ABSTRACT

The defining characteristics of a Basic Income (BI), (universal, individual, unconditional, high enough), do not provide the full specification for a working scheme. The methods of monitoring, compliance and delivery, the source of funding, and the actual level(s) of the benefit must be specified. A BI scheme is a set of instruments, rather than a program of policy objectives. Depending on the other instruments with which it is coupled, it could fulfil a variety of welfare objectives.

The novel contributions of this paper are that:

a) it demonstrates how a BI scheme can be designed to fulfil a set of stated objectives according to given priorities, in this case:

- To redistribute income from rich to poor (and thus from men to women, and geographically).

- That the BIs should reflect the prosperity of the economy.

- To prevent poverty for financially-vulnerable adults and households with children.

- To reduce the incidence of financial poverty of all other working-age adults.

- To provide a method of calculating an approximate figure for the standard rate of income tax required to finance a particular scheme.

- To provide a benchmark, using Minimum Income Standards for the UK.

- To provide a Rule-of-Thumb for the BI levels, to enable quick calculations, and to use as an illustrative example.

- To restore incentives for those on Partial BIs (working age adults, who are not financially-vulnerable) to seek paid work.

- Ensure that the BI system does not lead to a downward spiral of the economy, and that economic cycles are stabilised.

b) it provides a simple, illustrative Rule-of-Thumb model, with Partial and Full BIs set at proportions 0.25 and 0.50 respectively of mean income per head of man, woman and child (Y-BAR). This simplifies the required calculations.

c) Table 1 provides a method of costing a BI scheme financed out of a new, restructured, hypothecated income tax system, which for the Rule-of-Thumb model would have a standard rate of 40%.

d) Current higher rate tax-payers would lose very little, (5% at the most, and decreasing with gross income), on the introduction of this BI scheme with a standard rate of income tax of 40%.

e) It also shows how to construct, develop and cost a progressive element to the income tax schedule (justified on both equity and efficiency grounds), by introducing an initial tax-free tranche of gross income for those who receive Partial BIs, until their net income schedule meets and merges with the Full BI schedule. This variation requires a higher standard rate of income tax.

f) It finds that there is a variety of potential levels for the Partial BIs, and the associated income tax rates on the initial tranche of income before the Partial and Full BI schedules meet and merge, without increasing the standard rate of income tax. This offers a remarkable degree of flexibility.

g)Keeping the BIs as fixed proportions of Y-BAR for the term of a government administration provides a self-stabilising mechanism for the economy, and the lagged effects in the system provide fiscal drag and reduce the amplitude of the economic cycles.

h) It demonstrates that even fairly generous BI schemes are economically feasible in the UK.

Disclaimer: This scheme is not necessarily the policy of the Citizen’s Income Trust.

Note: The terms ‘Basic Income’ (BI) and ‘Citizen’s Income’ (CI) will be used interchangeably.

SPECIFICATION OF BENEFIT AND INCOME TAX SYSTEMS

More than 40 delegates from 14 European countries have been contacting each other, and meeting together, on a regular basis since the autumn of 2011 to prepare, discuss and vote for the final draft of a ‘European Citizens’ Initiative’ (ECI) entitled ‘Unconditional Basic Income’ (UBI). It asks the European Parliament to do all in its power to speed up the introduction of a UBI in the European Union. The paper lists the defining characteristics of a BI as: 1. universal, 2. individual, 3. unconditional, and 4. high enough to meet one’s material needs, in order both to survive and to ensure a life of dignity, together with full participation in society. These represent the key characteristics that are necessary to define an income maintenance system as a Basic Income (BI) scheme, but by themselves do not describe a complete system. For instance, the methods of delivery of the BI, and of monitoring and compliance, and of course, the source for financing the scheme, must be specified. Further, the level(s) or amount(s) of the BI must also be stated. It is in the process of designing the greater system, that these basically simple concepts become part of a potentially complex and technical structure with ramifying consequences, both intended and unintended.

Different sources for funding a BI scheme have been suggested. These include Value Added Tax, the Tobin financial transactions tax, Land Value Tax, Resource Taxes (such as the Dividend from Alaska’s Permanent Fund), a carbon tax and other ‘green’ taxes. However, it is unlikely that any one of these alone could finance a generous enough BI scheme to replace even the current level of benefits in the UK. In the UK, the Citizen’s Income Trust has mainly concentrated on exploring funding via an income tax system. The benefit and income tax systems are reverse sides of the same coin, and it is appropriate to consider them together, and that the one should finance the other, providing a ‘velvet revolution or circulation of income’. The main features that must be addressed in order to define a benefit and income tax scheme are given below, indicating the particular features that are assumed for a Basic Income scheme.

A. Eligibility states who is entitled and on what basis. The current UK social security system comprises a Social Insurance scheme, where entitlement is according to a set of conditions being fulfilled (maternity, invalidity, sickness, unemployment or retirement) and a contribution record, and a means-tested Social Assistance scheme, which is meant to be a safety net for those in need, who are either deemed to be unable to work, or deemed able to work and are actively seeking work. A Citizen’s Income is inclusive of a whole population. Early debates centred on whether the levels of CI would be needs-based (which would lead to much monitoring and selectivity, losing its simplicity, and introducing an element of arbitrariness), or in the form of the same level of Social Dividend from the economy for everyone, on which it may, or may not, be enough to live. A compromise could provide a social dividend that is sufficiently generous to ensure that the needs of the majority of the population were met. The corollary is that some people would receive more than they actually need to survive. A CI would be universal to everyone who is legally resident in the UK, and would not be withdrawable.

B. Both the benefit and tax units for assessment, and for the receipt of the benefit and/or payment of taxes, will be the individual, and not a couple or household.

C. Contingency refers to whether pre-conditions must be fulfilled before the recipient becomes entitled to a particular benefit. The Basic Income will be unconditional. The right to the BI will not depend on any preconditions, such as an obligation to work, being involved in community service, or behaving according to traditional gender roles.

D. Selectivity refers to whether recipients receive different amounts of a benefit based on their personal circumstances. The Basic Income will be non-selective, (except that it could be age-related), and certainly would not vary by race, creed, gender, sexual orientation, marital status, cohabitation, household composition or past work record. Neither would the entitlement be means-tested on the recipient’s own income or wealth, nor on that of another member of the household or family.

