This is an edited version of a paper presented at the BIEN Congress held in Tampere, Finland, in August 2018 [1]

Introduction

A Citizen’s Basic Income is an unconditional, nonwithdrawable income paid to every individual as a right of citizenship. It is as simple as that. Citizen’s Basic Income has a number of different names: Citizen’s Income, Basic Income, Citizen’s Basic Income, Universal Basic Income. They all mean exactly the same: an unconditional income paid to every individual.

The amount paid to an individual would not depend on their income, it would not depend on their wealth, it would not depend on their household structure, it would not depend on their employment status, and it would not depend on anything else. Every individual of the same age would receive exactly the same: the same amount, every week or every month, automatically.

Older people might receive more than working age adults, younger adults less, and less for children. Does adjusting the amount with someone’s age compromise Citizen’s Basic Income’s unconditionality? No, it does not. What is unique about Citizen’s Basic Income, what matters, and what makes it work, is that it can be turned on at someone’s birth, and turned off at their death, that no active administration is required in between, and that nothing that anyone can influence, or that requires enquiry of any kind, can affect it. Once the computer knows someone’s date of birth, it never needs to ask about their age: it can seamlessly adjust the amount that an individual is paid as their age changes. Everyone of the same age would receive exactly the same income, unconditionally.

Sometimes words are added, but they are not necessary. Citizen’s Basic Income is unconditional, so within the jurisdiction in which it is paid everybody gets it, so it is universal. There is no need to say that it is. Citizen’s Basic Income is unconditional, which means that it would not fall if other income rose, so it is nonwithdrawable. There is no need to say that it is. It is universal, and it is nonwithdrawable. But all we need to say is this: Every individual of the same age would receive exactly the same income, unconditionally.

The definition published by the Citizen’s Basic Income Trust reads as follows:

A Citizen’s Basic Income is an unconditional, automatic and nonwithdrawable income for each individual as a right of citizenship. (A Citizen’s Basic Income (CBI) is sometimes called a Basic Income (BI) or a Citizen’s Income (CI))

- ‘Unconditional’: A CBI would vary with age, but there would be no other conditions: so everyone of the same age would receive the same CBI, whatever their gender, employment status, family structure, contribution to society, housing costs, or anything else.

- ‘Automatic’: Someone’s CBI would be paid weekly or monthly, automatically.

- ‘Nonwithdrawable’: CBIs would not be means-tested. Whether someone’s earnings or wealth increase, decreased, or stayed the same, their Citizen’s Basic Income would not change.

- ‘Individual’: CBIs would be paid on an individual basis, and not on the basis of a couple or household.

- ‘As a right’: Everybody legally resident in the UK would receive a CBI, subject to a minimum period of legal residency in the UK, and continuing residency for most of the year. (Citizen’s Basic Income Trust, 2018)

According to the definition published on BIEN’s website:

A basic income is a periodic cash payment unconditionally delivered to all on an individual basis, without means-test or work requirement.

That is, basic income has the following five characteristics:

- Periodic: it is paid at regular intervals (for example every month), not as a one-off grant.

- Cash payment: it is paid in an appropriate medium of exchange, allowing those who receive it to decide what they spend it on. It is not, therefore, paid either in kind (such as food or services) or in vouchers dedicated to a specific use.

- Individual: it is paid on an individual basis—and not, for instance, to households.

- Universal: it is paid to all, without means test.

- Unconditional: it is paid without a requirement to work or to demonstrate willingness-to-work. (BIEN)

The different definitions exhibit different emphases, but, apart from the fact that the same term, ‘unconditional’, is used with two different meanings, they are almost consistent with each other and they represent a consensus – and, after all, consensus is what definitions are about.

Citizen’s Basic Income, and Citizen’s Basic Income schemes

A Citizen’s Basic Income is always as defined above, and anything that conforms to those definitions is a Citizen’s Basic Income. A Citizen’s Basic Income scheme is different: It specifies the levels of Citizen’s Basic Income to be paid to each age group, the frequency of the payments, and also the funding mechanism, which might be changes to the existing tax and benefits system, or maybe some other method. Consider two different Citizen’s Basic Income schemes: both would pay working age adult Citizen’s Basic Incomes somewhere around £70 per week, and different amounts for older and younger people; both would be largely funded by abolishing the Income Tax Personal Allowance and the National Insurance Contribution Primary Earnings Threshold; but one would abolish means-tested benefits, while the other would leave them in place and recalculate them on the basis that every individual in a household would now be receiving a Citizen’s Basic Income and that net earnings will have been changed by the abolition of the Income Tax Personal Allowance and the National Insurance Contribution Primary Earnings Threshold. The schemes would exhibit some very different effects. In particular, the scheme that abolished means-tested benefits would impose significant losses on low income households at the point of implementation, whereas the scheme that retained means-tested benefits would not. The latter would be politically feasible, whereas the former would not be (Torry, 2014; 2015a).

