Editorial

Private Eye

We couldn’t resist a recent news item:

Gordon Brown’s tax credit policy isn’t just driving claimants mad: it’s thrown his own staff into a state of gibbering confusion too.

After reporting changes in her childcare arrangements, one Eye reader had the temerity to question a demand for repayment of a tax credit overpayment. Not only did HM Revenue and Customs customer support unit respond that ‘it is not possible to explain how the figure of [£x] per week was calculated’, but she was also told the demand would stand as ‘we do not think it was reasonable for you to expect that your payments were correct.’

Quite right, too. Anyone who knows anything about tax credits would never believe they were being paid the right amount …

(Private Eye, September 2006)

The serious point being made of course is that the greater the complexity of a tax and benefits system, the greater the likelihood that mistakes will be made; and, as computer companies and civil servants are discovering, the greater the complexity of a system the greater the difficulties of computerising it – leading, we believe, to software developers determining constraints on tax and benefits policy.

The only alternative is genuine simplification – and the obvious model is the simplest benefit of them all: Child Benefit.

Sue Royston of the Department for Work and Pensions Simplification Unit is inviting advice agencies to tell her how things could be made easier for clients: ‘We believe complexity matters because it may prevent customers getting the benefits to which they are entitled. It may lead to errors both by staff in administering the benefit and by customers in not being clear what they need to report. It makes the system time consuming and therefore costly to administer. The benefits system has become complex because of the wish to ensure fairness for customers whose circumstances may be complicated; the desire to maximise the use of limited resources and the need to safeguard the system against fraud and abuse. In addition, over time, a multitude of small and large scale changes have been introduced which have interacted and overlapped with existing provisions to cause further complexity, which can be difficult for staff and customers alike to navigate their way around. The introduction of the Tax Credit System and the way it interacts with existing benefits has added a whole new layer of complexity for customers and staff. There are, however, things which can be done to reduce complexity and the unit have been asked to look at what can be achieved in the current year.’

The ‘Community Care’ website (on 22nd June 2006) reports that measures to help people into work have the opposite effect: It suggests that ‘there is a carrot-and-stick approach to moving people off benefits. The carrots are tax credits, national minimum wage, benefit ‘run-ons’, special rules for disregarding earnings and so on. The sticks are just as numerous: tighter rules on proving that you are looking for work or establishing you are genuinely sick; penalties for turning work down; greater policing of the claimant’s out-of-work activity.’ Particularly problematic is the ‘rule that limits unemployed claimants to studying fewer than 16 hours a week even if the course they want to do would subsequently increase their employability. This rule has been belatedly recognised as a barrier to employment. From September, in ….. pilot areas, low-skilled unemployed people will be able to attend full-time training and retain their Jobseeker’s Allowance. The site cites the example of a carer with a partner with disabilities who finds herself no better off employed for 15 hours per week than when employed for 4 hours per week, and worse off if they are employed for 20 hours per week than if they are employed for 4 hours per week. The article concludes: ‘There is something wrong with a benefit system that is so complicated that it’s difficult for people to make informed choices about what work they can safely undertake and not be worse off. And these are issues that must be addressed.’

The government of Kuwait is to give a grant of 200 dinars (690 dollars) to each citizen. The two million foreign workers in the oil-rich emirate were not included.

The Institute for Fiscal Studies has discovered that when household spending, rather than income, is used to measure living standards, relative poverty in Britain has risen, rather than fallen, since 1997. The study, funded by the Joseph Rowntree Foundation, suggests that a useful alternative definition of relative poverty would be living in a household which spends less than 60% of the median-spending household, rather than the measure most frequently used by the government, which is to be living in a household whose income is less than 60% of the median-income household. Using this alternative measure, the study finds that the rate of child poverty based on household spending rose by 11 per cent between 1996/97 and 2002/03, whereas the measure of child poverty targeted by the Government, based on income, fell by 15 per cent over the same period.