E. The amounts of any benefits paid should be compared to an acceptable benchmark. The amount of the BI to be paid to every man and woman could be a Full BI, that would be enough for a single person to live on modestly, allowing participation in society, or a Partial BI, which would have to be topped up by other income, usually earnings, or a Child BI.

F. A benefit could be delivered in a variety of ways. The BI will be delivered automatically to those who qualify. It could be in the form of a regular gross payment to the account of a named single holder (as opposed to a joint account), including the responsible parent of a dependent child – as now. This is in contrast to a Negative Income Tax (NIT), (a transfer payment net of any lesser income tax due on gross income), or a Tax Credit (TC), (a tax payment payable on gross income net of any lesser benefit due). Some advocates favour a TC system because it is thought that it might make for an easier transition from the current system. The BI payment should be simpler, (and therefore cheaper to administer), than a NIT, TC or the current system, and should ensure that everyone can rely on receiving a regular, predictable income. It involves large gross-transfers of income within society, but the net amount transferred (the total amount of payments paid net by the tax payers, or the total income received by the net recipients) will be much less, and will depend on both the degree of inequality of gross incomes in society at the time and the degree of inequality of net incomes aimed at.

G. Monitoring and compliance. This includes maintaining a database on the population of citizens, as now. Since the CI system is much simpler, the number of data on each recipient would be much smaller, and thus the total database would be much smaller and cheaper to maintain. However, some monitoring would be necessary, to ensure that each citizen receives only one CI, that s/he is legally resident in the UK, and actually resides where s/he claims.

H. The income tax system must specify the sources of income to be taxed, and the structure of rates and thresholds, including personal allowances, tax reliefs and exemptions.

Appendix A provides a table of some recent basic figures about UK (population, GDP, mean income per head, sample BI levels, current means-tested benefit rates, and income tax thresholds and tax rates) used throughout this exercise, for calendar years 2007-2010, and fiscal years 2009-10 to 2012-13, together with their sources.

POTENTIAL OBJECTIVES:

The defining characteristics of a BI/CI scheme (universal, individual, unconditional, non-selective (except that it could be age-related) and high enough) can help to achieve several related objectives for welfare reform, depending on the level(s) of the BI(s), including the following:

I. Equality objectives:

- to value all individuals;

- to end dependence on past National Insurance contribution records;

- to remove the stigma and low take-up of means-tested benefits (MTBs), helping to create a more united and inclusive society.

II. Financial Security objectives:

- to help to reduce the incidence and depth of financial poverty;

- to contribute to financial security;

- to reduce the current time-consuming personal effort required to apply for benefits.

III. Labour Market objectives:

- to restore incentives to work-for-pay and labour market efficiency, by reducing the current high marginal deductions from potential earnings facing unemployed and low-paid workers who claim means-tested benefits, (by removing the aggregated benefit withdrawals that are currently added to income tax liabilities and National Insurance contributions);

- to give employees some countervailing power in the workplace;

- to give employees some choice over their type of employment.

IV. Administrative objectives:

- to introduce simplicity and transparency;

- to reduce administration and compliance costs.

V. Personal Choice objectives:

- to give financial privacy and autonomy to individuals;

- to give parents and other couples the choice of living together, or not;

- to help all individuals to achieve a better work-life balance;

- to help all individuals to develop to their full potential, leading to greater well-being, improved health, a reduction in crime, and a renaissance of the arts.

However, a Citizen’s / Basic Income by itself will not redistribute income, reducing income inequalities between rich and poor, men and women, and geographically. For this objective to be achieved, the BI scheme for the UK would have to be financed by a restructured income tax system.

Depending on with what other instruments it is coupled, a BI scheme can give rise to a wide variety of welfare systems. When planning a particular scheme, it is safer to start by defining the type of society that one is aiming to create, then specifying which objectives would help to bring about such a society, and finally designing a system that will achieve these objectives. There is no single optimum BI scheme. Each scheme put forward will represent a particular set of priorities for the objectives, and the proposed levels for the BIs, and the proposed method of financing them, will reflect this.

A BI SCHEME DESIGNED TO MEET SPECIFIED OBJECTIVES

In this paper, a modified BI system is explored, since initially it assumes only a universal Partial BI, (although some people will be entitled to be topped up to a Full BI). These tax-exempt BIs will replace most of the current National Insurance (NI) benefits and Means-Tested Benefits (MTBs). The system is then extended in order to address the following particular objectives:

- To redistribute income from rich to poor (and thus from men to women, and geographically).

- The BIs should reflect the prosperity of the economy.

- To prevent the poverty of financially-vulnerable adults and households with children.

- To reduce the incidence of financial poverty of all other working-age adults.

- To provide a method of calculating an approximate figure for the standard rate of income tax required to finance a particular scheme (and thus summarising the cost of a particular scheme in terms of a single figure).

- To provide a benchmark using Minimum Income Standards for the UK.

- To provide a Rule-of-Thumb for the BIs to enable quick calculations, and to use as an illustrative example.

- To restore incentives to work-for-pay for working age adults on Partial BIs.

- Ensure that the BI system does not lead to a downward spiral of the economy, and that economic cycles are stabilised.

1. In order to redistribute income from rich to poor, the BI scheme will be financed by a new, restructured, hypothecated, proportional (flat-rate) or progressive income tax system, still based on the individual, (replacing both the current UK income tax and employees’ National Insurance contributions systems), with the following properties:

a. There will be no personal allowances, tax reliefs or exemptions, (tax loopholes which enable legal tax avoidance to occur, and which subsidise the wealthier sections of the nation);

b. The same rate of tax will be levied on all sources of income: wages and salaries from full-time and part-time employment, earnings from self-employment, share schemes and options, company perquisites (perks), pensions, interest and dividends, capital gains, rental income and gifts.

The fact that the income tax system is hypothecated and is used to finance only the transfer payments and associated expenditure, implies that it will be simple, introducing transparency, and therefore accountability. It also implies that there will be a standard rate of income tax that will be required to finance the BI scheme, together with a margin for administration, a safety net, costs of disabilities, and other associated costs. It also implies that all government expenditure, (as opposed to transfer payments), will be funded out of the revenue from other income and expenditure taxes. This is feasible in the UK.