Rothstein v. Torry

In November 2017, Social Europe published an article by Bo Rothstein entitled ‘UBI: A bad idea for the welfare state’ (Rothstein, 2017). The article sets out from a definition of ‘Unconditional Universal Basic Income’ (UUBI) as ‘every citizen will be entitled to a basic income that frees them from the necessity of having a paid job’; and it adds the details that the level of UBI would be £800 per month, and that ‘all means-tested programs for those who cannot support themselves through paid work can be abolished’. Rothstein correctly identifies as an advantage of such a reform that it ‘would force employers to create more acceptable and less demeaning types of work because people would not take jobs they consider unsatisfactory. Releasing people from the compulsion to have a paid job would, according to the proponents, also mean strengthening the voluntary/civil society sector and cultural life’. He equally correctly identifies as disadvantages that it ‘would be unsustainably expensive and would thereby jeopardize the state’s ability to maintain quality in public services such as healthcare, education and care of the elderly’, that it would lose political legitimacy, and that ‘people who can work [would] choose not to work’. Rothstein’s verdict is that ‘the basic error with the idea of unconditional basic income is its unconditionality’, because that threatens ‘the principle of reciprocity … Breaking with this principle is most likely to lead to the dismantling of the type of broad-based social solidarity that built [the] welfare state.’

Not so. The main problem with the Universal Basic Income that Rothstein discusses in his article is not its unconditionality: it is the flawed definition.

As we have seen, the definition of Citizen’s Basic Income implies neither a particular amount, nor that means-tested benefits would be abolished, and it does not imply that the UBI would necessarily free people from paid employment. Rothstein has confused his particular Citizen’s Basic Income scheme with Citizen’s Basic Income.

Instead of a Citizen’s Basic Income scheme that pays £800 per month to every individual, and that abolishes means-tested benefits, we could pay £264 per month to every individual (with different amounts for children, young adults, and elderly people), and leave means-tested benefits in place and recalculate them on the basis that household members would be receiving Citizen’s Basic Incomes. Instead of leaving undefined the funding method for Citizen’s Basic Income, as Rothstein does, we could choose to fund it by abolishing the Income Tax Personal Allowance and the National Insurance Contribution Primary Earnings Threshold (so that Income Tax and NICs would be paid on all earned income), we could apply a flat rate of National Insurance Contribution of 12% to all earned income (rather than the current two-tier 12% and 2% structure), and we could increase Income Tax rates by just 3%. As research conducted at the Institute for Social and Economic Research shows (Torry, 2017b; 2018c), far from being ‘unsustainably expensive’, this scheme would require no additional public expenditure, and it would not affect expenditure on public services. Rothstein cannot show that his scheme would not impose significant losses on low income households. This alternative scheme would not impose significant losses on low income households, it would impose few losses on households in general, and it would still take a lot of households off means-tested benefits. Rothstein cannot tell us how his scheme would redistribute disposable income, or how it would affect poverty or inequality indices. This alternative scheme would redistribute from rich to poor, it would reduce every poverty index, and it would significantly reduce inequality. Rothstein tells us that his scheme would reduce the incentive to seek employment. This alternative scheme would reduce marginal deduction rates ( – a marginal deduction rate is the rate at which additional earned income is reduced by taxation and the withdrawal of means-tested benefits) (Torry, 2018c), and would therefore be likely to incentivise employment, self-employment, and new small businesses. It certainly would not disincentivise them. Far from compromising the reciprocity on which our society is built, it would enhance it. And this alternative scheme would not lose the advantages that Rothstein mentions. Because everyone would have a secure financial platform on which to build, this Citizen’s Basic Income scheme, like Rothstein’s, would give to workers a greater ability to seek the employment or self-employment that they wanted, and would therefore encourage employers to supply better jobs in order to attract workers; and because this Citizen’s Basic Income scheme would give to each household more choice over its employment pattern, it would still encourage both caring and community activity. (Further details of this alternative scheme can be found in the appendix, and additional details in Torry, 2018c.)

