by Malcolm Torry

This article was first published as a EUROMOD working paper by the Institute for Social and Economic Research at the University of Essex. It builds on a previous EUROMOD working paper that was subsequently published in the first edition of the Citizen’s Income Newsletter for 2015.

Abstract [note]This paper uses EUROMOD version G2.0++. The contribution of all past and current members of the EUROMOD consortium is gratefully acknowledged. The process of extending and updating EUROMOD is financially supported by the Directorate General for Employment, Social Affairs and Inclusion of the European Commission [Progress grant no. VS/2011/0445.] The UK Family Resources Survey data was made available by the Department of Work and Pensions via the UK Data Archive. All remaining errors and interpretations are the author’s responsibility. Opinions expressed in this paper are not necessarily those of the Citizen’s Income Trust[/note]

A Citizen’s Income – an unconditional and nonwithdrawable income for every individual – would offer many advantages, but because the UK’s current benefits and tax systems are complex, transition to a benefits system based on a Citizen’s Income could be difficult to achieve. This paper builds on the results contained in a previous EUROMOD working paper by proposing two financially feasible ways of implementing a Citizen’s Income. The first method would be an ‘all at once’ method. That is, it would establish a small Citizen’s Income for every citizen of the UK, of whatever age. This paper shows that a strictly revenue neutral scheme is available that could be paid for by raising Income Tax rates by 3%, by abolishing Income Tax Personal Allowances, and by making adjustments to National Insurance Contributions. This scheme would impose almost no household disposable income losses on low income households at the point of implementation, and manageable losses on households in general. A second method – a ‘one step at a time’ method – would turn Child Benefit into a Child Citizen’s Income, then establish a Young adult Citizen’s Income, and then enable those in receipt of the Young adult Citizen’s Income to keep their Citizen’s Incomes as they grow older. This method of implementation would impose almost no losses in household disposable income at the point of implementation. The paper concludes that both ‘all at once’ and ‘one step at a time’ methods would be financially feasible.

Introduction

A Citizen’s Income is an unconditional, nonwithdrawable income for every individual as a right of citizenship. A benefits system based on a Citizen’s Income would offer many advantages over our current largely means-tested system. A Citizen’s Income would deliver reduced marginal deduction rates and so would increase employment incentives; it would offer greater social cohesion; it would not create the stigma that means-tested benefits generate; it would substantially reduce fraud and error rates; and it would be easy to administer. [note]Malcolm Torry, Money for Everyone, Policy Press, Bristol, 2013, pp 81-186[/note]

Research note: A feasible way to implement a Citizen’s Income showed that in 2012/13 a Citizen’s Income of £71 per week (with less for children and young people, and more for elderly people) could have been largely funded by abolishing the Income Tax Personal Allow-ance and means-tested benefits (except for Housing Benefit and Council Tax Benefit), but that at the point of implementation such a scheme would have imposed losses of over 10% of disposable income on 21.12% of low-income households (defined here as households in the lowest disposable income decile) and losses of over 10% on 9.28% of all households. An alternative scheme that retained means-tested benefits and took households’ Citizen’s Incomes into account when means-tested benefits were calculated, and which could have been largely funded by abolishing the Income Tax Personal Allowance and raising all Income Tax rates by 10%, would not have imposed losses on low income households and would have imposed losses of over 10% on only 5.38% of all households. A second alternative scheme, and with a Citizen’s Income of £50 per week, that retained means-tested benefits and took households’ Citizen’s Incomes into account when means-tested benefits were calcul-ated, and that could have been largely funded by abol-ishing the Income Tax Personal Allowance and raising all Income Tax rates by 5%, would not have imposed losses on low income households, and would have imposed losses of over 10% on only 1.09% of all households. [note]Subsequent to the paper’s publication I discovered that as well as Child Citizen’s Incomes being paid I had left Child Benefit switched on. This was of course a major reason for the low levels of losses.[/note]