Redistribution from rich to poor will also bring about redistribution from men to women within a household, and from areas of the country that are thriving to those that are deprived. This latter could help to regenerate economically deprived areas and, in time, build up the national economy so that the UK is less dependent on imports and exports.

2. The amount of the BIs should reflect the prosperity of the economy. In spite of the inadequacies of GDP as a measure of economic activity, expressing the Full, Partial and Child BIs for each country as proportions of GDP per capita, based on the most recent figures available, would enable international comparisons to be made as to the generosity of a particular scheme. However, in order to calculate the cost of the scheme in terms of a flat-rate income tax, the BIs would have to be expressed as proportions of average (mean) income per capita, Y-BAR, of man, woman and child, based on the most recent figures available. In the UK, this would be for the calendar year ending fifteen months before the intended benefit period or fiscal year. (A Y with a bar across the top is a common symbol for mean income). Mean income per head amounted to between 74 and 77% of GDP per head in the years 2007 – 10 and was declining. The sources of the difference between GDP at market prices (series YBHA) and ‘Total Resources of Households and Non-Profit Institutions Serving Households’ (series QWMF) can be examined by a comparison of Table 1.2 (income component method) and Table 6.1.3 of the UK National Accounts, (The Blue Book). The major item is ‘Taxes on production and imports (series NZGX), less subsidies ( – series AAXS)’.

3. To prevent poverty in financially-vulnerable adults and households with children: the financially vulnerable adults are groups that in a compassionate society would not be compelled to top up a Partial BI with earnings, and so will receive an extra amount of BI to make up their Partial BI to a Full BI, which the recipients could increase further with earnings, if they wished. Financially-vulnerable adults will comprise people above pension-entitlement age, those with disabilities, unpaid designated carers-of-last-resort, and the responsible parent of a dependent child (aged 0-15 inclusive, in the UK). These are not necessarily mutually exclusive groups. The financially-vulnerable groups would not receive their top-ups on account of desert or worth, ie because they are more deserving, but merely on the practical basis that it is usually more difficult for these groups to gain access to the labour market on equal terms with the other working-age adults. People with disabilities will receive tax-exempt payments to cover the costs of their disabilities (for care, mobility, special equipment, special diets, extra fuel, extra laundry, etc.), in addition to their Full BIs.

4. To help to reduce the incidence of financial poverty of all other adults of working-age: they will receive their Partial BI, and would be expected to top it up with earnings, but a safety net (probably of an individualised, means-tested, unified Housing-and-Council-Tax-Benefit) would have to be retained for those who were in economically depressed areas, where there was a shortage of paid work, and for those in other areas who were unable to find suitable paid employment.

5. To provide a method of calculating an approximate figure for the standard rate of income tax to finance a particular BI scheme (and thus summarising the cost of a particular scheme in terms of a single figure).

Table 1 below illustrates the method that can be used to estimate an approximate figure for the rate of income tax that would have been required to finance a given Basic Income scheme. It is based on the 2010 figures for population and income (Total Resources of Households and Non-Profit Institutions Serving Households). Column 2 gives the figures (or estimates from other sources) for the different sections of the population, which are expressed as proportions of the total population for the UK in column 3. Let the Partial and Full BIs be expressed as given proportions of Y-BAR, and let the Y-BAR figure from 2010 (£17,288 pa) be used to calculate the Partial and Full BIs to be distributed in the fiscal year 2012-13.

Table 1 below illustrates a simple version where Partial BI = Child BI = 0.25 of Y-BAR, and Full BI = 0.50 of Y-BAR from 2010. The proposed proportions of Y-BAR for the BIs are noted in column 4. Columns 5 and 6 contain the amounts that the FBI, PBI and CBI represent in annual and weekly figures, (which would then be implemented in the fiscal year 2012-13). The product of columns 3 and 4 is noted in column 7. The fifth row of column 7 gives the cost for the whole population, man, woman and child to receive a Partial BI of 0.25 of Y-BAR, and this gives a base figure for the income tax rate of 25%. On each of the subsequent rows, the extra amount that each of the groups who receive a Full BI contributes to the required total income tax rate, (or the amount that could be deducted by giving less to children, as is often proposed in CI schemes), can be easily calculated and is noted in column 7. This also makes it easy to calculate the cost of increasing or decreasing a BI for a particular group. The table could have been laid out differently, giving each group a separate row. The figures in column 7 are added to give the TOTAL.

A figure has been added to estimate the payments required to cover the cost of disabilities, and a margin has been added to cover administration costs and a safety-net: for those in poverty, in spite of the BI scheme; to cover a residual National Insurance scheme for those not eligible for a BI in UK (ie. those living abroad); to provide a social fund for emergency payments. The flat-rate tax required to finance this scheme would be 40%.

6. To provide a benchmark, using Minimum Income Standards. An early official benchmark was based on 0.6 of average earnings. However, earnings are difficult to define: whose earnings are used to define the population, does it include that of part-time workers and over-time workers, those who are currently out of work, or those who have never worked? This was then replaced by 0.5 of average income. However, the current official poverty benchmark for the European Union is given as 0.6 of the national median net household equivalent income, which was found to be almost co-incidental with 0.5 of average income. This is a very confusing benchmark. The first point is that the ‘net household equivalent’ implies that it has already been decided what the equivalent amounts for members of the household should be, and that those household members had access to the incomes with which they are imputed. It can be very difficult to find out exactly how this benchmark has been calculated, and different teams seem to use different methods. It is not at all transparent. As a benchmark for a BI scheme, based on the individual, the only relevant figure to use would be 0.6 of median gross income, where median income had been calculated from the distribution of the gross (pre-tax-and-benefit) non-equivalised incomes of all the individuals in the country, at the point where there are as many individuals receiving more than the median income, as those below it, including those with zero gross incomes.

TABLE 1. PERSONAL INCOME TAX RATE: QUICK-CALCULATOR TABLE

SUMMARY OF THE INFORMATION REQUIRED TO ESTIMATE THE PERSONAL INCOME TAX RATE WHICH COULD FINANCE A BASIC INCOME SCHEME, SHOWING THE EXTRA COSTS OF FULL BASIC INCOMES FOR SOME.