Distinctions matter. A Citizen’s Basic Income is always an unconditional income paid to every individual, without means test and without work test. A Citizen’s Basic Income scheme specifies the rate at which the Citizen’s Basic Income would be paid for each age group, and the funding mechanism. There are many possible Citizen’s Basic Income schemes. As Rothstein correctly suggests, his chosen scheme would have many disadvantages. As I have shown, an alternative scheme might exhibit none of those disadvantages, and might offer many additional advantages. Both of the schemes contain genuine Citizen’s Basic Incomes, but only one of them is desirable and feasible.

Citizen’s Basic Income and Minimum Income Guarantee

A Citizen’s Basic Income is an unconditional, automatic and nonwithdrawable income for each individual as a right of citizenship. A Minimum Income Guarantee is very different: it is a level of disposable income below which a household is not allowed to fall. The amount of money that a government will need to pay to the household will therefore depend on the household’s income from other sources (earnings, pensions, interest on savings, other benefits, and so on) and on the composition of the household.

The 1970s Canadian and US experiments were Minimum Income Guarantee experiments rather than Citizen’s Basic Income experiments. The fact that those experiments exhibited clear health benefits and very little employment market withdrawal suggests that a Citizen’s Basic Income might have similar effects, but because a Minimum Income Guarantee and a Citizen’s Basic Income are not the same, that cannot be assumed.

Pitts et al v. Torry

In the final edition of the journal Renewal for 2017, Frederick Pitts, Lorena Lombardozzi and Neil Warner suggested that the experience of the Speenhamland reforms of 1795 were ‘an experiment in a kind of basic income’ (Pitts, Lombardozzi and Warner, 2017: 150). They were not. They were an extension of means-tested poor relief to the working poor. The supplements paid out of the rates were designed to fill the gap between the worker’s earnings and a specified minimum income that was related to the size of the family and the price of bread (Speizman, 1966: 45). The scheme was a Minimum Income Guarantee, and the supplements paid were a means-tested benefit. They were definitely not a Citizen’s Basic Income. The modern equivalents of the Speenhamland project are Working Tax Credits and so-called Universal Credit, and not Citizen’s Basic Income.

Not only is a Minimum Income Guarantee different from a Citizen’s Basic Income: the effects would be different. The Speenhamland payments fell if earnings rose, and rose if earnings fell. The Speenhamland supplement therefore functioned as a dynamic subsidy. Because it rose if wages fell, employers who cut wages knew that the supplement would make up for the wage cut. A Citizen’s Basic Income would remain the same whatever the individual’s earnings, so it would be a static subsidy: that is, it would not rise if wages fell, so both employers and employees would know that if wages fell then employees’ families would be worse off. In the context of a Citizen’s Basic Income, both collective bargaining and the National Minimum/Living Wage would be even more important than they are now, and the effort to maintain them would intensify.

Another difference relates to employment incentives. Within the communities that were paying the Speenhamland supplement, for breadwinners with large families there was no financial advantage to seeking increased wages, a better-paying job, or additional skills. Increased wages would mean a lower supplement. But because a Citizen’s Basic Income would never change, anyone currently on means-tested benefits whose Citizen’s Basic Income enabled them to come off them would immediately experience increased incentives to seek higher wages, or to seek additional skills in order to obtain a better-paying job. No longer would an increase in wages result in a loss of benefits, so an increase in earned income would result in a far greater increase in net income. (See the appendix for research results on the number of households that would be taken off means-tested benefits by a fairly modest Citizen’s Basic Income scheme.)

Pitts, Lombardozzi and Warner are quite right to make a variety of criticisms of the Speenhamland approach. Means-tested in-work benefits such as the Speenhamland supplements, Working Tax Credits, and Universal Credit, do, as they suggest, ‘keep the cost of labour competitive with machines so that employers keep workers hanging on for longer than otherwise would be the case’; they do restrict ‘the freedom of workers to sell their capacity to labour to employers as equal parties to a contract’; and they do ‘render impossible the commodification of labour in a world still organised on the basis of the commodification of everything else’ (Pitts, Lombardozzi and Warner, 2017: 149–50). A Citizen’s Basic Income, on the other hand, would never compromise ‘the bargaining power of labour’, and so would not contribute to ‘falling or stagnating wages and deteriorating employment prospects’ (Pitts, Lombardozzi and Warner, 2017: 151). Indeed, by providing a secure financial platform on which individuals and households could build, a Citizen’s Basic Income would increase workers’ ability to start their own businesses, to turn down badly-paid jobs, and to argue for wage increases.