The Economic and Social Research Council has reported on a research project by Professor Jane Millar (in The Edge, issue 22, July 2006, p.31) which shows that non-poor low-paid employees have less chance of staying out of poverty during the following year than non-poor employees in general (91% as opposed to 96%), and that ‘tax credits and in-work benefits play an important role in keeping some low-paid people out of poverty, but are associated with a lower probability of avoiding poverty over time.’ As Professor Millar writes, ‘preliminary analysis of our data suggests the need to question the sustainability of relying too heavily on this type of fiscal strategy in preventing poverty over the longer term.’

A Norwegian research project has reported that being in contact with the needs testing part of the welfare state reduces levels of interpersonal trust but universal welfare arrangements increase them. The researchers conclude: ‘If it is the case that social capital as trust is an asset both for individuals and for society as a whole, interpersonal trust should ideally be cultivated, so also by the welfare state. From a policy point of view, one solution to develop trust, or at least not break it down, may thus be to restructure parts of the system of social assistance. In line with the results from this study, this may be possible by developing the universality of the welfare system as opposed to making it even more discretionary’ (Christer Hyggen, ‘Risks and Resources: Social Capital among Social Assistance Recipients in Norway’, Social Policy and Administration, vol.40, no.5, October 2006, p.507).

The Sixth Congress of the U.S. Basic Income Guarantee Network will take place from 23 to 25 February 2007 in New York City. The Congress is co-sponsored by USBIG and the Citizen Policies Institute and takes place in conjunction with the annual meeting of the Eastern Economics Association. Proposals are welcome on topics relating to the Basic Income Guarantee or to the current state of poverty and inequality. Suggested topics include but are not limited to the financing of BIG; the history of BIG; gender, family, and labour market issues of BIG; rights and responsibilities relating to BIG; strategies for implementing BIG; and empirical issues of BIG, and of poverty including cost estimates. The purpose of the conference is discussion, and all points of view are welcome. The USBIG Congress is entirely autonomous in content and submissions are welcome in any academic discipline and from non-academics. Deadline for submissions: Oct 27, 2006. (For further information see www.usbig.net)

Basic Income Studies: An International Journal of Basic Income Research (BIS) is a new international journal devoted to the critical discussion of and research into universal basic income and related policy proposals. BIS is published by the Berkeley Electronic Press and edited by an international team of scholars, with support from Red Renta Básica, the Basic Income Earth Network and the U.S. Basic Income Guarantee Network. The inaugural issue of BIS appeared in June with articles by Joel Handler and Amanda Sheely Babcock, Michael W. Howard, Yannick Vanderborght, and a retrospective on Robert van der Veen and Philippe Van Parijs’s seminal article on ‘A Capitalist Road to Communism’. The retrospective includes a reprint of the original article and a set of specially written comments by Gerald Cohen, Erik Olin Wright, Doris Schroeder, Catriona McKinnon, Harry Dahms, and Andrew Williams, together with a specially written reply by the authors. BIS is currently inviting contributions from academic scholars, researchers, policy-makers and welfare advocates on a wide variety of topics pertaining to the universal welfare debate and particularly welcomes research that pushes the debate into previously uncharted areas. BIS aims to promote the research of young scholars as well as seasoned researchers, and the editors particularly welcome contributions from non-Western countries. For more information, please visit the website at www.bepress.com/bis or contact the editors, Jurgen De Wispelaere and Karl Widerquist, at bis-editors@bepress.com. Scholars who want to have their books considered for review or who would like to review a book for BIS should contact Sandra González Bailón at bis-bookreviews@bepress.com.

The left-leaning thinktank Compass has recently shown some interest in the Citizen’s Income debate, and we are grateful to Compass for permission to reprint a ‘Thinkpiece’ on Citizen’s Income which appeared on their website early in 2006:

Compass Thinkpiece Number 4

A Citizen’s Income: a recipe for change

The context

At the moment, if someone who is on means-tested Income Support or Jobseeker’s Allowance enters employment, fairly soon their benefit is withdrawn pound for pound (apart from a small disregard), and, as their income rises, they lose Housing Benefit and Council Tax Benefit and start to pay Income Tax and National Insurance Contributions.