[table id=17 /]

Note: The data for 2010, (the most recently available figures), were abstracted from the following sources:

* Mid-year population estimates for 2010 were obtained from: www.statistics.gov.uk/statbase/Product.asp?vlnk=15106.

** ‘Total Resources of Households and Non-Profit Institutions Serving Households’, 2010, (QWMF), = £1 076 419 m. (Blue Book 2011, Table 6.1.3).

Thus, mean gross income (Y-BAR) = £17 288 pa; multiplying by 7/365 = £331.55 pw,

Disability benefits, 2010, (series EKY6) = £12,779 m, would add about 0.012 to the tax rate, (Blue Book 2011, Table 5.2.4S).

To access the UK National Accounts, the Blue Book, follow the instructions in the bibliography.

Note: the proportion of non-financially-vulnerable, working-age adults in the population is c. 0.38.

In 2006, the Family Budget Unit at York University and the Centre for Research in Social Policy at Loughborough University combined resources to produce a set of Minimum Income Standards (MIS), funded by the Joseph Rowntree Foundation. Its final report, Minimum Income Standards, was launched in July 2008. It is based on 39 focus groups, involving more than 200 people, in combination with input from experts in heating and nutrition. It established the income levels required in 2007 to provide Low Cost but Acceptable (LCA) standards of living for 13 different household configurations. Table 2, column 1, presents this information.

TABLE 2. MINIMUM INCOME STANDARDS (2007) AND BASIC INCOME LEVELS (2009-10) FOR DIFFERENT HOUSEHOLD TYPES

[table id=18 /]

LP = Lone Parent, A = Adult, T = toddler, PRE = Pre-school child, P = Primary school child,

S = Secondary school child, HB = Housing + Council Tax Benefits.

PBI = Partial Basic Income; FBI = Full Basic Income; CBI = Child Basic Income.

Bold shows those households receiving only a PBI, which does not meet MIS standards.

Italic shows households that gain disproportionately from the CI scheme.

* Source: Minimum Income Standards, 2008, gives incomes for 2007; excludes child-care cost.

** Source: ‘Benefit and Pension Rates, April 2009, BRA5DWP, from www.dwp.gov.uk/ These give Pensioner Credit levels, income-based Job Seeker’s Allowance for those aged 25 and over, adding £56.11 for each dependent child, and a family or Lone Parent premium of £17.30 pw, where relevant. It is assumed that all Means Tested Benefits lead to HB entitlement.

Initially printed in Miller, Citizen’s Income Newsletter, 2009/1, p.9.

Using this new benchmark, a simple BI scheme for the benefit year 2009-10 was designed (Miller, 2009), which would provide a Full BI for financially-vulnerable adults, a Partial BI for other adults of working age, and a Child BI, which enabled all financially vulnerable adults and all households with children, (whether headed by a single parent or by two parents) to attain their LCA income. Each parent would receive a BI that is independent of whether they are living with or without another adult. (The present benefit system, based on joint applications, penalises parents who live together). The amount for each BI was then expressed as a proportion of mean income per head of man, woman and child (Y-BAR) for the calendar year 2007, (Office of National Statistics, Blue Book, 2008 edition). The proportions for the FBI, PBI and CBI came to 0.56, 026 and 0.26 of Y-BAR respectively. Unexpectedly, the PBI and CBI came to the same amounts. Comparing column 5 with columns 1 and 6 of Table 2 reveals how successful the scheme is at meeting the objectives of protecting financially-vulnerable adults and households with children.

7. To provide a rule-of-thumb to enable quick calculations, and to use as an illustrative example.

The first rule of thumb provides that the Partial BI and Child BI are equal, (and this gives the basis for a Partial BI for everyone), and that the Full BI is twice the Partial BI. But, what should be the amounts for the BIs, and at what rate of income tax?

Using the method in Table 1, the required income tax rates were calculated for a range of BI schemes, where the Full BI lay between 0.30 and 0.60 of Y-BAR. (Table 3 gives part of these results, which also includes the original MIS-based scheme. The Full BI = 0.55 and Partial BI = 0.275 Y-BAR matched up with it very well). The added margin diminished as the scheme became more generous, on the assumption that the need for the safety net would become less as the scheme became more generous. The corresponding required tax rates lay between 0.28 and 0.46.

On examining the amounts of the BIs and the corresponding tax rates, it was found that the range for the FBI of 0.45 < FBI < 0.55, with 0.225 < PBI < 0.275, gave feasible values for the BIs. In other words, the amounts of the BIs should be within this range. The corresponding income tax rate, t, would be 0.37 < t < 0.43. Table 3 also shows which households would receive more than their Minimum Income Standard, and which ones would receive less, for the different levels of Basic Income. It was noted that the scheme where FBI = 0.43, PBI = 0.215 Y-BAR and t = 0.35 matches up with the amounts for the means-tested Pension Credit and the Jobseeker’s Allowance chosen by the Department of Work and Pensions for the 2012-13 fiscal year in the UK. The approach taken here is for the Full BI for the financially-vulnerable groups to be sufficiently high so that the majority of them can meet their needs, but the corollary of this is that others may receive more than they strictly need. Those receiving only a PBI would only be able to live on it by topping it up via earnings, or by living within a family, or by receiving a Housing-and-Council Tax Benefit.

TABLE 3, SHOWING THE BI ENTITLEMENTS FOR 13 HOUSEHOLD TYPES WITH 9 DIFFERENT BI LEVELS EXPRESSED AS PROPORTIONS OF Y-BAR, COMPARED WITH THEIR ‘MINIMUM INCOME STANDARDS’ BENCHMARK, Col.2

[table id=19 /]

LP = Lone Parent, A = Adult, T = toddler, PRE = Pre-school child, P = Primary school child, S = Secondary school child,

* excludes child-care cost

Bold shows those households purely on PBI, which does not meet MIS.

Italic shows households that gain disproportionately from the CI scheme.

§ shows where the BI is closest to the MIS benchmark.

Margin includes: safety net, costs of disabilities, administration costs, etc.

Tax rates calculated on 2010 population figures.