The Citizen’s Basic Income enthusiasts that Pitts, Lomardozzi and Warner have in their sights are those who suggest that a Citizen’s Basic Income would be a useful response to an automated economy in which fewer human workers would be required. It needs to be said that we cannot know the future of the employment market. Previous periods of technological change have seen new jobs created at the same time as existing jobs have been destroyed, and whether current and future technological change will have similar or different effects we cannot know. It is the fact that we cannot know the future shape of the employment market that is the argument for Citizen’s Basic Income. The benefits system that we are running in the UK is still a combination of the Poor Law and Speenhamland – that is, means-tested benefits both in and out of work. It is a system designed for a 1940s employment market characterised by long-term full-time jobs. This is even more true of Universal Credit. But the world has changed, and it will continue to change in ways that we cannot now predict. What we shall need is an income maintenance strategy that makes no assumptions about the future structure of the employment market, that incentivises employment, that provides as much freedom as possible for workers to choose how to deploy their labour, and that does not depress wages. Today’s benefits system is precisely what is not required. A Citizen’s Basic Income might be the best option.

Conclusion

The Citizen’s Basic Income debate is important, it is increasingly lively, and the number of organisations and individuals engaged with it is increasing rapidly. If the debate is to be rational then it is essential that all of the players should agree on definitions, and that they should use them consistently.

Rothstein tells us that he is discussing Citizen’s Basic Income, whereas in fact he is discussing a particular Citizen’s Basic Income scheme. Pitts, Lomardozzi and Warner tell us that the Speenhamland payments were a kind of Citizen’s Basic Income, whereas in fact they constituted a Minimum Income Guarantee: something entirely different. Such confusions are not helpful. What the Citizen’s Basic Income debate requires is not erroneous comparisons but high-quality research, careful logic, clear distinctions, and agreed definitions that everybody adheres to.

Appendix

A feasible Citizen’s Basic Income scheme for the UK

This appendix is based on the EUROMOD working paper Torry, 2018c. [2] For further details, and for the calculations and results relating to marginal deduction rates, please see the working paper.

- Introduction

This appendix evaluates the following illustrative Citizen’s Basic Income scheme:

- A Citizen’s Basic Income for every UK citizen, funded from within the current tax and benefits system.

- Current means-tested benefits would be left in place, and each household’s means-tested benefits would be recalculated to take into account household members’ Citizen’s Basic Incomes in the same way as earned and other income is taken into account.

As a previous working paper has shown (Torry, 2014), a Citizen’s Basic Income scheme that abolished existing means-tested benefits, and that was funded purely by making adjustments to the current Income Tax system, would generate significant losses for low income households. A Citizen’s Basic Income scheme that both abolished existing means-tested benefits and avoided losses for low income households would need additional funding from outside the current tax and benefits systems. In the foreseeable future such additional funding is unlikely to be forthcoming. In the longer term a Citizen’s Basic Income large enough to enable current means-tested benefits to be abolished while avoiding losses for low income households might be possible, but Torry 2014 suggests that in the short term any feasible implementation of a Citizen’s Basic Income will need to leave the current means-tested benefits system in place.

The research behind the working paper on which this appendix is based was guided by the same principle as previous working papers (Torry 2014; 2015a; 2016a; 2016b; 2017b): that is, as few changes as possible would be made to the current tax and benefits system, consistent with the other aims in view: revenue neutrality (Hirsch, 2015: 11, 25–28, 33), which I shall take to be a net cost or saving of no more than £2bn per annum; and the avoidance of significant losses, particularly for low income households. I shall also assume that raising Income Tax rates by more than 3 percentage points would be politically infeasible (Hirsch, 2015: 3–5, 25–28), but that equalising National Insurance Contributions at 12% across the whole earnings range would be just, sensible, and acceptable. The research discovers the levels at which Citizen’s Basic Incomes could be paid under these conditions, and evaluates the scheme in relation to poverty and inequality indices, the numbers of households able to escape from means-tested benefits, and household disposable income gains and losses.