The problem with all three of the schemes tested for Research note: A feasible way to implement a Citizen’s Income is found in the term ‘largely funded’. Each simulation delivered a funding gap of between £20bn and £24bn per annum – similar to the gap discovered when the costs of the first scheme were calculated using the national accounts. [note]This scheme was first prepared for submission to the House of Commons Work and Pensions Committee enquiry on benefits simplification in 2006. See the committee’s report, Benefits Simplification, HC 463, vol.I, London: The Stationary Office, July 2007, paragraphs 51, 55, 148, 176, 262, 381. www.publications.parliament.uk/pa/cm200607/cmselect/cmworpen/463/46302.htm. The Citizen’s Income Trust’s evidence to the committee can be found in the second volume on page Ev 84 at www.publications.parliament.uk/pa/cm200607/cmselect/cmworpen/463/463ii.pdf. The Trust subsequently published the scheme in its booklet Citizen’s Income: A brief introduction, London: Citizen’s Income Trust, 2006. In 2013 the figures were updated to 2012/13 values and the booklet was Booklet 2013[/note] The proposal made then was that the gap would be partly filled by administrative savings, and that much of the rest could be found by restricting tax relief on pension contributions to the basic rate of Income Tax. [note]Currently higher rate taxpayers can claim tax relief at the higher rate. Department for Work and Pensions running costs are currently £8bn per annum. An assumption is made that administration of Citizen’s Income would cost 1% of the total paid out – the same proportion as for Child Benefit and the Basic State Pension – which would amount to £3bn. A saving of £5bn is therefore assumed. For the sources, figure, and calculations, see Citizen’s Income: A brief introduction, London: Citizen’s Income Trust, 2013, www.citizensincome.org/filelibrary/booklet2013.pdf[/note] However, as Donald Hirsch has pointed out, this method of funding a Citizen’s Income is different in kind from changes in the Personal Allowance, in Income Tax rates, in National Insurance Contributions rates and earnings limits, and in means-tested and other benefits. It would be different from changes that would be intimately linked to the implementation of a Citizen’s Income. Rather proving this point, before the General Election the Labour Party said that it wanted to restrict tax relief on pension contributions and to use the additional revenue to reduce university tuition fees. I therefore propose that we should distinguish between ‘revenue neutrality’ and ‘strict revenue neutrality’. The schemes tested in Research note: A feasible way to implement a Citizen’s Income are revenue neutral: that is, the costs of the Citizen’s Incomes are met from elsewhere in the tax and benefits systems. In this paper I shall restrict myself to schemes that exhibit strict revenue neutrality: that is, the Citizen’s Incomes will be paid for by reducing or abolishing means-tested and other benefits, by reducing or abolishing Income Tax Personal Allowances, and/or by raising Income Tax and/or National Insurance Contribution rates.

I shall apply the following criteria to the schemes that I shall regard as feasible:

- Strict revenue neutrality (as above)

- Income Tax rates to rise not more than 3% (see below) (adjustments to National Insurance Contributions earnings limits, and of National Insurance Contributions up to 12% of earnings, are permitted)

- No more than 2% of low income households should suffer losses of over 5% of disposable income at the point of implementation

- Any redistribution should be modest and should be from rich to poor.

In search of an ‘all at once’ Citizen’s Income scheme

The first two schemes that I have tested for this research paper are similar to the first and third schemes tested in Research note: A feasible way to implement a Citizen’s Income. I have omitted the second of those original schemes because it required Income Tax rates to rise by 10% as well as leaving a large funding gap, so to remove the funding gap would have required an even larger increase in Income Tax rates. In this paper I have added a third scheme – scheme C – because I have been asked what Income Tax rates would be required to pay Citizen’s Incomes equal to the Minimum Income Standards published by the Joseph Rowntree Foundation. [note]Minimum Income Standards for 2013 can be found at www.jrf.org.uk/site/files/jrf/images/MIS-2013-figure2.jpg. Deciding the levels of Citizen’s Incomes that would match the Minimum Income Standards is not a simple matter as MIS levels are calculated for households whereas Citizen’s Incomes are paid to individuals. The weekly MIS levels for 2013 are as follows (excluding rent and childcare): single work-age person, £200.64; pensioner couple, £241.25; Couple and two children, £471.16; Lone parent and one child, £284.57. Citizen’s Incomes based on the smaller assessment units would be higher than Citizen’s Incomes based on the larger units. I have chosen to be guided by the larger units. I have set the young person’s Citizen’s Income rate half way between the adult and child rates.[/note] Characteristics that apply to the schemes are as follows:

- For the first scheme, Citizen’s Income rates are pegged to 2013/14 means-tested benefits rates (rather than to 2012/13 rates, as in the previous research note). [note]The most recent tax and benefits regulations available in EUROMOD version G2.0++ are those for 2013/14, and the most recent Family Resource Survey data is for 2009, uprated to 2013 values. It is therefore not currently possible to simulate Citizen’s Income schemes for more recent periods. ‘The factors that are used to update monetary variables (parameter sheet Uprate_uk) from the mid-point of the data year (October 2009) to the mid-point of the policy years applying on June 30th (i.e. October 2010 to October 2013) are shown in Annex 1 of the EUROMOD UK country report. No other updating adjustments are employed. Thus the distribution of characteristics (such as employment status and demographic variables) as well as the distribution of each income source that is not simulated remain as they were in 2009/10’ (Paola De Agostini and Holly Sutherland, Euromod Country Report: United Kingdom 2009-2013, Colchester: Institute for Social and Economic Research, Essex University, 2014)[/note]

- For all three schemes, National Insurance Contributions (NICs) above the Upper Earnings Threshold are raised from 2% to 12% and the Lower Earnings Limit is reduced to zero. This has the effect of making NICs payable on all earned income at 12%. This seems to me to be an entirely legitimate change to make. The ethos of a flat rate benefit such as Citizen’s Income is consistent with both progressive tax systems and with flat rate tax systems, [note].B. Atkinson, Public Economics in Action: The Basic Income / Flat Tax Proposal, Clarendon Press, Oxford, 1995[/note] but not with regressive tax systems.

- For all three schemes, all Income Tax Personal Allowances are set at zero.

- As suggested above, the schemes are strictly revenue neutral. The net cost of each scheme is at or below £2bn per annum.

- Estimates of administrative savings are conservative. In the first and third schemes, means-tested benefits are abolished (apart from Housing Benefit and Council Tax Benefit [note]In 2013/14 Council Tax Benefit was centrally regulated. Under the Government’s localisation agenda, its replacement, Council Tax Support, is locally regulated as well as locally administered. This means that every borough in the country can invent its own regulations, and, in particular, its own taper rate. It will be far from easy to include Council Tax Support in future tax and benefits simulations. [/note]). Given that current DWP running costs are £8bn per annum, we can assume savings of £4bn per annum. For the schemes that do not abolish means-tested benefits, large numbers of households will no longer be receiving means-tested benefits, but the means-tested structure will need to stay in place. So in the case of scheme B I assume a saving of £1bn per annum.

As in the research for Research note: A feasible way to implement a Citizen’s Income, I have studied the gains and losses experienced by households, and not those experienced by individuals. There are good arguments for both approaches. It is individuals who receive income, so gain or loss is an individual experience; and within households income is not necessarily equitably shared, so the amounts that individuals receive might be more relevant than the amount that the household receives. However, we can assume that in most cases income is to some extent pooled within households, so if one member gains and another loses then the household might be better off, which might be more significant than that one member of the household suffering a loss. Another point to make about households is that they are of different sizes, so the absolute gain or loss is not particularly relevant. However, percentage gains and losses are relevant, so this is the measure that we shall use.

Particularly problematic is knowing how to order households. A household of two parents and three children with twice the disposable income of a household containing just one adult will not be as well off as that individual adult. For the purposes of this exercise I ignore the different sizes of households. More detailed research, employing household weights so that the disposable incomes of households of different sizes could be more relevantly compared, would constitute a further research project. [note]Malcolm Torry, Research note: A feasible way to implement a Citizen’s Income, Institute to Social and Economic Research Working Paper EM17/14, Colchester: Institute for Social and Economic Research, University of Essex, September 2014, pp. 3-4[/note]

The following table summarises the characteristics of the schemes and the results of the simulations:

[table id=7 /]

(See the footnote for the method [note]The method is as follows: A new set of benefits is created in the UK country system in EUROMOD: a Citizen’s Pension (CP) for over 65 year olds, a Citizen’s Income (CI) for adults aged between 25 and 64, a young person’s Citizen’s Income (CIY) for adults aged between 16 and 24), and a Child Citizen’s Income (CIC) for children aged between 0 and 15. In the definitions of constants, levels are set for these Citizen’s Incomes, and all Personal Tax Allowances are set at zero. So that the additional taxable income is taxed at the basic rate, and not at the higher rate, the first tax threshold is changed from 32010 to 42010. The National Insurance Contribution Lower Earnings Limit is set to zero, and the NIC rate above the Upper Earnings Limit is set to 12% (to match the rate below the limit). For the first scheme, Working Tax Credit, Child Tax Credit, Income Support, Income Related ESA, Pension Credit, and Income based Jobseeker’s Allowance are no longer added to the total for means-tested benefits. Incapacity Benefit, Contributory ESA and Child Benefit are removed from non-means-tested benefits (except that in the second scheme Child Benefit is left in payment). For all schemes, the Citizen’s Income total is added to non-means-tested benefits, and for the second and third schemes Citizen’s Incomes are added to the means applied to means-tested benefits. The state pension is no longer added to the pensions total in the first and third schemes (as the Citizen’s Pension has already been added to the non-means-tested benefits total). Where benefits are no longer in payment they are removed from the tax base. Simulations of the 2013 system and the system being tested generate two lists of household disposable incomes for the entire Family Resource Survey sample. These then generate a list of gains (negative gains are losses), and the total of the gains gives the net cost of the scheme for the sample. To convert EUROMOD’s monthly figures to annual figures, and the sample size to the total population, a multiplier of (12 x 64.1m / 57,381) = 13.4m gives the cost for the UK population. A process of trial and error adjusts the Income Tax rates until the net cost minus the assumed administrative saving is below £2bn per annum. The initial disposable incomes are then ordered, the bottom 10% are selected, and the percentage gains are evaluated. The process is then repeated for all households.[/note])