The column for Full BI = 0.43 of Y-BAR and Partial BI = 0.215 of Y-BAR matches up with Pension Credit (£142.70 pw for those over pension entitlement age), and Jobseeker’s Allowance/Employment and Support Allowance (£71.00 pw) introduced in 2012-13.

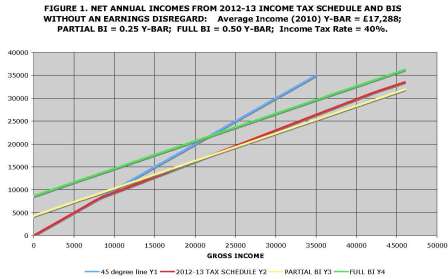

A second rule of thumb proposes that the Full, Partial and Child CIs are 0.50, 0.25 and 0.25 of average income per head (Y-BAR) respectively, and that these amounts can be used for illustrative purposes and has the extra advantage of providing easy calculations. The calculated tax rate was 40%. The graph of net income plotted against gross income gives two parallel lines with an inclination of 0.60. (See Figure 1) A recipient of the higher Full BI in 2012-13 would not become a net tax-payer until a gross annual income of £21,610 is reached, and s/he will have a greater net income than under the single person’s current income tax schedule for 2012-13, over the whole range of gross income. A recipient of the lower Partial BI becomes a net tax-payer at a gross income of £10,805 and becomes worse off compared with the 2012-13 income tax system, at a gross income of £21,613. These BIs are slightly less than those devised from the benchmarks provided by the Minimum Income Standards for those with no source of income other than their BI. The downside of proposing this rule of thumb is that, if one relaxes the benchmark of the MIS, then there is a temptation for others to reduce the levels even more.

While an income tax rate of 40% might sound quite high, it is economically feasible. Those above the higher rate tax threshold have already been paying a slightly higher Marginal Deduction Rate (effective income tax rate) than this in 2011-12 and in 2012-13, (40% income tax plus 2% employees’ National Insurance contributions on gross incomes of £42,475 or more). On the other hand, many people on means-tested-benefits, who are trying to earn their way out of poverty, not only have to pay income tax of 20% and National Insurance of 12%, but often face multiple benefit-withdrawal rates leading to a Marginal Deduction Rate of nearly 96%. The proposed introduction of a new Universal Credit system in 2013 aims to reduce these levels to 76 and 65%, depending on whether one’s income is above or below the personal allowance (income tax threshold) respectively. The greater reduction in Marginal Deduction Rates for people on low incomes from 96% to only 40% in this BI scheme is a major achievement, and most of those people will be materially better off with this BI scheme than under the present system, especially with the retention of a residual Housing Benefit scheme.

A non-financially-vulnerable, working-age person would have lost only £1,669.60 in net income at the current higher income tax threshold (£42,475 in tax year 2012-13), if this BI had been introduced, (retaining £31,476.60 under the current 2012-13 income tax schedule, and £29,807 with the Partial BI). This represents a loss of 0.053 of his/her net income. As his/her gross income, Y, increases, the loss = £31,476.60 + 0.58(Y – £42,475) – (£29,807 + 0.60(Y – £42.475)) = £1,669.60 + (0.58 – 0.60) (Y – £42,475), and decreases as gross income Y increases, until gross income Y = £83,480 + £42,475 = £125,955, when one becomes better off under the Partial BI scheme than the current tax system. Higher rate tax-payers would lose very little on the introduction of this BI scheme with a standard rate of income tax of 40%. In fact, at this rate of income tax it is quite difficult to ensure that they do not benefit unduly from the introduction of a universal BI that is paid to the wealthy. This counter-intuitive outcome can most probably be best described as equivalent to the current tax expenditures, that occurred on account of the tax loopholes, being ‘reclaimed’ by the tax authorities and distributed more equally among the wealthier section of the population in the form of a BI.

Even a proportional tax linked with a BI scheme can be very redistributive. For instance, it can be shown that for a skewed distribution of gross income with a given Gini coefficient (a measure of inequality of a distribution that can take values between 0 (equally distributed) and 1 (the most unequal that it can be)), a proportional income tax rate of t = ß, where 0 < ß < 1, coupled with a BI = ß.Y-BAR, yields a net income distribution with the Gini coefficient reduced by ß.

This costing method has the advantage of providing a single figure to summarise the gross cost. A progressive tax schedule will redistribute income to an even greater extent, but it is much more difficult to calculate its gross cost, because it usually requires information about the distribution of the gross income. Costing a proposed BI scheme based on a proportional tax would not preclude a government of the day from implementing a progressive income tax system when the time came. However, a flat-rate tax might reduce the opposition to a BI scheme from current and aspiring higher-rate taxpayers.

8. To restore incentives to work-for-pay, via an earnings/income disregard, for adults of working age who are not financially-vulnerable and who are receiving Partial BIs.

One of the strange effects of any BI scheme which includes both a FBI and a PBI, and where every one pays the same rate of tax on all other sources of income, is that the graph of net income plotted against gross income reveals the two schedules to be parallel lines over the whole range of gross income. (See figure 1.) This implies that, at any given gross income, a financially-vulnerable adult will always require the same amount extra of net income than any other working-age adult receiving a PBI. Yet, on both equity and efficiency grounds, it would be preferable for there to be an earnings/income disregard (EDR) (zero tax-rate) for each person receiving the Partial BI, until his/her net income schedule meets and merges with the Full BI schedule. This introduces an element of progressivity into the Partial BI tax schedule. Since this second, more progressive, Partial BI schedule foregoes all of the income tax revenue from the first tranche of income, it is more expensive to finance. In fact, it can be almost as expensive as granting a Full BI to all adults.

Let us assume that there is a BI scheme, comprising a Full BI = ßF.Y-BAR for all N adults, requiring a standard rate of income tax of tF. Then the scheme is modified, and C adults, C < N, receive a Partial BI = ßP.Y-BAR, where ßP < ßF. An income tax rate, tP, where 0 < tP < tF, is levied on the first tranche of their gross income, until the Partial BI income tax schedule meets and merges with the Full BI schedule, where gross income is Yo.

(1) Full BI + (1 – tF).Yo = Partial BI + (1 – tP).Yo

Yo = (Full BI – Partial BI) / (tF – tP)

Yo = (ßF – ßP)Y-BAR / (tF – tP).