2. The illustrative Citizen’s Basic Income scheme

The Citizen’s Basic Income scheme to be tested is constructed as follows:

- Unconditional Child Benefit is increased by £20 per week for each child.

- National Insurance Contributions (NICs) above the Upper Earnings Limit are raised from 2% to 12%, and the Primary Earnings Threshold is reduced to zero. This has the effect of making NICs payable on all earned income at 12%. (This seems to me to be an entirely legitimate change to make. The ethos of a flat rate benefit such as Citizen’s Basic Income is consistent with both progressive tax systems and with flat rate tax systems, but not with a regressive tax system (Atkinson, 1995)).

- The Income Tax Personal Allowances are set to zero.

- Tax-free Citizen’s Basic Income levels are set as follows: An Education Age Citizen’s Basic Income (ECBI), for 16 to 19 year olds no longer in full-time education, is set at £40 per week; a Young Adult’s Citizen’s Basic Income (YCBI), for people aged 20 to 24, is set at £50 per week; a Working Age Adult Citizen’s Basic Income (WACBI, or simply CBI), for people aged 25 to 64, is set at £63 per week; [3] and a Citizen’s Pension, for everyone aged over 65, is set at £40 per week. The existing National Insurance Basic State Pension is left in place. (In this particular scheme the ECBI is not paid to someone still in full-time education, in recognition of the fact that their main carer is receiving Child Benefit on their behalf.)

- Income Tax rates are adjusted as required in order to achieve revenue neutrality.

It might be suggested that it would be better either to retain Child Benefit as it is and pay a separate small Child Citizen’s Basic Income at the same rate for every child, or to abolish Child Benefit and to pay an equal Citizen’s Basic Income, and that to pay an enhanced Child Benefit at different rates for the first and for the second and subsequent children would compromise the principle that everyone of the same age should receive the same level of income. This might be true in theory, but in practice the situation is more complex. This Citizen’s Basic Income scheme envisages that Child Citizen’s Basic Incomes will be paid to the main career, as is Child Benefit. So what is happening in practice is that children receive no Citizen’s Basic Incomes while their main carers receive varying amounts in relation to the number of children in their families. This means that to pay different amounts for the first and for the second and subsequent children would simply vary the already varying amounts paid to main carers of children. It would preserve sufficient of the unconditionality principle by ensuring that every main carer of the same number of children would receive the same total level of Citizen’s Basic Income, made up of their own Citizen’s Basic Incomes and those for their children. To enhance the level of Child Benefit is therefore legitimate in practice as well as conforming to our principle of making the smallest number of changes possible. (A similar approach is taken by Painter and Thoung, 2015.)

Net cost, and household gains and losses

This part of the evaluation is based on the effects of the Citizen’s Basic Income scheme on household disposable incomes rather than on individuals’ disposable incomes. There are good arguments for both approaches. It is individuals who receive income, so gain or loss is an individual experience; and within a household income is not necessarily equitably shared, so the amounts that individuals receive might be more relevant than the amount that the household receives. However, we can assume that in most cases income is pooled within households, at least to some extent, so if one member gains and another loses then the household might be better off, and that might be a more significant factor than that one member of the household has suffered a loss in disposable income. Because households are of different sizes, an absolute gain or loss is not particularly relevant. However, percentage gains and losses are relevant, so this is the measure that we use.

Table 1 summarises the results obtained from microsimulation of the scheme proposed here. [4]

Table 1: An evaluation of an illustrative Citizen’s Basic Income scheme with the working age adult Citizen’s Basic Income set at £63 per week for fiscal year 2017-18.

| Citizen’s Pension per week (existing state pensions remain in payment) | £40 |

| Working age adult Citizen’s Basic Income per week | £63 |

| Young adult Citizen’s Basic Income per week | £50 |

| Education age Citizen’s Basic Income per week | £40 |

| (Child Benefit is increased by £20 per week) | (£20) |

| Income Tax rate increase required for strict revenue neutrality | 3 % |

| Income Tax, basic rate (on £0 – 43,000) (plus NICs on earnings) | 23 % (+12%) |

| Income Tax, higher rate (on £43,000 – 150,000) (plus NICs) | 43 % (+12%) |

| Income Tax, top rate (on £150,000 – ) (plus NICs) | 48 % (+12%) |

| Proportion of households in the lowest original income quintile experiencing losses of over 10% at the point of implementation | 1.62 % |