Discussion

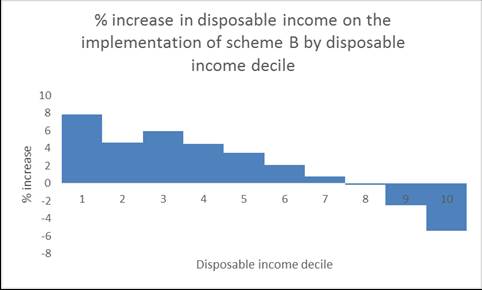

In relation to schemes A and C, while it is true that the high losses imposed on households at the point of implementation are the result of the complexity of the current tax and benefits scheme, and not of the Citizen’s Incomes, such losses would make the schemes impossible to implement. And while it is true that higher tax rates in the context of Citizen’s Incomes that are worth more than the Personal Allowance ought not to be a problem, and that what matters is the overall gain or loss in disposable income, Income Tax rates are a psychological as well as a financial issue, [note]Donald Hirsch, Could a ‘Citizen’s Income’ work? York: Joseph Rowntree Foundation, 4th March 2015, pp. 25-28. www.jrf.org.uk/publications/could-citizens-income-work[/note] and to raise them by more than say 3 per cent would probably make a scheme impossible to implement. So while all three schemes would be revenue neutral in the strictest sense, the only scheme likely to be viable would be scheme B.

There are three additional advantages attached to scheme B:

a) On average, it would deliver a modest redistribution from rich to poor: [note]Table generated from the results of statistics obtained from EUROMOD simulations for the current tax and benefits system and for scheme B.[/note]

The Gini coefficient for disposable income would be reduced from 0.3 to 0.28.

b) In relation to the income component of poverty, the number of children in poverty would be reduced from 12.16% to 9.19%, i.e., by nearly a quarter.

c) Because all existing benefits are left in place, this scheme could be implemented both easily and quickly. All that would be required would be for the Citizen’s Incomes to be paid, Income Tax Personal Allowances and the National Insurance Contributions Lower Earnings Limit to be reduced to zero, Income Tax rates to be adjusted, National Insurance Contributions to be collected at 12% on all earned income, and means-tested benefits to be recalculated – which would be easy to do as every household’s Citizen’s Incomes would be of entirely predictable amounts.

A long term aim

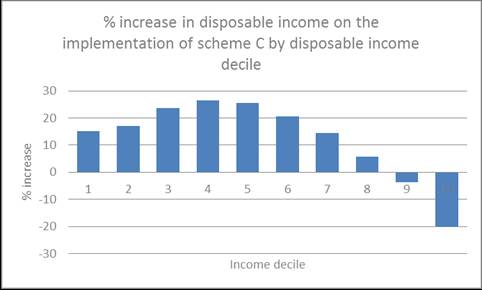

However, having made the case that only a scheme that satisfied the criteria suggested above would be politically acceptable, there is no reason why a Citizen’s Income based on Minimum Income Standards should not remain a longer term aim. Such a scheme would have a considerable effect on inequality ( – it would reduce the Gini coefficient from 0.3 to 0.2), and it would reduce from 12.16% to just 1.60% the number of children in poverty. Redistribution would be largely towards the middle range of incomes, which could be politically acceptable – although a reduction of 20% in the disposable incomes of the highest disposable income decile might be contentious for some:

A ‘one step at a time’ method

In the UK there is a tradition of cautious and piecemeal change to the benefits system. This has its disadvantages – particularly when the current system no longer fits the society, economy and employment market that it needs to serve – but the advantage is that new approaches can be tested out without causing too much disruption to administrative systems or to household budgets. But let us assume that the arguments for Citizen’s Income are understood by policymakers, and that only the difficulties relating to the transition from the current system to one based on a Citizen’s Income stand in the way. In this situation it could be useful to have asked about the financial feasibility of taking the first steps towards a universal unconditional and nonwithdrawable income for every citizen.