Something similar happens to someone in low paid work who is receiving tax credits: as their earned income rises, tax credits fall, income tax is paid, National Insurance Contributions are paid, Housing Benefit is lost ….

The ‘unemployment trap’ and the ‘poverty trap’ discourage people from entering employment and from seeking to increase their earned incomes. The problem is compounded by the complexity of the system and the resulting uncertainty over how much net income someone will have if they enter or change their employment and have to pay travel and other expenses. This situation is bad for them, for their families, for their communities, and for the economy.

If you want to understand the depth and breadth of the unemployment and poverty traps then there is no substitute for looking at the Department of Work and Pensions’ Tax and Benefit Model Tables (at www.dwp.gov.uk/asd/asd1/TBMT_2005.pdf).

By the ‘depth’ of the poverty trap we mean the extent of the marginal deduction rate, i.e., the rate at which income is withdrawn for any particular level of earned income. So, to take the example below, a lone parent who is a private tenant and who has one child under 11 experiences a marginal deduction rate of 89.5% for any earned income within the range £134.33 to £392.66. By the ‘breadth’ of the poverty trap we mean the spectrum of earned incomes for which there is a high marginal deduction rate: so here the breadth of the poverty trap is defined by an earned income of £392.66 per week.

The table shows the situation quite graphically:

Marginal Deduction Rates

Lone Parent with 1 child under 11 , Private Tenant

| Gross earnings £ per week | Event | Marginal deduction rates |

|

34.04

|

Income reduces HB/CTB |

85.0%

|

|

94.00

|

NI becomes payable |

87.9%

|

|

94.13

|

Tax payable at 10% |

88.1%

|

|

100.13

|

WTC reduced by pay |

93.7%

|

|

107.59

|

CTB disappears |

85.3%

|

|

143.33

|

Tax payable at 22% |

89.5%

|

|

266.79

|

WTCdisappears/CTC reduced by pay |

89.5%

|

|

392.66

|

HB disappears |

33.0%

|

|

630.00

|

NI Upper Earnings Limit (UEL) |

23.0%

|

|

717.21

|

Tax payable at 40% |

41.0%

|

|

958.91

|

CTC family element reduced by pay |

47.7% |

|

1,108.91

|

CTC disappears |

41.0%

|

HB = Housing Benefit

CTB = Council Tax Benefit

NI = National Insurance Contributions

WTC = Working Tax Credit

CTC = Child Tax Credit

What is most disturbing about the tables is that it is families with children which suffer the deepest and the broadest poverty traps. All families with children (whether with one parent or two) experience marginal deduction rates of over 60% on gross earnings at least up to £300 per week and often beyond £400 per week, and some family types experience marginal deduction rates of over 80% on gross earnings up to £300 per week. This situation makes it difficult for families with children to lift themselves out of poverty by earning more.

Analysis

The detailed tables in the publication make it clear that the one benefit which both reduces child poverty and does not contribute to marginal deduction rates is Child Benefit. This is because Child Benefit is paid unconditionally, so to increase it is to reduce child poverty because 1) it increases the net income of families with children, and 2) it reduces the marginal deduction rates for families with children and thus enables families to lift themselves out of poverty by earning more.

The detailed tables make it equally clear that the major culprits in the deepening and broadening of poverty traps are Working Tax Credit and Child Tax Credit. Whilst the motives for their introduction were excellent (and they have indeed reduced poverty for many families with children), their long-term effects might be little short of disastrous because they make it very hard for families with children to earn their way out of poverty.

If the government were looking for a way to continue to reduce child poverty at the same time as increasing families’ incentives to increase their net income by improving their skills and increasing earned income (good for them, and good for the economy), then the obvious way forwards would be to reduce tax credits and at the same time increase Child Benefit.

And in general the less means-testing is done the easier it will be for families and individuals to earn their way out of poverty.

A similar issue arises with pension provision. At the moment there is a significant disincentive to save for old age, and independent financial advisers are unwilling to advise on pension plans because it is not clear what the fiscal situation will be when the individuals concerned reach retirement age. If there is still considerable means-testing when that happens then the pension fund’s customer might have gained little advantage from saving for retirement.