| Proportion of households in the lowest original income quintile experiencing losses of over 5% at the point of implementation | 2.67 % |

| Proportion of all households experiencing losses of over 10% at the point of implementation | 1.90 % |

| Proportion of all households experiencing losses of over 5% at the point of implementation | 9.88 % |

| Net cost of scheme | £2bn p.a. |

We can conclude that the scheme would be revenue neutral (that is, it could be funded from within the current income tax and benefits system); that the increase in Income Tax rates required would be feasible; and that the scheme would not impose significant numbers of significant losses on low income households. In theory there should be no losses for low income households because current means-tested benefits would still be in place and would be recalculated to take account of households’ Citizen’s Basic Incomes and changes in net incomes. Further research on the detail of the Family Resources Survey data would be required to discover the particular household circumstances that generate losses. Losses for higher income households will be due to increased Income Tax and National Insurance Contribution rates on higher earnings.

We can conclude that the scheme would be financially feasible.

Changes to means-tested benefits claims brought about by the scheme

Tables 2 and 3 give the results of calculations based on microsimulation of the current Social Security scheme and of the Citizen’s Basic Income scheme.

Table 2: Percentage of households claiming means-tested social security benefits for the existing scheme in 2017 and for the Citizen’s Basic Income Scheme

| The existing scheme in 2017 | The Citizens Basic Income scheme | % reduction | |

| Percentage of households claiming any means-tested benefits | 33.2% | 30.9% | 6.9% |

| Percentage of households claiming more than £100 per month in means-tested benefits | 29.2% | 24.7% | 15.3% |

| Percentage of households claiming more than £200 per month in means-tested benefits | 26.6% | 21.3% | 20.2% |

(For details for individual classes of benefits, see the working paper Torry, 2018c.)

Table 3: Percentage reductions in total costs of means-tested benefits, and percentage reductions in average value of household claims, on the implementation of the Citizen’s Basic Income scheme

| Reduction in total cost | Reduction in average value of claim | |

| All means-tested benefits | 30.7% | 25.5% |

(For details for individual classes of benefits, see the working paper Torry, 2018c.)

These results show that the Citizen’s Basic Income scheme would reduce

- by 6.9% the number of households receiving means-tested benefits;

- the total cost of these benefits by nearly a third;

- by a quarter the average amount of these benefits received by households claiming them;

- by 15.3% the number of households receiving more than £100 per month in these benefits; and

- by one fifth the number receiving more than £200.

A lot of households would find it far easier to come off means-tested benefits than they do now.

The poverty, inequality and redistributional effects of the Citizen’s Basic Income scheme

Table 4 shows the changes that the illustrative Citizen’s Basic Income scheme would bring about in relation to poverty and inequality.

Table 4: Changes in poverty and inequality indices brought about by the Citizen’s Basic Income scheme

| The current tax and benefits scheme in 2017 | The Citizen’s Basic Income scheme | Percentage change in the indices | |

| Inequality | |||

| Disposable income Gini coefficient | 0.30 | 0.27 | 9.2% |

| Poverty headcount rates | |||

| Total population in poverty | 12% | 8% | 33.3% |

| Children in poverty | 14% | 6% | 56.3% |

| Working age adults in poverty | 12% | 9% | 29.4% |

| Economically active working age adults in poverty | 4% | 2% | 39.4% |

| Elderly people in poverty | 11% | 9% | 11.6% |

We can conclude that

- the Citizen’s Basic Income scheme would deliver a significant reduction in inequality;

- even more significantly, child poverty would fall by a half, and working age poverty would also fall substantially.

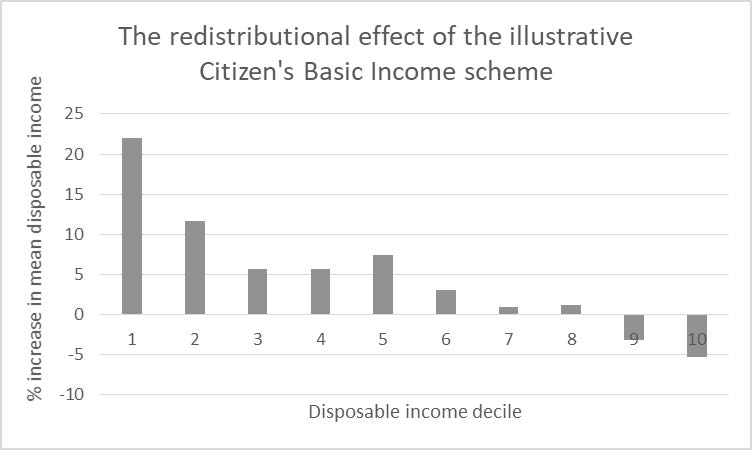

Table 5 and figure 1 show the aggregate redistribution that would occur if the Citizen’s Basic Income scheme were to be implemented.