(2) The gross amount saved by granting only a Partial BI to C individuals is,

Amount saved = (Full BI – Partial BI) x number of recipients receiving the Partial BI

= (ßF – ßP) Y-BAR x C.

(3) The actual income tax revenue foregone, by the introduction of the Partial BI and lower tax rate on the first tranche of income, is the difference between the sums of the tax revenue foregone on incomes, YiF, at income tax rate, tF, and that gained from the incomes, YiP, taxed at the new rate tP, summed over the Partial BI population, i = 1, 2, … C. Both the lower BI, and the lower tax rate, tP, should provide incentives for people to increase their hours of work-for-pay, that is: 0 ? YiF ? YiP ? Yo and total output could increase as a result.

Actual income tax revenue foregone =

The limiting case occurs where YF = YP = Yo, for all i, which is the maximum tax revenue foregone.

Actual tax revenue foregone is less than or equal to maximum tax revenue foregone.

(3a) Maximum income tax revenue foregone

= (tF – tP).C.Yo

Substituting for Yo = (ßF – ßP)Y-BAR / (tF – tP) from equation (1) gives

Max tax revenue foregone

= (tF – tP) x {(ßF – ßP).Y-BAR / (tF – tP)} x C.

= (ßF – ßP) Y-BAR x C.

Equations (1), (2) and (3a) imply that, the amount saved by granting a lower BI to some people will equal the maximum possible tax revenue foregone on the first tranche, Yo, of their Partial BI income tax schedule, where the Partial and Full BI schedules meet and merge, and this is true for any combination of ßF > ßP , and is not dependent on the difference in the two tax rates.

The fact that the actual tax revenue foregone is less than or equal to maximum revenue foregone, implies that the actual required standard income tax rate to fund the scheme will not be more than the initial required tax rate, tF, and could even be less, depending on the distribution of the incomes 0 ? YiF ? YiP ? Yo,, over the first tranche.

These two statements are quite powerful in practical terms. One of the potential weaknesses of the rule-of-thumb BI scheme put forward here is that the Partial BI = 0.25 Y-BAR could leave some working-age adults in poverty. The conclusion above means that a higher level of Partial BI could be granted, with either a zero or a positive tax rate, (tP < tF), and according to equations (1), (2) and (3a), it will cost the same in terms of the maximum gross transfer bill, or less in terms of the actual gross transfer bill. See Table 4 below for some examples. However, The effects on households of increasing the Partial BIs should be examined by comparing them with the Minimum Income Standards presented in Table 2.

Note, even a proportional tax linked with a BI scheme can be very redistributive. However, a progressive tax schedule will redistribute income to an even greater extent. Having a zero tax rate on the initial tranche of gross income introduces a simple method of making the income tax schedule progressive for at least some people.

Table 4. Examples of different Partial BIs and income tax rates, tP, that are possible, while levying a standard tax-rate, tF = 0.50, (tP less than or equal to tF).

[table id=20 /]

For the Rule-of-Thumb example, the product of the proportion (approximately 0.4) of the total population who receive a PBI, multiplied by an increase in the PBI to a FBI (0.25 Y-BAR) is 0.10 Y-BAR, which added to the previous income tax rate of 0.40 Y-BAR, implies that this BI scheme could be financed adequately by an income tax rate of 50%, (tF = 0.50), which is probably the maximum that the UK could stomach as the standard rate of tax. (See Table 3 above)

Equation 1) above gives

Yo = (ßF – ßP)Y-BAR / (tF – tP)

Substituting for ßF = 0.50, ßP = 0.25, tF=0.5 and tP=0

Yo = (0.50 – 0.25) Y-BAR / (0.5 – 0) = 0.5 Y-BAR

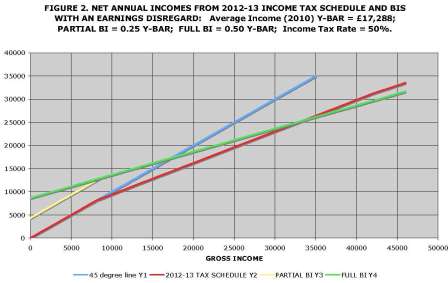

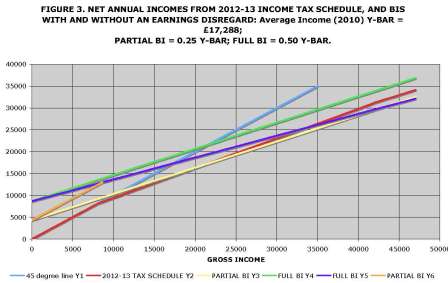

The key features of this illustrative Rule of Thumb BI scheme are very easy to work out. The Full and Partial BI schedules will meet when gross income, Yo, reaches 0.5 of Y-BAR, at which point, net income will be 0.75 of Y-BAR. A working-age adult receiving a Partial BI will only start to pay income tax when his/her annual gross income exceeds 0.5 of Y-BAR. Further, no adult will become a net income tax payer until his/her income is greater than Y-BAR. (See Figure 2. Figure 3 combines figures 1 and 2.) Almost all of those with a gross income less than £33,613, (which is almost twice Y-BAR from 2010), would be better off with the BI scheme than under the current 2012-13 income tax schedule.

Might this be a simple but useful way to define the richer and poorer sections of the nation: a ‘poorer’ person is one who receives a net benefit, while a ‘richer’ person is one who pays net income tax, ie. defined by whether their gross income is less or greater than Y-BAR? This is distinct from the super 1% richest of the population, or even the top 10%.

If this BI scheme had been introduced, then at the higher income tax threshold (£42,475 in 2012-13), the loss experienced by a tax-payer would be: loss = £8,105 + 0.68 (£42.475 – £8,105) – (£8,644 + 0.50 (£42,475)) = £1,595.10. This represents 5% of his/her net income. As gross income, Y, increases, the loss = £31.476.60 + 0.58 (Y – £42,475) – (£29,881.50 + 0.5 (Y – £42,475)) = £1595.10 + 0.08 (Y – £42.475) and it increases as gross income increases.