Clearly a possible method would be to start with children and young people, say up to the age of eighteen, and then as they grow into adulthood to allow them to keep their Citizen’s Incomes. If at the same time the new Single Tier State Pension were to be turned into a genuine Citizen’s Pension, then it would take about fifty years to implement the Citizen’s Income ( – a period that could be shortened by thirteen years if a pre-retirement unconditional and nonwithdrawable income were to be paid to everyone over the age of 55).

The first step: raising Child Benefit for children up to the age of 15 (i.e. to their sixteenth birthday) and equalising the Child Benefit paid for every child.

Here, the only other change made is to increase National Insurance Contributions by 4% above the Upper Earnings Limit. [note]Purely for the purpose of modelling the net cost, we eliminate Child Benefit for 16 to 19 year olds by adjusting the definition of a dependent child in both the current system and in the system with raised Child Benefit.[/note] Income Tax Personal Allowances and tax thresholds remain as they are.

The results for two different rates are as follows:

[table id=8 /]

Discussion

Scheme b fulfils our criteria, but the Income Tax rate for scheme a is too high.

However, as we can see from the following chart, the number of children in poverty would be reduced by a tenth if a single rate of £40 were to apply to children under the age of 16, and to raise Child Benefit to £56.80 would reduce by a quarter the number of children in poverty. Such reductions in child poverty would in themselves be an excellent reason for raising Child Benefit immediately to a single rate of £40, and then to £56.80. For such a virtuous purpose, increasing Income Tax rates by 4.5% might be acceptable.

[table id=9 /]

The modest rise in National Insurance Contributions, and bearable rises in Income Tax rates, would in either case suggest political feasibility for such a worthwhile outcome. To establish such a Citizen’s Income for children would be a useful first step on the road to a Citizen’s Income for every age group, and one that could be achieved with public acceptance simply because children are universally regarded as a deserving demographic group.

The second step: implementing a Young adult CI of £56.80 per week for young adults between their sixteenth and their nineteenth birthdays. (This could be paid to the main carer until the eighteenth birthday, and then transferred to the young adult; or a staged transfer could occur.)

The only change to be made would be to increase National Insurance Contributions, in this case by 6% above the Upper Earnings Limit. [note]The results are modelled by removing Child Benefit for everyone aged 16 and above, and instead paying a Young adult Citizen’s Income. In this case the results are extracted from simulations of individual rather than household disposable incomes. As above, the removal of Child Benefit over the age of sixteen is achieved by adjusting the definition of a dependent child. [/note] Income Tax Personal Allowances and tax thresholds remain as they are, except that for those young adults now receiving a Citizen’s Income all earnings would be taxed, thus enabling their Citizen’s Incomes to be paid for as they grew older.

[table id=10 /]

Discussion

This relatively modest proposal would not raise Income Tax rates, could generate savings (which would be useful), and would begin to sort out the income maintenance of a demographic group that is currently ill served by a patchwork of provisions that makes little sense and that doesn’t provide the kind of flexibility needed during a period which is inevitably one of transitions.

Discussion of both of the above steps taken together

Comparing the two schemes b and d with scheme B above shows that the increases in National Insurance Contributions above the Upper Earnings Limit and in Income Tax rates required by scheme B are generated by the Citizen’s Incomes granted to children and young adults, and that the working adult Citizen’s Incomes are effectively paid for by the loss of the Income Tax Personal Allowance, as we would rather expect.

If both the increased Child Benefit and the Young adult’s Citizen’s Income were to be implemented, then National Insurance Contributions would be at 12% on all earned income. The recipient year groups would not receive Income Tax Personal Allowances, and as they grew older they would continue to receive Citizen’s Incomes (while everyone older than them would not be receiving Citizen’s Incomes and would retain their Personal Allowances). The means-tested benefits structure would still be in place, and we would be well on the way to implementing scheme B (but with a genuine Child Citizen’s Income, rather than a combination of Child Benefit and Child Citizen’s Income). Gradual increases in the Citizen’s Income rates for children and young adults would be both affordable and acceptable, enabling a Citizen’s Income of £56.80 to be paid to all adults. Further rises might be acceptable. Because of the gradual nature of the implementation, nobody would ever need to suffer the modest losses in disposable income that would occur if the entire scheme were to be implemented all in one go. Income Tax rates might have to rise slightly, but the simulation of scheme B suggests that they would not need to rise by more than 3% over the fifty year implementation period if the adult Citizen’s Income were to be at £50 per week.