Table 5: The redistributional effect of the illustrative Citizen’s Basic Income scheme

| Disposable income decile | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| % increase in mean disposable income | 22.0 | 11.7 | 5.7 | 5.7 | 7.4 | 3.1 | 1.0 | 1.2 | –3.2 | –5.3 |

Figure 1: The redistributional effect of the illustrative Citizen’s Basic Income scheme

The table and graph show that the scheme would achieve manageable and useful redistribution from rich to poor, with those households often described as the ‘squeezed middle’ benefiting from the transition as well as the poorest households.

- Conclusion

Because the only changes required in order to implement this illustrative Citizen’s Basic Income scheme would be

- payment of the Citizen’s Basic Incomes for every individual above the age of 16 (apart from those between 16 and 19 still in full-time education), calculated purely in relation to the age of each individual,

- increases in the rates of Child Benefit,

- changes to Income Tax and National Insurance Contribution rates and thresholds, and

- easy to achieve recalculations in existing means-tested benefits claims,

the entire scheme could be implemented very quickly.

This simple scheme would substantially reduce poverty and inequality; it would remove large numbers of households from a variety of means-tested benefits; it would reduce means-tested benefit claim values, and the total costs of means-tested benefits; particularly for the large number of households no longer on means-tested benefits, it would provide additional employment market incentives to the extent that marginal deduction rates affect employment market behaviour; it would avoid imposing significant numbers of losses at the point of implementation; and it would require almost no additional public expenditure.

This simple illustrative scheme could be both feasible and useful.

Bibliography

Atkinson, A.B. (1995) Public Economics in Action: The Basic Income / Flat Tax Proposal, Clarendon Press, Oxford.

BIEN, http://basicincome.org/basic-income/

Citizen’s Basic Income Trust, http://citizensincome.org/

Citizen’s Basic Income Trust (2018) Citizen’s Basic Income: A brief introduction, London: Citizen’s Basic Income Trust

De Agostini, Paola (2017) EUROMOD Country Report United Kingdom 2013–2016, Colchester: Institute for Social and Economic Research, February 2017, https://www.euromod.ac.uk/sites/default/files/country-reports/year7/Y7_CR_UK_Final.pdf

Department for Work and Pensions (2003) Tax Benefit Model Tables April 2003, London: Department for Work and Pensions Information Centre, Information and Analysis Directorate.

Hirsch, Donald (2015) Could a ‘Citizen’s Income’ work? York: Joseph Rowntree Foundation, www.jrf.org.uk/publications/could-citizens-income-work

Makovec, Mattia and Miko Tammik (2017) Baseline results from the EU28 EUROMOD: 2011–2016, EUROMOD Working Paper EM17/14, Colchester: Institute for Social and Economic Research, University of Essex, www.iser.essex.ac.uk/research/publications/working-papers/euromod/em6-17

OECD (2017) Basic Income as a Policy Option: Can it add up? Paris: OECD, www.oecd.org/employment/emp/Basic-Income-Policy-Option-2017.pdf

Painter, Anthony and Chris Thoung, (2015) Report: Creative Citizen, Creative State – The principled and pragmatic case for a Universal Basic Income, London: Royal Society of Arts, https://www.thersa.org/discover/publications-and-articles/reports/basic-income. (A review of the report can be found in Citizen’s Income Newsletter, issue 2 for 2016, London: Citizen’s Income Trust, 2016, pp. 20–21, http://citizensincome.org/research-analysis/the-royal-society-of-arts-report-on-citizens-income/ .)