At a gross income of £100,000, the loss is £6,197.10, or 9.6% of net income. At a gross income of £100,000, the personal allowance (£8.105) is withdrawn at a rate of 50%. An additional tax amounting to 50% is levied at the threshold of £150,000. However, this is merely a short-term situation, since the UK government plans to cut the additional tax to 45% in the tax year 2013-14.

Again, an income tax rate of 50% to finance the BI scheme may seem high, but it is still much lower than the current marginal deduction rates (MDRs) facing those who try to return to work while receiving means-tested benefits. A reduction of the MDR from nearly 96% to 0% on the first tranche of income (of 0.5 of Y-BAR) for those receiving a PBI is a major achievement. Those who are currently expected to pay “the additional income tax rate” of 50% (plus 2% National Insurance on earnings), could hardly demur at paying 50%, if all citizens, except the poorest working-age adults, paid the same rate. A universal, non-stigmatising BI scheme based on citizenship (rather than need), and a common tax rate will help to create a very inclusive society. Income tax at 50% is the price for creating and maintaining a compassionate, inclusive and harmonious society. It is analogous to “One hand for the ship and one hand for oneself”. Again, this rate might sound very high, but if the idea is repeated often enough, it becomes more familiar, acceptable and realistic.

It is often claimed that most people would not be prepared to pay a high marginal income tax rate (of 50%) by choice. But, might they do so, if they could be convinced that they will be better off? In the 2010-11 fiscal year, (the latest year for which income tax figures are available), some 300,000 people paid the additional income tax rate of 50%, and about 4 million paid the higher rate tax. Just to give an approximate figure, roughly another 28 million people were standard rate tax-payers, with gross incomes of between £6,475 and £43,875. About 4/5 of the way along this range is the point where people would have become worse off under the BI scheme at a gross income of £36,620 in 2010-11, so perhaps another 6 million standard rate tax payers would be worse off, (but for some, other members of their families could be better off, leaving themselves with more in their own pockets). It is possible that, given the extremely skewed nature of the gross income distribution in the UK, only about 10 million people out of 50 million potential voters would have been worse off in 2010-11, with the rule-of-thumb BI model described above, and some, possibly many, might be prepared to accept a higher income tax rate, if they thought that it would help to create a fairer, more inclusive society in which they themselves and their loved ones, especially financially insecure younger members of their families, could benefit.

Of course, the question also arises as to whether children receiving their Partial or Child BI should also be entitled to the earnings / income disregard, thus allowing them to earn from paper rounds or Saturday jobs without having to submit tax returns. There are two differences between children and adults being entitled to a tax-free tranche: (i) the income of children in aggregate is negligible, and so, therefore, is the income tax revenue foregone; and (ii) wealthy parents might be tempted to allocate some of their income to their children to extend their own tax-free earnings / income disregard. How much would be the extra income tax revenue foregone? What constraints, if any, should be placed on this tendency?

9. Ensure that the BI system does not lead to a downward spiral of the economy.

It is sometimes feared that when people first receive a BI, it will provide a large disincentive against their taking, or increasing, paid employment, and the economy will become less productive. However, the incentive to take paid employment comprises two parts: the income effect (the unearned income, which will have increased, will be a disincentive), and the substitution effect (the Marginal Deduction Rate or effective tax rate – decreased for many). However, the changes that take place will be as much an effect of the system that is being replaced as of the new one. Many will experience incentives to seek paid employment, or increase their hours of work, whereas others may prefer to reduce their hours. Not only will there be a redistribution of income, but it is likely that there will be a redistribution of hours of work-for-pay, and, indeed, of unpaid work.

It is also feared that a significant number from the wealthier section of society will emigrate, taking their job-creation schemes with them, – or at least threatening to do so. The UK, being politically stable and with a temperate climate, is a very attractive place in which many wealthy foreigners wish to reside, even without tax loopholes and other government incentives to persuade them. It is the government’s job to protect all of its people, but especially the poorest, who are unable to protect themselves, and it should not submit to blackmail from people who are not committed to contributing to an inclusive society. It should not be a matter of regret if some wealthy people decide to leave.

Let the Full and Partial BIs be fixed proportions of Y-BAR. If the labour supply schedule shifted leftwards (ie reduced labour supply), on the introduction of a BI scheme, as a result of the disincentive effect outweighing the incentive effect, and Y-BAR decreased, then the BI in the next time period would decrease also, the labour supply schedule would shift to the right, thus acting as a self-stabilising mechanism, preventing any tendency towards a downward spiral of the economy. If the BIs are sufficiently generous in the first place, then small reductions in the amount could be tolerated. Similarly, if there were a leftward shift in the labour demand schedule (ie reduced demand for labour) due to external factors, again leading to a reduction in Y-BAR, there would be decreased BIs in the next time period, increasing the incentives to work-for-pay, and shifting the labour supply schedule to the right. It is important that the BIs remain as fixed proportions of Y-BAR, for at least the term of a government’s administration, (and should be announced in each party’s manifesto beforehand), or this important stabilising effect will be lost.

Another important outcome of pegging the proportions for a fixed period is that it will create fiscal drag. The lag resulting from the BIs being distributed in the current fiscal period, but being based on Y-BAR from the calendar year ending at least 15 months earlier, will provide a slight fiscal drag, which will provide a stabilising influence on the country’s economic cycles by reducing their amplitude. This lag will reduce demand when Y-BAR is increasing, and increase demand when Y-BAR is diminishing, in much the same way that the present benefit and income tax systems interact. A prudent government would keep enough reserves to cover the cost of the BIs, in case the economy declines, as did GDP in the UK by 3.76% in monetary terms between 2008 and 2009.

Conclusion

While an analysis of the intended redistributive, and labour market, effects has not yet been carried out, the Basic Income scheme put forward here is designed to redistribute income from rich to poor, to restore incentives to work for the poorest members of society, and to provide a level playing field (all paying the same maximum rate of tax) for everyone else.

This exercise has demonstrated several things. Each person has his/her own ideas about the specific BI system that s/he would like to see implemented, because, in addition to the inclusion of the defining criteria for the BI with their associated advantages, each person has a different set of priorities with respect to other aspects of society and the economy. There is no single, optimum BI system. It has been demonstrated here that one can design and cost one’s own ideal scheme, and experiment with variations.