The prescription

A Citizen’s Income (CI) is ‘an unconditional, non-withdrawable income payable to each individual as a right of citizenship’ (Citizen’s Income Trust strapline). Within that definition a wide variety of options are possible in terms of how large the income might be and how it might be paid for. Most of the research and debate which the Citizen’s Income Trust has undertaken or sponsored has been based on the premise that only a small Citizen’s Income is politically feasible in the short- to medium-term and that only revenue-neutral schemes funded by something like existing tax rates are likely to be considered (i.e., schemes entirely paid for by reducing tax allowances, means-tested benefits and National Insurance benefits and by leaving income tax rates at somewhere near their current level) – though this presupposition has been somewhat dented recently by the Irish Government’s willingness to consider a sizeable Citizen’s Income paid for by substantially increasing tax rates (Department of the Taoiseach, 2002). An adult Citizen’s Income of €109 per week is envisaged, paid for by a single tax rate of 47.14% (Anne Miller, 2003). And the Citizen’s Income Trust is itself about to publish a persuasive paper which shows that a Citizen’s Income paid at £90 for each adult might be feasible.

But the debate about how large a Citizen’s Income would be is a secondary matter. What matters is the structure: its unconditionality, its nonwithdrawability, and its payment to individuals rather than to households; and it is this structure which creates its effect, which makes it attractive to people with a variety of political outlooks, and which gives it its close relationship with notions of citizenship.

Because the Citizen’s Income is not withdrawn as earnings rise, a large CI would mean that net income would rise steadily for the poorest families as earned income rises, and a small CI would mean that for those families still on means-tested benefits net income would rise more rapidly than it does now.

For Britain’s many flexible workers, a Citizen’s Income would provide a measure of security on which they could build. Part-time work and self-employment would become more attractive, allowing people to develop more flexible patterns of working more consistent with their own and their children’s or other dependents’ needs. Thus consistently high levels of employment can be expected.

(For a single person living alone and simply, and maybe for other categories of people, a Citizen’s Income might have a disincentive effect; but for most individuals the incentive effect of lower withdrawal rates will outweigh the small disincentive effect of receiving the Citizen’s Income.)

A Citizen’s Income would help people to undertake higher education, training, or retraining by providing a small, secure income.

Above all, a Citizen’s Income would help to tackle poverty by providing an income on which people with low earnings potential could build through paid work and savings. Rather than destroying the work ethic, as our present system does, a Citizen’s Income would help to lift people out of the various traps outlined above and would encourage them to earn a living (Citizen’s Income Trust, 2003a).

A universal Citizen’s Pension would encourage people to save for their retirement because it wouldn’t be withdrawn from people with personal pensions or other investments, as the Pension Credit is now. The second report from the Pensions Commission, published on 30 November 2005, recommends ‘reforms to make the state system less means-tested and closer to universal ….’.

A Citizen’s Pension would do this, and it would enable meaningful advice to be offered on pension plans because net income in retirement would be more predictable.

One of the particularly interesting things about the Citizen’s Income idea is the support expressed by members of all of the major political parties. The Citizen’s Income Trust has conducted a survey amongst MPs which shows this. (www.citizensincome.org/resources/newsletter%20issue%203%202004.shtml ) The reason is probably that a Citizen’s Income would increase equality, freedom, and a sense of citizenship.

A particular revenue-neutral Citizen’s Income scheme

Using Family Expenditure Survey data for Great Britain for 2003, POLIMOD (a modelling programme maintained by Holly Sutherland at the Microsimulation Unit at the Department of Applied Economics at the University of Cambridge) analyses the effects of changes to the tax and benefits system. For the purposes of this exercise only revenue-neutral possibilities were considered so that the changes create neither a net gain nor a net loss to the exchequer; and only schemes which require the minimum of administrative change were considered in order to facilitate an easy transition. (In particular, tax credits are left in place and all means-tested and National Insurance benefits are left as they are – though of course the payment of a Citizen’s Income will cause the amount of means-tested benefits received by an individual or a family to be reduced).