Pitts, Frederick Harry, Lorena Lomardozzi, and Neil Warner (2017) ‘Speenhamland, automation and the basic income: A warning from history?’ Renewal, 25 (3–4): 145–155

Rothstein, Bo (2017) ‘UBI: A bad idea for the welfare state’, Social Europe, 23 November 2017, https://www.socialeurope.eu/ubi-bad-idea-welfare-state

Speizman, Milton D. (1966) ‘Speenhamland: An experiment in guaranteed income’, Social Service Review, 40 (1): 44–55

Torry, Malcolm (2013) Money for Everyone: Why we need a Citizen’s Income, Bristol: Policy Press.

– (2014) Research note: A feasible way to implement a Citizen’s Income, EUROMOD Working Paper EM17/14, Colchester: Institute for Social and Economic Research, University of Essex, www.iser.essex.ac.uk/research/publications/working-papers/euromod/em17-14

– (2015a) Two feasible ways to implement a revenue neutral Citizen’s Income scheme, EUROMOD Working Paper EM6/15, Colchester: Institute for Social and Economic Research, University of Essex, www.iser.essex.ac.uk/research/publications/working-papers/euromod/em6-15

– (2015b) 101 Reasons for a Citizen’s Income: Arguments for giving everyone some money, Bristol: Policy Press

– (2016a) An evaluation of a strictly revenue neutral Citizen’s Income scheme, EUROMOD Working Paper EM5/16, Colchester: Institute for Social and Economic Research, University of Essex, https://www.iser.essex.ac.uk/research/publications/working-papers/euromod/em5-16

– (2016b) Citizen’s Income schemes: an amendment, and a pilot project – addendum to EUROMOD Working Paper EM5/16, EUROMOD Working Paper EM5/16a, Colchester: Institute for Social and Economic Research, University of Essex, https://www.iser.essex.ac.uk/research/publications/working-papers/euromod/em5-16a

– (2016c) The Feasibility of Citizen’s Income, New York: Palgrave Macmillan

– (2016d) Citizen’s Basic Income: A Christian social policy, London: Darton, Longman and Todd

– (2016e) How might we implement a Citizen’s Income, London: ICAEW, www.icaew.com/-/media/corporate/files/technical/sustainability/outside-insights/citizens-income-web—final.ashx?la=en; for a report on the consultation, see http://citizensincome.org/news/icaew-report-on-implementing-citizens-income/.

– (2017a) ‘Universal Basic Income: Definitions and details’, Social Europe, 11 December 2017, https://www.socialeurope.eu/universal-basic-income-definitions-details

― (2017b) A variety of indicators evaluated for two implementation methods for a Citizen’s Basic Income, Institute for Social and Economic Research, Colchester, Euromod Working Paper EM 12/17, www.iser.essex.ac.uk/research/publications/working-papers/euromod/em12-17

― (2018a) ‘Speenhamland, automation, and Basic Income: A response’, Renewal, 26 (1): 32–35

― (2018b) A presentation given at event held at the London School of Economics, 20 February 2018, http://www.lse.ac.uk/Events/LSE-Festival/Events/20180220/beveridge-rebooted

― (2018c) An update, a correction, and an extension, of an evaluation of an illustrative Citizen’s Basic Income scheme – addendum to EUROMOD working paper EM12/17, Institute for Social and Economic Research, Colchester, Euromod Working Paper EM 12/17, www.iser.essex.ac.uk/research/publications/working-papers/euromod/em12-17a

– (2018d) Why we need a Citizen’s Basic Income: The desirability, feasibility and implementation of an unconditional income, Bristol: Policy Press

Notes

[1] This paper is based partly on Torry, 2017a; 2018a; 2018b; 2018c.

[2] I am most grateful to Alari Paulus of the Institute for Social and Economic Research for considerable assistance with the original working paper EM 12/17. The results presented here are based on EUROMOD version H1.0+. EUROMOD is maintained, developed and managed by the Institute for Social and Economic Research (ISER) at the University of Essex, in collaboration with national teams from the EU member states. We are indebted to the many people who have contributed to the development of EUROMOD. The process of extending and updating EUROMOD is financially supported by the European Union Programme for Employment and Social Innovation ‘Easi’ (2014–2020). The UK Family Resources Survey data was made available by the Department of Work and Pensions via the UK Data Archive. The results and their interpretation are the authors’ responsibility. Opinions expressed in this paper are not necessarily those of the Citizen’s Basic Income Trust.

[3] For the calculation, see the working paper Torry, 2018c.

[4] For details of the method, see the working paper Torry, 2018c.