In order to fulfil my list of stated objectives, I have designed a universal, individual-based, unconditional, tax-exempt Partial BI scheme,

1. that is financed out of a hypothecated new income tax system, replacing the current income tax and employees’ National Insurance contribution systems;

2. where all BIs are stated as proportions of average (mean) income per head, Y-BAR;

3. where financially-vulnerable adults are topped up to a tax-exempt Full BI; a tax-exempt payment to cover the cost of disabilities is paid in addition;

4. where all those receiving a Partial BI would have recourse to a safety net, if necessary;

5. where a method is provided for calculating an approximate figure for the rate of income tax required to finance the scheme. This can be calculated for any BI scheme, whether or not the government is likely to introduce such an income tax system;

6. where Minimum Income Standards provide a benchmark;

7. with a Rule-of-Thumb, where Partial BI = 0.25, and Full BI = 0.50 of Y-BAR respectively, and the required rate of income tax is 40%;

8. where adult recipients of the Partial BI have an earnings/income disregard (zero tax rate) until the Partial BI income tax schedule meets and merges with the Full BI schedule, when gross income, Yo is 0.50 of Y-BAR, and net income is 0.75 of Y-BAR. The required standard rate of income tax is 50%. This provides an illustrative example with easy calculations. However, it was demonstrated that a variety of levels of the Partial BI, and associated income tax concessions on the first tranche of gross income, Yo, could be operated without increasing the standard income tax rate.

9. where the proportions of Y-BAR for the BIs are fixed for the term of administration of a government, to provide a self-stabilising adjustment mechanism, and to reduce the amplitude of economic cycles.

I have also demonstrated that a reasonably generous BI scheme is economically feasible in the UK. Any new scheme would need to be monitored, to confirm that it meets the stated objectives.

I have not dealt with the problem of the provision of social-care, or of day-care for the responsible parent of a dependent child, who wishes to engage in paid employment, nor with any unintended consequences, such as changes in illegal immigration, the birth-rate, environmental effects, or possible inflation. Nor have I calculated the potential savings that could be obtained from the additional beneficial effects of a BI scheme, leading to reductions in the costs of different social programs, including a healthier, more trustworthy/trusting society. As with all things, not only is prevention cheaper than cure, but the prevention of poverty represents a real investment in society and the economy. Of course, the specification of a ‘better society’ is not complete, and needs to include other instruments, such as the provision of education, health services, social housing and public transport. Countries that do not provide universal health and education services as we do in the UK, may wish to provide more generous BI levels than the Rule of Thumb ones proposed here.

It is worth reflecting that income inequality in the UK has increased from a Gini coefficient of 0.25 in 1979 to 0.34 in 1990, with further increases over the next 20 years to 0.36 (Cribb et al, 2012, p.36). The effect of a high degree of inequality on a society can be illustrated by a simple baby-sitting bean group. If one or two households have a low propensity for going out, but carry out lots of baby-sitting, they will accumulate a large stock of beans, and eventually refuse to carry out more baby-sitting. Meanwhile, the rest of the group, in hoc to the bean hoarders, with a reduced aggregate set of beans between them, will be scrabbling about, trying to earn beans by baby-sitting, in order to be able to go out themselves. When the group gets to this stage, if there is not a redistribution of beans, then the group often breaks up.

A Basic Income scheme is not a panacea to cure all ills, but it is a necessary, although not sufficient, condition for a ‘better society’.

The author wishes to thank participants at the North American Basic Income Guarantee Congress at the University of Toronto, 3- 5 May, the Joint East Asian Social Policy Research Network (EASP) and United Kingdom Social Policy Association (SPA) Annual Conference 2012 at the University of York, 16-18 July, and the 14th Basic Income Earth Network Congress, in Munich, 14-16 September, for helpful comments on earlier drafts of this paper.

BIBLIOGRAPHY:

Cribb, Jonathan, Robert Joyce, and David Phillips (2012), Living Standards, Poverty and Inequality in the UK: 2012, London: Institute for Fiscal Studies

DWP, Benefit and Pension Rates, April 2009-2011, BRA5DWP or DWP035, www.dwp.gov.uk/ Click on A-Z, then click on ‘Benefit and Pension Rates’ to download this leaflet.

European Citizen’s Initiative, final draft, 27 April 2012, page 2.

Centre for Research in Social Policy, Loughborough University, 2008, Minimum Income Standards, published by the Joseph Rowntree Foundation.

Miller, Anne G. ‘Minimum Income Standards: A Challenge for Citizen’s Income’, Citizen’s Income Newsletter, 2009/3, pp. 6-14. (www.citizensincome.org)

Office of National Statistics, United Kingdom National Accounts, the Blue Book, for successive years. www.ons.gov.uk/. Click on publications, and enter ‘UK National Accounts’ in the search space. It is easiest to look according to publication date, which is usually around 31 July each year, (but the 2011 edition was released on 23 November 2011). The whole Blue Book can be downloaded as a pdf document.

Population figures: www.statistics.gov.uk/statbase/Product.asp?vlnk=15106.

Taxation figures from Her Majesty’s Revenue and Customs: www.hmrc.org.uk/

APPENDIX A. SOME FIGURES FOR THE UK.

[table id=21 /]

*Recipients of Means-Tested-Benefits are usually eligible for Housing Benefit and Council Tax Benefit also.

SOURCES FOR APPENDIX A:

Mid-year UK population estimates were obtained from www.statistics.gov.uk/statbase/Product.asp?vlnk=15106

GDP = Gross Domestic Product (output method) at market prices, series YBHA, from Table 1.2 of the United Kingdom National Accounts, The Blue Book, 2011 edition.

GDP per capita, series IHXT, from Table 1.5, of The Blue Book, 2011 edition.

Income = ‘Total Resources of Households and Non-Profit Institutions Serving Households’, series QWMF, from Table 6.1.3 of The Blue Book, 2011 edition.

Child Benefit and Child Tax Credit rates from www.hmrc.gov.uk

Tax rates and thresholds from www.hmrc.gov.uk

‘Benefit and Pension Rates’, April 2009 – 2012, BRA5DWP, or DWP035, from www.dwp.gov.uk