Conclusion

In his new book Inequality, Tony Atkinson makes a number of proposals for reducing inequality: a more progressive Income Tax; Child Benefit paid at a substantial rate; an EU-wide Child Basic Income; and a Participation Income that looks as if it has been modelled as a Citizen’s Income. [note]Anthony B. Atkinson, Inequality, Cambridge, MA: Harvard University Press, 2015, pp. 303-4. The text offers some pointers towards social participation conditions for receipt of the Participation Income, but no such conditions are mentioned in the text relating to the results of EUROMOD modelling on p.297[/note] It is perhaps no surprise that Atkinson’s agenda and the content of this paper are similar; and equally no surprise that the steps that both Atkinson and this paper envisage would be steps towards a Citizen’s Income.

We need a new approach to tax and benefits in the UK, and a Citizen’s Income offers precisely what we require. Increasingly objections are not to the principle of a Citizen’s Income, but to its feasibility. In this paper I have shown that there are feasible ways of implementing a Citizen’s Income, either all at once or by one step at a time. There would of course be other ways to implement a Citizen’s Income, and more research in this area would be most welcome.

What matters above all is that at every stage it should be a genuine Citizen’s Income that is implemented, because it is the characteristics of universality, unconditionality, and nonwithdrawability, and the fact that every individual receives their own Citizen’s Income, that deliver the many social and economic advantages of a Citizen’s Income. Those advantages will need to be experienced at every stage of any implementation method if the population as a whole is to appreciate the advantages that a Citizen’s Income for every citizen would offer. The implementation methods outlined above are for genuine Citizen’s Incomes, and research on additional implementation options should follow the same rule.

Similarly, to be politically feasible, proposed Citizen’s Income schemes should be strictly revenue neutral, should not propose large increases in Income Tax rates, and should impose very few losses on low income households, either at each stage of the implementation process or at full implementation for the entire population. As we have seen, such losses can be eliminated if implementation begins with children and young adults and they keep their Citizen’s Incomes as they grow older. A Citizen’s Income implemented for every individual at the same time will always generate some initial losses, simply because the current benefits system is so complicated – but, as we have seen, it would still be possible to implement a Citizen’s Income scheme all in one go while imposing relatively few losses on low income households.

The difficulties facing our current tax and benefits systems, and the importance of fashioning a benefits system that will better serve our society and our economy, suggest that the Government, think tanks, and academic institutions should now be applying substantial research and policy analysis resources to the subject: and the many arguments for a Citizen’s Income, [note]Malcolm Torry, Money for Everyone: Why we need a Citizen’s Income, Bristol: Policy Press, 2013; Malcolm Torry, 101 Reasons for a Citizen’s Income: Arguments for giving everyone some money, Bristol: Policy Press, forthcoming, 2015[/note] along with the results in this Working Paper, suggest that a considerable proportion of that effort should be spent on fashioning a tax and benefits system based on a Citizen’s Income.

References

Anthony B. Atkinson, Inequality, Cambridge, MA: Harvard University Press, 2015

Citizen’s Income Trust, Citizen’s Income: A brief introduction, London: Citizen’s Income Trust, 2007

Citizen’s Income Trust, Citizen’s Income: A brief introduction, London: Citizen’s Income Trust, 2013

House of Commons Work and Pensions Committee (2007) Benefit Simplification, the Seventh Report of Session 2006-7, HC 463, London: The Stationery Office, pp Ev.84-90

Malcolm Torry, ‘Research note: A Citizen’s Income scheme’s winners and losers’, Citizen’s Income Newsletter, issue 3 for 2012, London: Citizen’s Income Trust, pp 2-4. www.citizensincome.org

Malcolm Torry, Money for Everyone: Why we need a Citizen’s Income, Bristol: Policy Press, 2013

Malcolm Torry, ‘Research note: A feasible way to implement a Citizen’s Income’, Citizen’s Income Newsletter, issue 1 for 2015, pp 4-9

Malcolm Torry, 101 Reasons for a Citizen’s Income: Arguments for giving everyone some money, Bristol: Policy Press, forthcoming, 2015

Notes