tested at the beginning of this article, and so are not reported here.

Conclusions

We can conclude that nationwide UK schemes with the working age adult Citizen’s Basic Income set at either £65 or £70 would be feasible; that a pilot project with characteristics not entirely dissimilar to those schemes would be feasible; that it would be possible to maintain a positive Income Tax Personal Allowance of £4,000 per annum if a £50 per week working age adult Citizen’s Basic Income were to be paid; that there would no appreciable advantage to raising the total income tax rate to 70%; and that the replacement of legacy benefits by Universal Credit is likely to reduce the number of household net disposable income losses.

References

Hirsch, Donald (2015) Could a ‘Citizen’s Income’ work? York: Joseph Rowntree Foundation.

Torry, Malcolm (2016) Citizen’s Income schemes: An amendment, and a pilot project – addendum to EUROMOD working paper EM5/16. EUROMOD Working Paper EM5/16a. Colchester: Institute for Social and Economic Research, University of Essex.

Notes

[1] I am most grateful to Holly Sutherland, Matteo Richiardi, Alari Paulus, Cara McGenn, Iva Tasseva, Paola De Agostini, and all those from the Institute for Social and Economic Research who have given me considerable assistance with research and papers during the past fifteen years. In relation to this paper, I am particularly grateful to Alari Paulus for the trouble that he has taken to review its content and to make many useful suggestions for its improvement. The results presented here are based on EUROMOD version I1.0+ and on previous versions. EUROMOD is maintained, developed and managed by the Institute for Social and Economic Research (ISER) at the University of Essex, in collaboration with national teams from the EU member states. We are indebted to the many people who have contributed to the development of EUROMOD. The process of extending and updating EUROMOD is financially supported by the European Union Programme for Employment and Social Innovation “EaSI” (2014–2020). The results and their interpretation are the author’s responsibility. The UK Family Resources Survey data was made available by the Department for Work and Pensions via the UK Data Archive. The results and their interpretation are the author’s responsibility. Opinions expressed in this paper are not necessarily those of the Citizen’s Basic Income Trust.

[2] The calculation is as follows: Income Tax Personal Tax Allowance in 2018-2019 is £11,850. Removing the allowance would mean additional Income Tax of 11,850 x 0.2 = £2,370 being paid. The Primary Earnings Threshold for National Insurance Contributions is £162 per week. Reducing the threshold to zero would mean additional National Insurance Contributions of 162 x 52 x 0.12 = £1,010.88. The total additional payment would be 2,370 + 1,010.88 = 3,380.88, which translates as £65.02 per week: so a Citizen’s Basic Income of £65 per week would compensate for the loss of the Income Tax Personal Allowance and the reduction of the Primary Earnings Threshold to zero. This calculation assumes that the Basic Rate of Income Tax will remain at 20%, which of course it does not. This means that there will be losses for every household earning an income, because as the Income Tax rate rises – in this scheme it rises by 3 percentage points – the value of additional Income Tax and National Insurance Contributions will be greater than the amount received as a Citizen’s Basic Income. For families with children, this loss is more than compensated for by the increased Child Benefit that the scheme envisages. For households without children, the loss of £7 per week remains. Another scheme tested in this paper repairs most of this loss, but at the cost of a substantial drop in the increase in Child Benefit.

[3] A recent complexity is the fact that Scotland can now vary its Income Tax rates slightly, and it can also vary and add Income Tax thresholds – and it does. For the purposes of this exercise, and for the sake of simplicity, Income Tax rates have been harmonised across the UK at 23%, 43%, and 48%, and the thresholds have been harmonised, even though for narrow bands of earnings this requires a change of 4% rather than 3%. It should not be assumed that this is what would happen if a Citizen’s Basic Income scheme were to be implemented.

[4] A variety of possible consequences of doing this would need to be studied. For instance, in the normal course of events, if a BR tax code is applied throughout a tax year, then the Income Tax system will still assume that an Income Tax Personal Allowance should have been in place, and a tax refund will be issued. This would have to be prevented for the tax years relating to the pilot project. Similarly, how to handle earnings above the higher rate threshold and the top rate threshold would have to be discussed.

[5] The calculation is as follows: Reducing the NIC Primary Earnings Threshold (PET) to zero pays for a Citizen’s Basic Income of £162 (the PET) x 0.12 (the NIC rate) = £19.44 per week. A reduction in the Income Tax Personal Allowance (ITPA) therefore needs to pay for a Citizen’s Basic Income of £30.56 per week. Therefore the ITPA reduction x 0.2 (the Basic Rate of Income Tax) = 30.56 x 52 = 1589.12. Rearranging: the ITPA reduction = 5 x 30.56 x 52 = 7945.60. The continuing ITPA therefore needs to be 11,850 – 7,945.60 = 3904.40. For the sake of simplicity, the continuing Income Tax Personal Allowance is set at £4,000 per annum.