The scheme

- Child benefit is increased to £15 per child.

- A Citizen’s Income is paid as follows: £20 p.w. to 16/17 year olds; £25 to adults below 65 years old, £30 between 65 and 75, £35 above 75.

- The individual tax allowance is reduced to 0.

- A flat rate of income tax of 26% up to the current higher tax threshold, and thereafter 40% as now.

The results are as follows:

- The scheme is revenue-neutral.

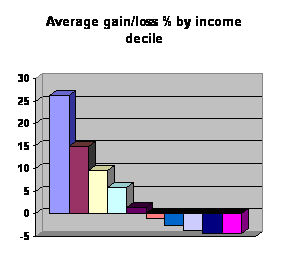

- Gainers and losers are as follows:

| Income decile | Average gain/loss % |

| 10 | -4.20 |

| 9 | -4.40 |

| 8 | -3.65 |

| 7 | -2.63 |

| 6 | -1.00 |

| 5 | 1.34 |

| 4 | 5.70 |

| 3 | 9.51 |

| 2 | 14.78 |

| 1 | 26.17 |

Thus income is redistributed from people in the higher income deciles and towards those in the lower deciles, with high percentage increases for those in the lower deciles and low percentage decreases for those in the higher deciles. This kind of redistribution will not affect the lifestyles of the wealthy overmuch, it will leave middle-income individuals and families in much the same position as they are in now, and it will considerably increase the incomes of the poorest section of the community – and it achieves this while not deepening the poverty or unemployment traps. Because every individual and household will receive a greater proportion of their income as non-withdrawable cash payments, those in the lower earnings deciles will experience lower withdrawal rates and thus a greater incentive to increase their earned income.

References

Atkinson, Tony (1991), ‘Participation income’, Citizen’s Income Bulletin, London: Citizen’s Income Trust, no.16, July 1993, pp.7-11

Bentley, Tom (2004), ‘The self-creating society’, Renewal, vol.12, no.1, pp.13-24

Blaug, Ricardo (2004), ‘Perception of participation and ten pieces of reform’, Renewal, vol.12, no.1, pp.33-39

Citizen’s Income Trust (2003a), Citizen’s Income, London: Citizen’s Income Trust, 2003

Citizen’s Income Trust (2003b), Citizen’s Income Newsletter, London: Citizen’s Income Trust, no.3 for 2003, pp.1-10

Citizen’s Income Trust (1996), ‘Participation Income’, unpublished paper, London: Citizen’s Income Trust

Citizen’s Income Trust (1997), How Citizen’s Income could become a Practical Reality, London: Citizen’s Income Trust

Clark, Charles (2002), The basic income guarantee: ensuring progress and prosperity in the 21st century, Dublin: The Liffey Press, in association with the Conference of Religious of Ireland Justice Commission

Clark, Charles (1996), ‘Basic income, inequality, and unemployment: rethinking the linkage between work and welfare’, Journal of Economic Issues, vol.30, no.2, pp.399-407

Department of the Taoiseach (2002), Basic Income: A Green Paper, Dublin: Department of the Taoiseach

Finlayson, Alan (2004), ‘Citizenship and the democracy of politics’, Renewal, vol.12, no.1, pp.25-32

Lawson, Neal and Daniel Leighton (2004), ‘Blairism’s agoraphobia: Active citizenship and the public domain’, Renewal, vol.12, no.1., pp.1-12

Lord, Clive (2003), A Citizen’s Income: A foundation for a sustainable world, Charlbury: Jon Carpenter

Miller, Anne (2003), ‘The Irish Situation’, Citizen’s Income Newsletter, London: Citizen’s Income Trust, no. 2 for 2003, pp.1-5

Van Parijs, Philippe (1991), ‘Why surfers should be fed: the liberal case for an unconditional basic income’, Philosophical and Public Affairs, vol.20, pp.101-31

Wright, Erik Olin (2004), ‘Envisioning real utopias’, Renewal, vol.12, no.1, pp.69

© Citizen’s Income Trust 2013